Why Isn’t The USA in a recession ?

Oddly I am back here posting. Even more oddly I am posting on the topic I am paid to address. I start by noting two things. About one year ago, many macroeconomic forecasters predicted that a recession would have started by now in the USA. I forget who placed the probability at 100%. In spite of sltightly disappointing 0.4% (1.6% if annualized) real GDP growth in the first quarter of 2024, we are not in a recesion. What went right ?

The presumed cause of a recession was the sharp shift to contractionary monetary policy in a effort to fight inflation.

In this post, I will focus mostly on domestic demand. Briefly, high interest rates can cause a recession by causing an appreciation of the national currency which causes a sharp decline in net exports. This may have been important in 2981-2, but it usually isn’t a huge deal for the huge USA. In any case exchange rates haven’t shifted much, nor have real exchange rates, because most US trading partners have had inflation similar to US inflation. I think that’s the explanation. The shift to contractionary monetary policy occurred at roughly the same time in many countries, so there was not much shift in interest rate differentials of exchange rates.

So I mainly look at domestic demand (AKA absorption). The larges element is consumption which has continued to grow. Consumption mainly tracks disposable income with the rest of variation explained by changes in wealth . Wealth is high due to high house prices and the (illusory wealth) from the national debt. No surprise. Government consumption plus investment remains stable. The issue is investment which should decline with high interest rates. I will disaggregate investment.

FIrst it is the sum of fixed capital investment and inventory investment. Inventories follow final sales so inventory investment is (almost entirely) expalained by the change in final sales, which have grown. No surprise.

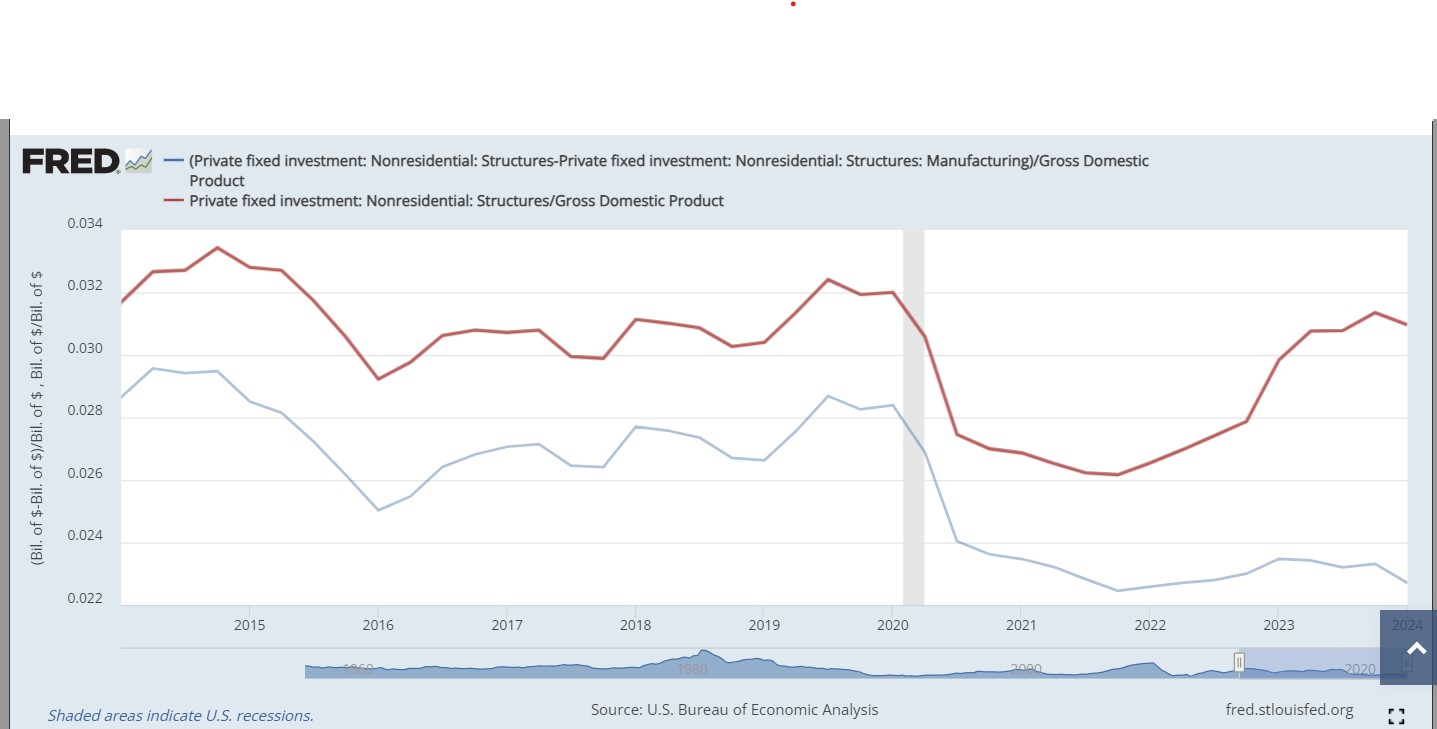

Fixed capital investment is divided into residential (the real puzzle) and non residential. Non residential investment is divided into investment in structures and investment in equipment and software (I am old enough to remember when this was called investment in equipment). The cost of investing in equipment and software is almost all depreciation (not interest) which is almost all due to techological obselescence. It tracks the change in GDP which has continued to grow, so no surprise there.

The puzzle is why has investment in structures held up. I will discuss non residential structures first. A fairly small part of that is investment in manufacturing structures AKA factories. This is a small amount of demand, because factory buildings are large but simple. However, the increase has been dramatic with investment in manufacturing structures roughly doublin. This can be explained by the incentives in the CHIPS act and the IRA – fiscal policy not working as aggregate demand but as incentives for private demand. In fact that is almost the whole story. Other non residential investment in structres fell dramatically during the Covid epidemic and then remained low. This makes sense as people worked from home reducing demand for office space, and purchased things to be delivered reducing demand for retail space (Amazon structures keep appearing in remote places but, like factories they don’t cost much).

The current level of investment in structures other than manufacturing structures at less than 2.4% of GDP is very low (trough of great recession low, commercial property bubble burst in 1991 low — sorry I didn’t show those years). It hasn’t declined after the shift to tight monetary policy. I guess these are structures that are really needed (new shopping centers in new housing developments) and the increased cost from increased interest rates are passed on to consumers.

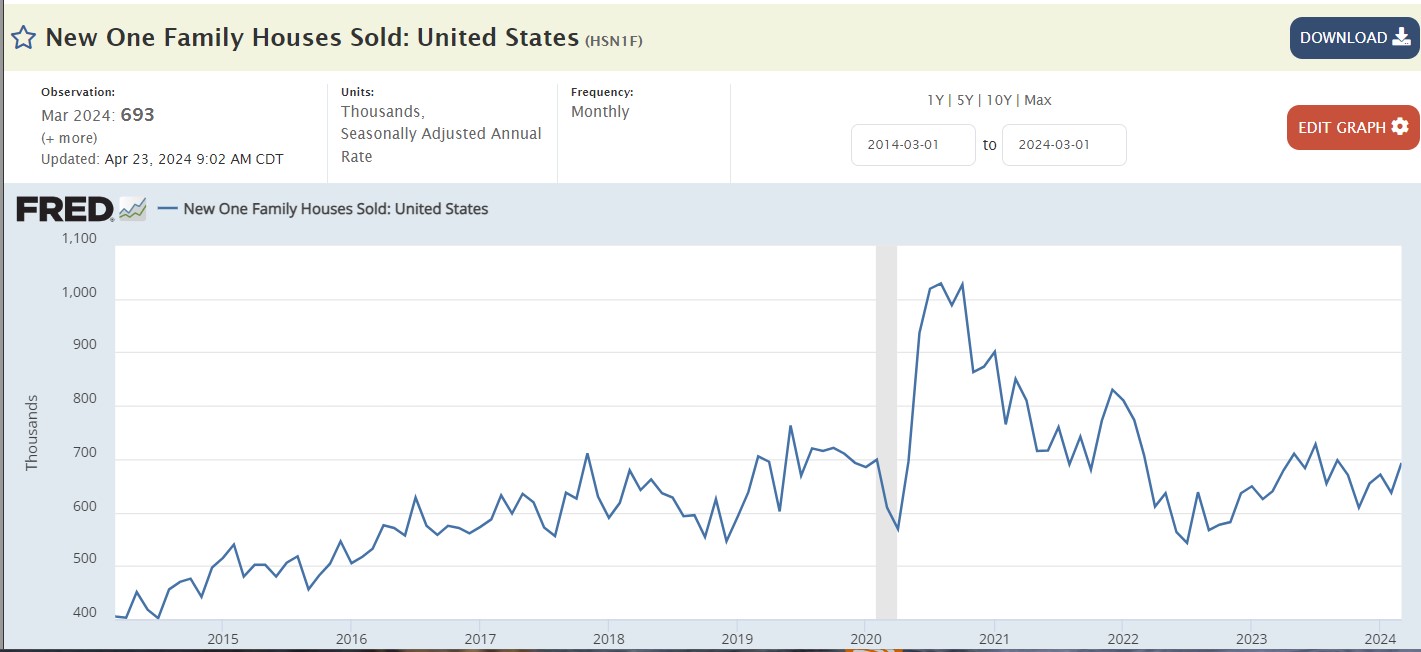

The remaining huge puzzle is residential fixed investment. Why are people buying houses ? The relative price is very high – higher than in 2006 at the peak of the (last???) bubble

But that’s not the half of it. Mortgage interest rates are very high (and long term expected inflation isn’t). Yet new homes are being purchased.

I don’t understand this (which is key). I have some guesses. My first guess is that people are willing to pay the huge prices (and huge interest on the mortgage) because they are convinced prices are going up so it is a good investment. This could be yet another bubble or could be a rational forecast. There are other possibilities.

Work from home creates demand for home offices. This is an explanation of the huge increase in rents on newly signed leases in 2021-2022 (still working through to average rents which explains a lot of persistent inflation). It also applies to owner occupied housing in two ways. People might want a whole house not an apartment to have a home office. Also, high rents encourage buying even if the price is high (this isn’t enough — a 20% increase in rents does not make buying now sensible without something else going on).

Two other things. The prolonged period of low construction post great recession means that square feet per adult are way below trend. It might be that a housing shortage implies people who need some space are buying even with high prices and mortgages.

Finally, Brad DeLong had an idea (I don’t know if it is on his substack). High mortage rates lock in people paying low interest mortgages. This can include boomers who would otherwise move to smaller houses. My reaction is to ask which boomers still have mortgages. But some can if, for example, they moved and each time moved to a larger house. Or if they moved from a depressed area, selling a house for very little and bought a much more expensive house in a booming area. Or, especially, if they took out home equity loans. It still seems odd to me that equity in a large house would not make it possible to buy a small house without a new mortgage. There is also a possibility that people who move from a house with a low interest rate mortgage don’t sell but rather rent it taking advantage of high rents (I know a couple who are doing this).

In any case, I find the determination to buy a house even now when everything is against it puzzling

“It still seems odd to me that equity in a large house would not make it possible to buy a small house without a new mortgage.” Sure, that’s possible. We tried to do this. But you have to look at what you get when you downsize from a larger house to a starter house in a less desirable neighborhood.

What’s missing are Honda Accords for the housing market…small, feature rich homes near good medical care, shopping, and transportation in attractive developments. Builders generally do not build this type of housing. And if you can find one, it’s likely to cost more than the not- so-old, larger house you’re trying to leave. Or it’s way out in the boonies.

I raised this problem 20 years ago with the city council in our mid-sized city…and nothing was done, either by the city or by local developers.

We finally gave up and eventually lucked out by finding a very expensive, feature-rich rental in a continuing care facility, a type of high-quality housing that is also in short supply.

John:

I sat on a Planning Commission and we approved a build on a couple of hundred acres which was mixed between condos, small homes, and the much larger ones. An old harness racing track. we established the lot sizing so it would not be a pile on by the developer. Pre-2008 and things went awry. I had to leave my position for a while. The developer went bankrupt. A new developer came in and wanted alterations to the development. The Commission caved. This was in Livington County Michigan, the richest county in Michigan and just north of Ann Arbor.

They altered the small housing and lot build to the larger home, etc. I was pissed when I returned. It was a whole concept wasted due to old ideas and a lack of vision as to what was needed.

The older I get, the less I trust my judgment on concepts like “boonies”. You live in a place and think “those guys way out there are are nuts to be so far from medical services, good grocery stores, and 15 other things” and 5 years later you figure out you are further away from those than they turn out to be. Doesn’t mean you want to live there, but my 65+ year-old opinion of an area isn’t as important as what 30 year-olds are thinking.

eric

maybe not, but my considerably older opinion is the same as yours and has been since i got old enough to know enough to have a better sense of proportion.

meanwhile i think the main article here is too abstract to mean much of anything to anyone but an economist who doesn’t get out much. and the opinions about house buying too personal to mean much except as a rough guide to what other people are thinking in case you (I) missed something.

we actually sold a house (large) in an area where house prices were appreciating (though today thats not the case) and bought a smaller house with no mortgage (in an area where property values were lower, and at the time were slightly growing, but now are also depreciating with no mortgage). sold that before the depreciation took hold. now no longer in owning a home. most of the time the largest investments by the majority of people (house/vehicles) are depreciating and sales are way down

dw:

In and around 2008, we were at breakeven in mortgage to sale. 2021, we sold and received a healthy amount of funds after expenses. If you go into this thinking you are going to make a ton of money, you will not do so more than likely. A return of 2-3 percent may be more likely. Interest rates are a real killer in getting returns. We were at 4% after the end of a seven-year ARM. Today, we are at 2.6% assumable. About half of our payment goes to principal. Most of the funds from the sale went to investments. Houses typically are not investments. They are a cost of living.

I agree with your comment.

Buying a house is buying an option on one’s future rent. Rents are going up, as they have been for decades. Even with high interest rates, that option is a good deal. It’s a hedge against even higher interest rates. If rates fall, one can refinance and buy an even lower rent.

You could argue that rents are really high now, but they could go down and make the fixed rent option a liability. This would be a hard sell. There are very few people living who remember rents falling for more than brief periods.

Kaleberg

agree about the chance of rents going down. but there are more things in life than money. they used to be free, but you can’t count on that anymore either.

so far i have been lucky. not so my formerly rich daughter. all she has left is some property she built up until she can no longer afford the taxes on it.

JohnH

I like your thought about Honda houses. I came at something similar by obsdving the very large number of people living in cars and in tents around my little city.

Rather than build “homeless shelters” why not use the money to build homes. Make them available to the homeless for a “forgivable loan”…thank you Don Trump. that could be converted to actual ownership, or sale to poor but not yet homeless people. Creating along the way a reserve of ‘government owned” housing for emergencies like fire , flood, and insurrection.

that reserve might ten to keep housing prices and rents fair and reasonable and discourage predatory banks and predatory (corporate) landlords.

yes to cost of living. though that is not what they told me when i bought my first house. thing that amused me was that i had to sell that house (change of job) six months after i bought it. i did not expect to recoup my down payment (investment) but the realtor asked me how much i needed to get to be happy. i suggested a number much higher than i expected to get. and he sold it for exactly that much. which i used as down payment for my next house, for which i paid about 10k more than i expected, at 10% interest. i paid off that mortgage in two years. now i have a house that is worth six times what i paid for it… but i could not get nearly as good a house in as good a neighborhood for that much. so maybe it was an investment after all

anyway, it keeps me off the streets. my daughter is not as lucky as i am. her property is now worth twelve times what she paid for it. but she has only herself to blame. when times were good she improved it, and now that times are bad for her she can’t afford the taxes.

sorry for starting the housing boom and causing everybody so much trouble.

my comment at 1:01 was in reply to bill at 10:48

my comment to JohnH has typo “tend” not “ten.”