While house price gains continue to go nuts, housing remains much more affordable than at the peak of the bubble

While house price gains continue to go nuts, housing remains much more affordable than at the peak of the bubble

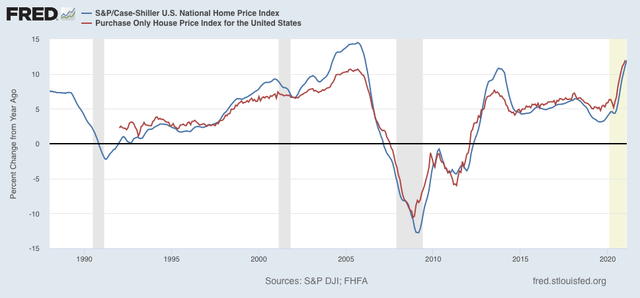

The boom – and maybe insanity – in house price gains continued in February, as both the Case Shiller and FHFA house price indexes increased roughly 1% just since January! The YoY increase for both was almost exactly 12%, as shown in the graph below:

While the YoY increase in house prices matches those of the bubble peak, and are, to say the least, not sustainable, they aren’t quite the crisis that they appear at first glance.

While the YoY increase in house prices matches those of the bubble peak, and are, to say the least, not sustainable, they aren’t quite the crisis that they appear at first glance.

That’s because mortgage rates over the 12 month period declined, which makes the affordability of monthly mortgage payments considerably less intense. And in real terms compared with income mortgage payments are still well below their level at the peak of the housing bubble.

Since the peak of the housing bubble in roughly September 2005, house prices increased roughly 33% as of February 2020. With the 12% further increase in the past 12 months, they are now almost 50% higher than in September 2005.

But what is *very* different is mortgage rates.

Here is the average rate for a 30 year mortgage in each of the 3 months:

9/05 – 5.77%

2/20 – 3.47%

2/21 – 3.08%

That means that in nominal, not-inflation-adjusted terms, the monthly mortgage payment in February 2020 is only 2% higher than in September 2005. In February 2021 it was only about 8% higher, even taking the big appreciation of house prices into account.

Over the same period of time – since September 2005 – average hourly wages are up 55%. As of 2019 (the last available measure), median household income was up 48%.

In other words, home buyers in the aggregate have about 50% more income to pay a mortgage bill less than 10% higher than it was in 2005.

In sum, although monthly mortgage payments have increased by about 7% since December, when rates averaged 2.68%, even with the huge price increases that continued through February, housing remains much more affordable than it was in 2005 at the peak of the bubble.

What you have missed is that the pre-2008 housing bubble was driven almost entirely by low monthly mortgage payments (much lower relative to income than they are now). That coupled with the willingness of junk bond investors to finance tens of millions of loans to people who were not required to document income or assets and who put no money down for a house appraised above value.

Monthly payments were extremely low because the borrowers were allowed to borrow more each month to cover the payments. What could go wrong?

Below is a link to an article from 2006 extolling the virtues of the market “innovations” that made this miracle possible.

https://www.robertstoweengland.com/writer/19-the-rise-of-a-private-label

“Product innovation has resulted from two developments, the first is mortgage consumers looking for new low-payment mortgages to help them afford rising home prices. The other is the growing willingness of investors to fund the new types of mortgage products that lenders have developed to meet this need.

Mortgages that offer low monthly payment options often do not amortize the principal balance on the loan, and may even negatively amortize. These products –interest-only (IO) mortgages and option adjustable-rate mortgages (option ARMs)–are the primary generators of gains in market share for private-label issuers.”

“Mortgages that offer low monthly payment options often do not amortize the principal balance on the loan, and may even negatively amortize. These products –interest-only (IO) mortgages and option adjustable-rate mortgages (option ARMs)–are the primary generators of gains in market share for private-label issuers.”

So everyone lives in a $million home now. Property taxes, that is the middle class wealth tax, will be going up substantially for most people. Funny, it didn’t take politicians or the electorate voting for tax increases. Just a paper increase in the value of your home. Meaningless if you don’t intend to sell. Worse than meaningless if you do because you’ll have to buy another. Not really sure who benefits from this? Down the line maybe the schools?

what happens to housing prices when interest rates rise and mortgage payments can no longer support today’s prices?

rjs:

Like I mentioned, the prices will collapse, people may go underwater on their house, Value will be less than equity, there will be a glut in the market place, builders may go bankrupt. House appraised at $300,000 (which was probably overpriced too), bidder bid $30,000 more. Bidder has to make up the difference over what the bank will loan. This is happening in Phoenix right now.

One model of a home we could buy for $280,000 1-1/2 years ago is going for high $300s or over $400. Builders are doing lotteries for lots and telling you what home can go on the Lot and what is on the inside of the home. It is driving up prices. You can not pick land site or what a home looks like on the inside.

Rjs,

Same thing that would happen in the bond market. If you have to sell you’re screwed.

I remember when any mortgage rate in single digits was really, really good. Today’s rates are almost unbelievable. When people talk about 4 or 5 % rates putting a damper on sales I have to laugh. Of course, way back when wages were a lot better for the average working stiff.

I understand what all of you are saying. today is a really good time to be wealthy.

I bought our forever home in April 2004. It is our forever home not because it is so grand, but because it will be needing more fixing up forever. Paid if off in 15 years. Now we can afford to get more of the work that it needs done. Our home is a 2600 square foot 1959 brick built ( not veneer) ranch plus a rough basement. The location is irreplaceable with nearby access to the E/W Interstate 64, the 295 Richmond beltway, and the 895 E/S connector. There is a YMCA just one block away and a VFW hall sort of next door. Thanks to an idiot developer from NJ we now have two abandoned homes to our east. Whiteside Road is to our west.

Home trading is a better way of life for real estate agents than homeowners. My old boss lived in the only home that she and her husband ever bought long enough that their kids were grown before they could afford a bigger home and then they did not need to downsize. Apparently some people like moving more than she and I.

That real interest rates are very low is one element in explaining why higher housing prices may be rational. Another is that real rents today are higher than they were back in say 2006.