Joe Biden’s roll out of a new student loan forgiveness plan

The Biden administration will soon roll out a new student loan forgiveness proposal that could impact millions of Americans. For years, Joe Biden has been against Student Loan forgiveness. Now he is seeking forgiveness for making student loans totally unforgiveable.

The proposed student loan program is smaller in scope than President Joe Biden’s first education debt relief plan which the Supreme Court ultimately blocked. Rough estimates by higher education expert Mark Kantrowitz, the new aid package could still forgive the debt for as many as 10 million Americans.

The Wall Street Journal says President Joe Biden is planning to provide details of his new debt forgiveness plan during a speech Monday (April 8?) in Madison, Wisconsin. The timing of this corresponds ahead of the election in November. In a recent survey, almost half of all voters (48%) say canceling student loan debt is an important issue to them and will help them decide who to vote for in the 2024 presidential and congressional elections.

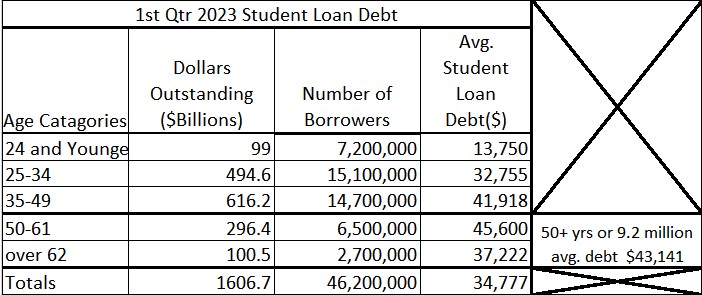

Mid 2023, June to be exact, Angry Bear posted about student loan debt. 45 and Now 46 million strong Owning Student Loans 2023 – Angry Bear. We presented this chart depicting the numbers of people by age and the amount of student loan debt of each age bracket. Portfolio-by-Age.xls (live.com).

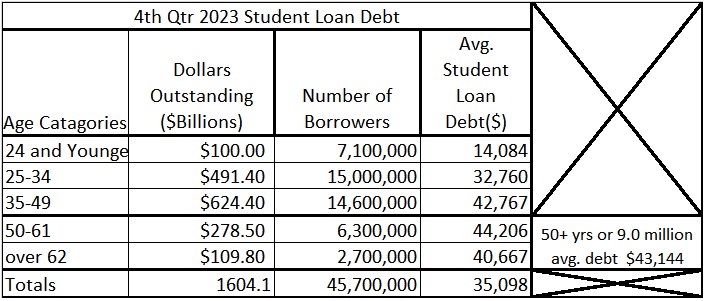

With the latest data, I have updated the chart again showing numbers and the amounts owed by age bracket and in total. Again as taken from Portfolio-by-Age.xls (live.com)

As you can see, the total numbers of borrowers did drop by 500,000. This is not a lot. However, as more people drop out, others just start college. We can see a drop from the 1st Qtr. of 2023 to the 4th Qtr. of 2023. The numbers in each age bracket have decreased.

If you click on Portfolio-by-Age.xls (live.com), you can also compare 2018 to 2023. The numbers for 24 and under in college has decreased by 1.5 million. The 25 to 34 year old age bracket also saw a small decrease of 300 thousand. It may be, people becoming of age are avoiding college and its costs. This does not bode well for colleges. Too soon to tell what the outcome will be.

The president’s Plan B for student loan forgiveness will likely target several groups of borrowers, including those who’ve been in repayment for decades and people who are experiencing financial hardship.

Immediately after the Supreme Court struck down Biden’s $400 billion student loan forgiveness plan last June, the administration began working on a revised assistance package. The administration believes its updated plan will survive legal challenges this time for several reasons. One, it’s far narrower than its first attempt, which impacted as many as 40 million Americans.

Why would Biden concentrate on those who have been in repayment for decades? In an earlier commentary “45 and Now 46 million strong Owning Student Loans 2023,” Angry Bear, I was discussing the issue of age and paying back at 50 and 62 years of age. Some verbiage . . .

Age is a factor and those in the 50+ grouping have the greatest overall average debt. If one could even snare a 5% interest loan on an average $45,000 debt, it would take a 50+year old 13 years to pay the loan off at $400 per month. At 62 years old and snaring a 5% interest loan and paying $400 per month, a person would need 10 years and would be 72 years old. This is calculated at 50 and 62 years old. Think older and is it possible to do? Not likely.

Student Loans are not that friendly. They are meant to hold student captive. Unless there is some type of relief, many will be captive for a lifetime. Could they pay it back? Four hundred dollars a month is a considerate chunk of money coming out of a budget.

You can read the rest of “45 and Now 46 million strong Owning Student Loans 2023 – Angry Bear” yourselves. I do not buy the argument SCOTUS comes back with on student loan forgiveness. If such is the case, Congress should eliminate their retirement funding. These loans are deceptive and the only loans to which bankruptcy is not allowed. For this issue, we have to look for further than Joe Biden and his campaign against student loan forgiveness.

Biden administration will soon roll out a sweeping new student loan forgiveness plan

“Biden administration will roll out new student loan forgiveness plan,” cnbc.com

Why would a 50+ take 13 years to payoff the 5% loan at $400/month but the 62 year-old gets it done in 10 years? Are the loan amounts different? It says $45k for the 50+ but is not specified for the 62. If not, does the older borrower get some sort of programmed credits reducing their obligations? Also confusing is that 62 is part of 50+.

Okay, I think the presumption is to use a rounded number from one of the tables where 62 has lower loan amount. In any case, what can be done to reform this loan business to get out of these problems in the future? Is the system continually creating new stressed-out borrowers? Maybe a truncated guarantee scheme: first $10k has full government backing, but after that initial amount the borrower is in some manner obligated to convince lenders that continuing amounts are a good risk to run. Feels like a lot of people only wake-up that they over-borrowed relative to what it actually can do for them after they get in way too deep. Lenders think ‘this has a backstop, so I don’t care much if it is kind of ruinous for the borrower’. Nothing is perfect, but some kind of earlier “reality check” could prevent a lot of future stress.

@Eric,

How about changing the law so that student loans can be discharged through bankruptcy, like other loans? That way, the risk is on the lender, as it should be.

Joel

yes, but see my “welcome to America” comment on HOA’s above: America;s go-to business model is “consumer fraud.” The borrower in the School Loan business is no match for the lender, or the “school.”

Eric seems to think that wiser choices by the borrower is the solution. It is not. The borrower doesn’t even know he has a choice. Innocent buyers are the mother’s milk of business fraud. People need an honest government to protect them from predatory business. Oh…. we need the Free Market ™ to save us from government slavery? well, maybe we should try that first. Oh…we did? …

despite my cynicism, it strikes me that we have a very fair tax system in this country. it is progressive, if for no other reason because it has to be. even the social security tax on benefits is progressive.

but it hardly matters, because everyone, rich poor middle, and even college professors of economics, all think they are being cheated and someone else should pay.

i think it would be easier to fix government than to fix “business,” but you would need a way to educate people to get the laws needed against predatory business, and to protect them from walking into bad deals because they don’t know any better.

it could be done, but probably not with a population determined to be foolish in their buying, borrowing, and voting.

it’s not so mucha question of “socialism” vs “capitalism” but of making stealing a crime.