September industrial production turns down, but no major cause for concern

September industrial production turns down, but no major cause for concern

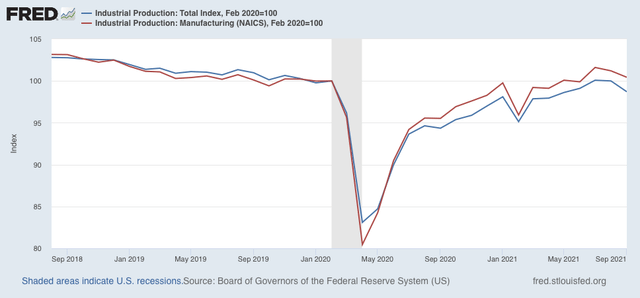

Industrial production is the King of Coincident Indicators. This morning’s report for September was negative, and August was revised downward, taking total production back below pre-pandemic levels.

Total production decreased -1.3% in September, and the manufacturing component decreased -0.8%. The August reading for each was revised downward by -0.3%. Nothing particularly special about that; in fact, the manufacturing component was a little weak compared with most recent months. Additionally, the July numbers were revised slightly (not significantly) higher and lower for each, respectively. As a result, manufacturing is now only 0.4% above February 2020, and total production is down -1.3% compared with just before the pandemic:

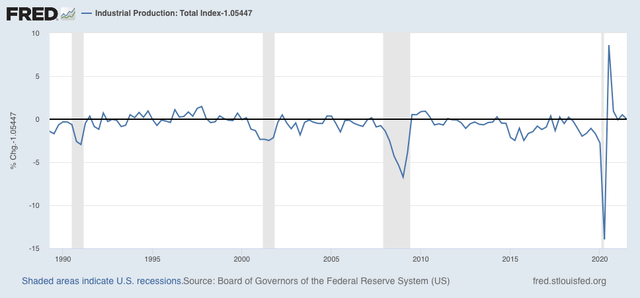

Needless to say, this is very much at odds with the continuing very positive ISM manufacturing index readings which we have gotten every month this year. The Fed regional manufacturing indexes, as well as the Chicago PMI, also remain positive, so I am not terribly concerned about one poor month (which needless to say may also be revised!). This morning’s report is probably going to prompt some scary downward revisions to forecasts of Q3 GDP, which will be released one week from Thursday. But when we look at quarter-over-quarter numbers, industrial production is still up 1.1% from Q2 of this year. In the below graph, I’ve subtracted that number so that it norms to zero, to compare that increase with the past 30+ years:

As you can see, while it isn’t the strongest reading, it is higher than most quarters during the 3 expansions since 1989, and is nowhere near recessionary. So, while we’re almost certainly going to see a sharp *deceleration* from the blockbuster last several quarters in q/q GDP next week, in absolute terms I do not see any particular cause for concern.

Dogon:

I do not do stupid here at the Bear.

the drop in manufacturing looks like a seasonal adjustment payback to me….the July manufacturing index increased by 1.4%, largely due to a seasonally adjusted 11.2% increase in the output of motor vehicles and parts, because “a number of vehicle manufacturers canceled their normal July shutdowns because vehicle assemblies had been constrained by a persistent shortage of semiconductors over the prior months”; without the large July seasonal adjustment, i figured actual vehicle assemblies fell by around 20% in July…here’s my discussion of that here at AB: https://angrybearblog.com/2021/08/industrial-production-rose-0-9-in-july#comments

here’s the “Seasonal Factors for Domestic Auto and Truck Production” from the Fed:

https://www.federalreserve.gov/releases/G17/mvsf.htm

i had expected a reversal of most of that +11.2% in August, but August took back less than half…so i figure September’s drop to be the rest of it…

seasonal adjustment aberrations don’t change what actually happened; they just cause it to be shifted around from one month to another… what i’m pointing out, i guess, is that for the automotive component of manufacturing, September wasn’t anything special; it’s been in trouble all year…

while i’m here, i should also explain why i don’t put much stake in the widely followed manufacturing diffusion indices NDD cites:

the PMIs, and all other such indices that i know of, are derived from a survey of purchasing managers or other executives who are in a position to know the details of a business’s condition…they are queried as to production, new orders, employment and several other business metrics with the possible responses simplified to “getting better”, “getting worse”, or “about the same”…responses indicating improvement add 1 to the index; those that are about the same add 0.5, and those indicating weaker conditions add 0….the diffusion index is then constructed by multiplying the resulting total by 100 and dividing by the number of responses…there is no query as to the degree that conditions might be getting better or getting worse…hence, the response from a company that might be doing much better would be offset by one doing just slightly worse…furthermore, there is no weighting of the size of the companies whose purchasing managers are members of the Institute for Supply Management; the response from Ford’s purchasing manager counts the same as the response from Podunk Tiddlywinks…hence we might have a strongly positive PMI if several tiddlywinks companies had a little bit better month in September than they did in August, even if Ford and GM are doing much worse…

since the PMIs are released in advance of the hard data collected by government agencies, they’re probably useful as an advance indicator of industry sentiment, and possibly might indicate which direction the actual data for the month might turn…but other than that, they’re really no more indicative of the hard data than a consumer confidence survey is of retail sales…