Average real wages rise for 12 straight months as prices decelerate faster than nominal wage growth

by Elise Gould

EPI

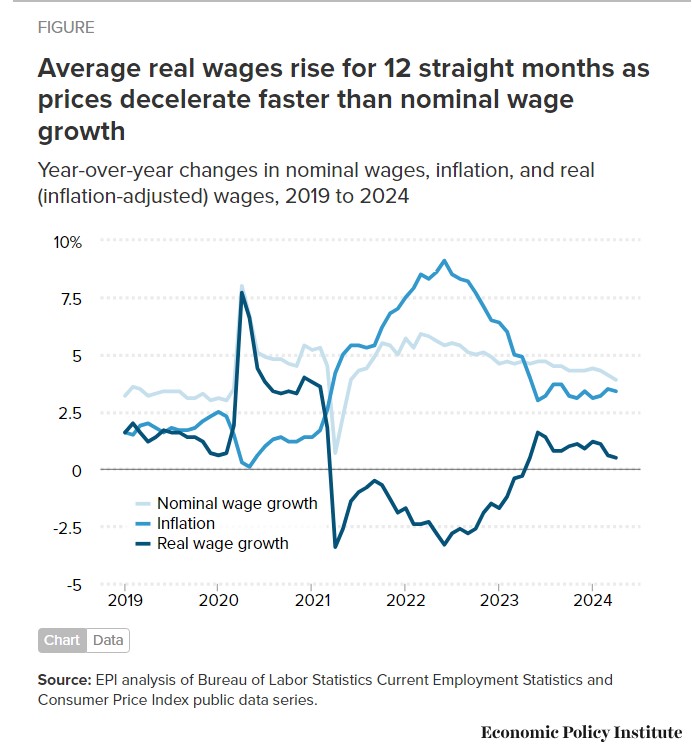

Average hourly wage growth has exceeded inflation for 12 straight months, according to new Bureau of Labor Statistics data released this morning. This real (or inflation-adjusted) wage growth is a key indicator of how well the average worker’s wage can improve their standard of living. As inflation continues to normalize, I’m optimistic more workers will experience real gains in their purchasing power.

The dark blue line in the figure below plots year-over-year real hourly wage changes for all private-sector workers.

Year-over-year real wage changes measure the percent change in wages in one month compared with the same month a year prior. Monthly or even quarterly changes in wages are notably more volatile. While shorter-term measures are valuable to capture very recent changes, this year-over-year measure provides a more stable and longer-term perspective on the state of real wage growth.

As the figure shows, average real wages rose sharply at the onset of the pandemic, but it is because the bottom dropped out of the labor market when millions of lower-wage workers lost their jobs. Average real wages then fell sharply in the pandemic recovery as many of those lower-wage workers returned to work, pulling down the average. Real wage growth continued to decline as inflation rose steadily due to supply chain bottlenecks and shifts in consumer demand. As quickly as inflation rose—peaking at 9.1% in June 2022—it fell, hitting 3.0% in June 2023.

Nominal wage growth is the year-over-year growth in wages, not adjusted for inflation. The Federal Reserve looks at that measure for signs of wage-driven inflationary pressures. What’s clear is that nominal wage growth has been steadily decelerating over the last two years, as shown in the lightest blue line in the figure. The latest data find nominal wage growth at 3.9%, just a bit above the 3.5% long-run target for wage growth that is consistent with the Fed’s inflation target (2.0%) plus productivity growth (likely around 1.5%).

While nominal wage growth is an important indicator for Fed policymakers to measure signs of labor market slack and inflationary pressures (and these remain relatively muted), real wage growth is what matters for workers’ living standards. On average, the data are clear: wages have been beating inflation for 12 months now.

Looking beyond the average, production/non-supervisory workers—roughly the bottom 82% of the wage distribution—started seeing positive real wage growth two months earlier in March 2023, now 14 months in a row (not shown). It’s not surprising that those more moderate-wage workers experienced faster wage growth as other research has shown that lower-wage workers had the strongest wage growth during the pandemic, which is quite unusual in recent U.S. history. These gains for workers are encouraging—and something I hope continues.

Angry Bear . . . Any increase in Social Security withholding staves off depletion of the trust fund. On a 40,000 annual salary, 1/2 of 1% withholding is $200 annually for a person and the same for a company. Not rocket science.

Before we get too excited about “how well” labor has been doing, median usual weekly real earnings are virtually flat—1% above where they were before the pandemic: https://fred.stlouisfed.org/series/LES1252881600Q

We all know the problems with averages…

New Deal democrat covers nonsupervisory real wages weekly, monthly? Last commentary:

Real wages, payrolls, and consumption vs. employment, and their forecast implications: April update – Angry Bear.

First, here is real average hourly wages for nonsupervisory workers. In April, nominal average wages increased 0.2%. Since consumer inflation increased 0.3%, real nonsupervisory wages declined -0.1%, the third monthly decline in a row:

Real nonsupervisory wages are up 2.8% since just before the pandemic, and while the sharp increase in 2020 can be discounted due to compositional effects (many more low wage service workers were laid off during the pandemic closures than more highly paid office workers), still real average hourly wages have made no progress at all since July 2020.

On the other hand, on a YoY basis, real average hourly wages are up 0.6%, which historically is not bad:

For the real amount of wage income available to the American working and middle class as a whole, we turn to real aggregate payrolls. Because the number of hours worked actually declined during April, these only increased 0.1%, so in real terms they declined -0.2%:

With the exception of the pandemic, these have always peaked between 4 and 10 months before the onset of recessions. As the longer historical graph below shows, one month decline is not unusual, but obviously if this continues for several more months it would be of increasing concern:

On a YoY basis, these are up 2.1%. Typically they have sharply declined to negative territory coincidently or very close thereto the start of recessions:

There is no sign of any such sharp decline at present. So these remain a very positive sign for the economy now.

You can read the rest at the link which is also a part of Angry Bear.

John:

I do not think we are too excited as to Labor as we are one the edge of going into recession. The economy is doint well, prices are too high due to manipulation, and there are other reasons. We just have not slipped off the edge yet,.

My experience for the past couple years is that a very big part of the perception of high prices this time is centered on food. If the wage increase is measuring against a price inflation index without food, might miss a big area of concern.