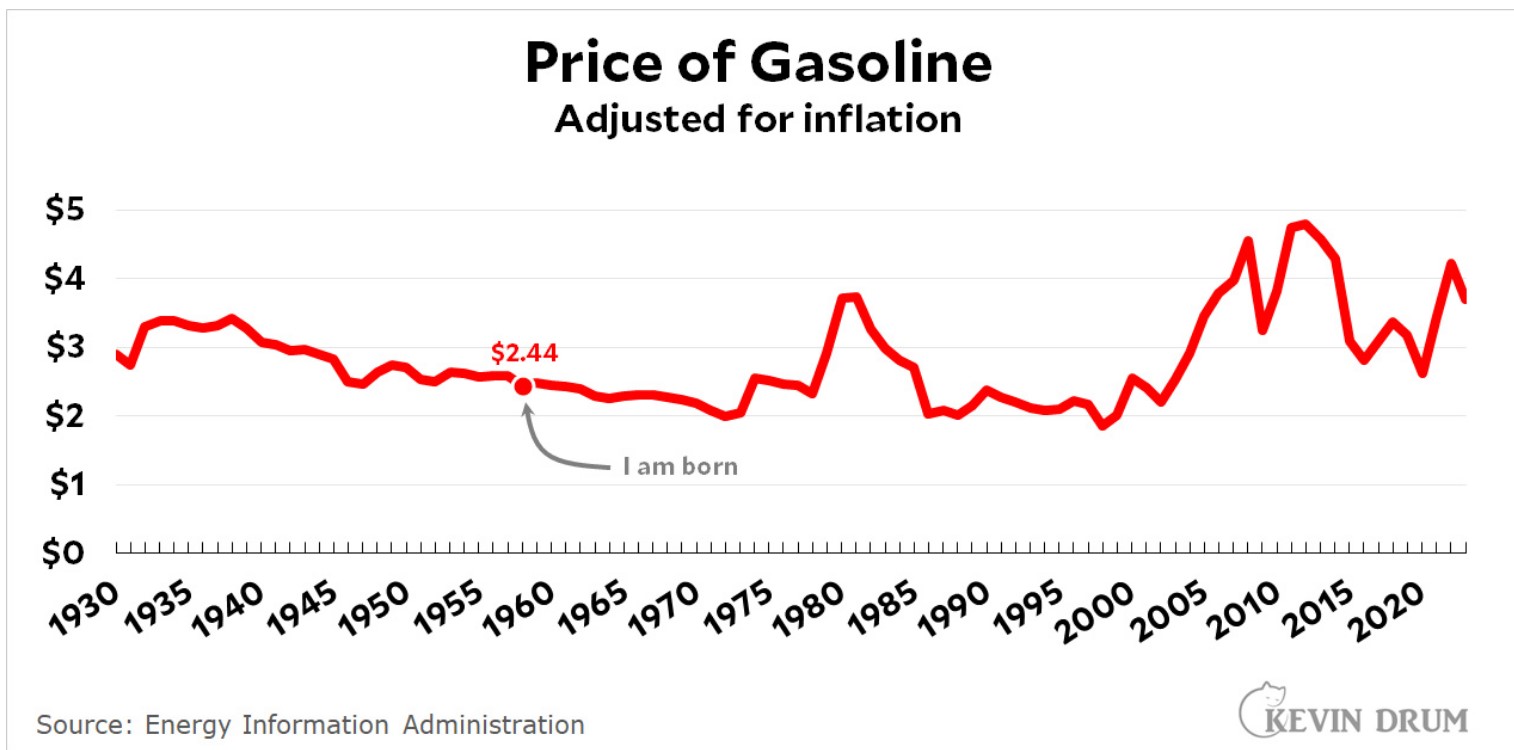

Gasoline Pricing during my lifetime

A bit of Kevin Drum: “Raw data: Gasoline during my lifetime,” jabberwocking.com, Kevin Drum.

I had just been discharged from Marine Corp active duty in 71, married, and bought a boxy Datson 510 to get around in the Chicago suburbs. Finished up at one college in 72 and started finishing my BA at another college 40-something miles away. The1.8 litre with a three speed Borg Warner transmission Datsun paid off at 30 miles to the gallon. I hauled gasoline back for the tractor I used to cut 30 acres of land. Now Kevin Drum . . .

“A regular reader asks if I can post a chart of gasoline prices over my lifetime. Of course. In fact, I can do better:”

I was born right in the middle of that warm postwar summer of ever-declining gasoline prices—which ended abruptly in 1973 with the first oil embargo. And then again in 1979 with the second oil embargo. And again in 2002-08 during the Iraq War. And again in 2011 because of turmoil in the Middle East. And then finally yet again in 2022 thanks to the Ukraine War.

Will gasoline ever get down to $2 again? Probably not. OPEC countries need a higher price than that to avoid bankruptcy. But it will probably recede to $3 one of these days.

Understanding Inflation using Gasoline Prices, Angry Bear, Daniel Becker

To me, this says as much about inflation as it does about the price of gasoline. But it’s also about America’s love of the ‘open road’ & its need for automobiles.

When I started driving in the late sixties, gas was at about 30 cents per gallon, sometimes a little less. On the price chart above (‘adjusted for inflation’) it was over $2/gallon.

‘The 1967 Oil Embargo began on June 6, 1967, the second day of the Six-Day War, with a joint Arab decision to deter any countries from supporting Israel …’ And make a few bucks.

OPEC decided that gas should at that point should cost about six times what it had previously, and that they should be paid in gold bullion. And they never looked back.

So now it costs about 13x what it did back in the day. But only twice as much on the chart above.

And cars cost about 15x-20x what they did back then. The first car I ever bought was a 1970 VW bug that cost $2K. I see a 1971 Bug available near here for $20K, and the final version from 2019, low mileage, for $37K (very different mechanically, but still familiar in appearance).

Fred:

And they would come out and pump your gasoline for $3.00 worth of gas.

@Fred,

“So now it costs about 13x what it did back in the day.”

LOL! And salaries, house prices and car prices are way higher than the late ’60s, too. As anyone with a rudimentary knowledge of economics knows, you can’t compare prices over time without correcting for inflation. Real dollars are what matter, not nominal dollars.

Am I the only one who wonders how/if the general inflation we have experienced is somehow tied to the Six-Day War. Houses in my town cost about 15x what we paid for ours in the late 70’s. That may be 20x more than at the end of the 60’s. Is the answer simply ‘just because’?

@Fred,

With housing, the answer is usually “location, location, location.”

That is very true. We have a house that has given us much joy, and much trouble over the years. Mrs Fred insists we would make a bundle if we were ever to sell, but neither of us wants to really. Too dang much trouble really.

I think you have a good point, similar to what Krugman had to say earlier this month. Drum’s regular reader probably thought that the cost of gasoline was sky high because he remembered cheaper gas. But the ability of the consumer to think about inflation over various timeframes is rather poor.

Are you saying I ought to be pretty pleased it only costs twice as much in inflated dollars instead of 13x as much in ‘uninflated’ dollars. Well, I am somehow grateful for being able to pay 13x as much. Will that suffice?

I hope everyone is earning at least 13x what they were making in 1968.

I was making about $8k per annum back then. I never in my life made $104k annually. Maybe a bit more than half that, before retiring, about 20 years ago.

As Chas Dickens wrote, paraphrasing, ‘If yer income is even just a little more than your outgo, then all is well. Otherwise, yer miserable.’

I object to the meaningless use of numbers and calling it data.

When you retired gasoline was 1.50 to 1.75 per gallon (unadjusted for inflation) or 5 to 6 times the 30 cent number you quoted. Your salary was 52K (or a bit more), 6 or 7 times the 8K you quoted. Since you retired, your assertion that your salary did not go higher is less than meaningless. It is absurd and misleading. Just the kind of numbers gaming I object to.

And I object to meaningless (i.e., unexplained) inflation. Fat lot of good that will do me.

@Fred,

If both your income and costs inflate at the same rate, why do you object?

I suppose, living on monthly soc sec and investment income, I’m only vaguely concerned about running out of funds. No sign of that yet. But this forum is about the hoi polloi, is it not? Presumably that’s how you’re looking at issues here also.

My late dad, not a well educated man, always thought that meant ‘the rich people’. Sounds like it should. Would that were the case.

🙂

I’d forgotten the 1967 oil embargo, I was still in high school and not paying attention.

The 1967 War and the “oil weapon” | Brookings

Turns out US, Iran and Venezuela replaced the oil denied to US, UK and W Germany.

Per Brookings oil demand rose rapidly from 1970, all us boomers buying big block V-8s! US went from excess to net importer in early 1970’s.

I recall gas shortages in summer prior to Yom Kippur war. The issue seemed to be permitting the Alaska pipeline.

“Let them freeze in the dark!”

The US wasn’t much of an oil importer until around 1969. If anything, we were an exporter before then. That might explain why so few people remember the 1967 embargo but so many remember the 1973 and 1979 embargoes. (There was also likely some shift towards suburban living in the 1970s as urban living became less the norm.)

I ignore the price of gasoline as I buy my motor fuel from Xcel Energy and they deliver it to my car via the EVSE in my garage.

@Dave,

I ignore the price of gasoline because (a) I don’t drive much, (b) I combine trips as much as possible, and (c) I drive a Honda Fit. Even if the (real) price of gas tripled, I’d still ignore gas prices at the pump. The knock-on effects of fuel prices on food and other commodities are more significant than your personal vehicle. Most new car purchases are SUVs and trucks. When that changes to subcompacts, you’ll know gasoline prices are high.

Joel:

We plan our trips, minimize the purchase of $5-gallon gasoline, and stick close to the speed limit. Such does not influence the “TBTFTO” drivers who believe it is their right to do as they please. Heck of a conflict on the roads today which we also avoid by timing our excursions. Thirty and 40 miles to the gallon on a 10-year-old Escape and an 8-year-old Volkswagon. Well maintained lower mileage vehicles. I do not feel like I want to buy new. The bigger one we use to cart things locally. The sedan is for road trips.

$5/gallon gasoline is still not enough of a high price to get them to slow down or lower their take-offs acceleration from a Stop sign or Red light. State highway is marked with crosses on its sides. Still no effort to go to intermodal ways of getting into the city. Just add another lane to the road.

I had something of a revelation this morning. You may remember that I approach economics as a devotee of physics, with the belief that econ is the ‘physics of the social sciences’.

I have not properly understood ‘inflation’, or at least what causes it. I started out with the assertion by economists that there is a ‘natural rate of inflation’. And that was to be taken as its cause. Not good enuf (for me). But I have never read a decent explanation. That may be because I haven’t looked hard enough.

But somehow this occurred to me this am. (You may say ‘Well, duh!)

In an economy, where spending money is natural, it is necessary for prices to increase continuously, in order to keep people consuming. If they weren’t, than you would postpone purchasing as long as possible, rather than stock-up, i.e. buy what you don’t need this very minute. Because that’s what you should do if the price tomorrow will be the same as today.

(We can’t have a robust economy where consumer demand is not ever present.)

I guess this is what is meant by ‘natural rate of inflation’. To a physicist, natural is associated with phenomena like gravity, elliptical orbits, tides, radioactive decay. Hence my confusion. If we didn’t have money we wouldn’t have inflation. DUH! So then the question becomes: is money natural? (Cut to the Star Trek universe?)

And in the end, even low rates of inflation compound continuously, so a VW Bug that cost $2K 50 years ago now goes for $20K or more today. If you can even find one to buy.

For example…

I am having trouble keeping my iPhone charged. Can’t do it anymore with a cable, because some tiny pins broke. This will get fixed eventually, Mrs Fred tells me, when the battery is replaced. Batteries don’t last forever. (Go figure!) But the battery in my phone is still at 90% ‘healthy’ – whatever that means. It means no new battery yet.

I need this phone to work for my medical library work. So, I need to use ‘wireless charging’ which is available with add-on expenses for such gear. Which I bought. Works great! Then I realized that that doesn’t last forever either. So I’ve had to buy spare wireless charging gear to keep around until needed. Ka-ching!

(Is this why Apple is just about the most profitable corp on the planet?)

@Fred,

What lasts forever?

Nothing. Protons probably. Stuff made from protons and other such ingredients, not quite so long. Stuff made from ‘long-chain’ molecules, not so long at all.

But that’s not the point. In the vaguely natural world of econ, you have to have money, people have to spend it, and do so regularly. Savings is the enemy! Keep interest rates loooooow to make us spend. Spend, spend, spend! Keep updating technology to make sure this happens.

@Fred,

“In the vaguely natural world of econ, you have to have money, people have to spend it, and do so regularly.”

LOL! Setting aside the question of what, exactly, is “natural” about the “world of econ,” why are people compelled to spend money just because they have it?

I don’t consume just because advertisers tell me to. YMMV.

Consume because it’s inevitable.

(That is, do yer part to keep society afloat.)

Not because advertisers tell you to!

Or, make it a point to buy NOT what they tell you to. Just buy!

Drive advertisers crazy by only buying stuff they don’t advertise.

That’ll fix ’em. Unless they figure out what yer doing and start advertising stuff you can’t do without. New microscopes maybe.

@Fred,

I approach economics as a devotee of physics, with the belief that econ is the ‘physics of the social sciences’.

There’s your problem.

Well, duh.

Wikipedia: From the ancient world (at least since Aristotle) until the 19th century, natural philosophy was the common term for the study of physics (nature), a broad term that included botany, zoology, anthropology, and chemistry as well as what we now call physics.

So, econ is the natural philosophy of the social sciences, if you prefer.

But, to make matters worse, the social sciences may not be sciences at all.

Even if they do falaciously employ a lot of math & statistics.

‘Everything transitory is only illusion.’ JW von Goethe.

@Fred,

As an actual, you know, PhD scientist, I’ve never been clear about how economics = physics. Many fields suffer from physics envy, but that doesn’t mean that they have achieved the predictive ability that physics has.

OTOH, I wouldn’t quote Goethe about economics *or* physics.

I am pretty sure that most physicists don’t either (and I just managed to eke out a BS.)

I think it has to do with the idea that econ is the underpinning of all the so-called social sciences, supposedly. As physics obviously is to all natural sciences.

And superior to all, no doubt, is mathematics. Of the theoretical variety.

In any case, I am personally pleased that I have worked out a satisfactory/sufficient explanation, however simple, for why we have to live with inflation. Why we are stuck with it. Why it’s inevitable, like the tides.

‘what, exactly, is “natural” about the “world of econ?’

A good question, which I attempted to answer.

Econ is essentially about ‘money’ & so it is obviously natural.

‘This is intuitively obvious to the most casual observer.’

A saying that was in frequent use by the profs where I learned physics, chemistry, math & even had semesters of economics, sociology. and psychology.

@Fred,

“Econ is essentially about ‘money’ & so it is obviously natural.”

LOL! Many (natural) human societies operated for millennia without money, and no other (natural) animal or plant species uses money.

How is that relevant?

I was trying to make the point actually that what is said to be ‘obvious’ often is not.

The Island of Stone Money

@Fred,

Cowry shells, Yap stone coins, gold pieces of eight, “money” is whatever people agree is a store of value that they’re willing to accept in exchange for goods and services. Money is a belief system shared between human beings. There’s nothing “natural” about it. Money is a quintessential example of the artificial.

So, there’s still no explanation for ‘natural rate of inflation’ I guess.

@Fred,

Supply and demand?

Sure. In the sense that if you want something from me, I’d be expected to ask for more than you are willing to pay. Somebody else might well take yer offer. If so, unfortunately (for me), no inflation ensues. So perhaps that doesn’t explain inflation either. I seem to have enuf Quaker heritage in my genes (& they supposedly felt bargaining was sinful) that I wouldn’t do that. I’d either not sell to you, or take what you offered. Where’s the inflation in that?

It seems philosophers in general (from Aristotle on) thought money was kind of peculiar, that bartering was natural perhaps, but exchanging currency was not. (I generally don’t put much stock in what philosphers have to say.)

The idea that ‘it’ll cost more tomorrow than it does today’ makes sense to me. We had some new windows put in last year. We were going to do ten, and they were going to cost a lot. We were told we could do half then, and half later, but the 2nd half would no doubt cost more. Ten cost way too much. We bought 5, did the other five this year, quite recently. Yep, it cost us about $1k more. That would be inflation, yes?

So, more of a ‘time value of money’ thing than ‘supply & demand’?

Again, the point here, and of this post overall I think, is that inflation is natural, and the reason for it (I say) is that prices going up are what motivates people to keep buying stuff. Yes, they need money to do that. For most, they have to keep working to do so.

When I was working, my employer for the longest stretch (almost 20 years) made it known that it was considered very bad form to be ‘grubbing’ for more money. They would give you whatever increases they could handle (& what they felt you had earned) and you were to just keep your shoulder to the wheel as it were.

To that extent, inflation precedes wage/salary increases.

My employer back then was ‘dead-set’ against unions & would have us know, subtly perhaps, that this was why they were ‘generous’ (or so they said) about such increases. Even if they weren’t particularly perhaps.

@Fred,

“When I was working, my employer for the longest stretch (almost 20 years) made it known that it was considered very bad form to be ‘grubbing’ for more money. They would give you whatever increases they could handle (& what they felt you had earned) and you were to just keep your shoulder to the wheel as it were. “

LOL! And for 20 years, you accepted it. No prob. Other folks might have priced their labor differently and quit for a higher paying job. Also no prob.

Oh, they did. There were half a dozen competing companies in the region, all in the same space. All were bought out and/our went under. Had to pay too much in wages & salaries I guess.

@Fred,

“There were half a dozen competing companies in the region, all in the same space.”

The phrase “in the region” is doing all the work in that sentence. When you want to make a big change, ya gotta move from the ‘hood.

https://www.youtube.com/watch?v=65rWPDimvyI

For various reasons, we were not going to leave New England.

Mrs Fred did entertain taking a job in Rancho Cucamonga or some such place once upon a time, and I would have been expected to follow along, but that was not to be.

In any case, your point seemed to be that if I wanted to get higher pay, I could go elsewhere. Indeed I could. Others did. In the end it did not turn out well. I could have taken my chances in Rancho Cuckamonga.

What does that have to do with anything?

Economics is about human behavior, so it is more like anthropology than any other field. Accounting might have something in common with physics in that it has a set of conservation laws, but a lot of economics violates all sorts of accounting principles. I’m with Jane Robinson. When the sciences started gaining credibility, the ruling class would pay you to pretend economics was a science to further their interests.

The sine qua non of science is that there is a self assembly process and that process can be quantified into mathematical relationships with prospective predictive capability.

The asset debt macroeconomic system has the characteristics of a self assembly process.

If by “Natural rate of inflation” you mean a steady state inflation rate, then that would be related to NAIRU.

See here for source quotes: https://www.economicshelp.org/blog/glossary/the-difference-between-the-nairu-and-the-natural-rate-nr-of-unemployment/

NAIRU – Non-accelerating Inflation rate of Unemployment. This is the level of unemployment that is consistent with no acceleration in the inflation rate. The NAIRU is related to the short-run Phillips Curve. If unemployment rises, inflation falls. If unemployment falls, there will come a point, where inflation starts to increase.

Long term, the natural rate of unemployment is determined by structural unemployment, e.g. mismatch of skills, frictional unemployment and geographical immobilities.

But this may change because of changes in market structure and frictions.

It was always assumed the US had a natural rate of unemployment of around 6%. However, in the 2010s, unemployment has fallen to 4% without any noticeable increase in inflation.

The Philips Curve may also change over time.

https://www.stlouisfed.org/open-vault/2020/january/what-is-phillips-curve-why-flattened

Given that the FED can set interest rates to drive inflation rates to their preferred value, then the “natural rate” could be understood as whatever the FED wants it to be.

Again, market structures and frictions will delay the inflation rate changes (due to interest rate changes) on the inflation side also.