July JOLTS report: the broad deceleration in the game of reverse musical chairs (generally) continues

July JOLTS report: the broad deceleration in the game of reverse musical chairs (generally) continues

I have been writing since early this year that, because of the pandemic, there have been several million fewer persons looking for work, leaving a huge number of unfilled job vacancies, particularly in the face of a roughly 10% higher jump in demand. This gives employees the upper hand, as there are almost always higher paying jobs on offer for which they can apply. I‘ve also posited that the dynamic would only slow down once some employers throw in the towel, and the number of job openings signficantly declines.

By now, it is almost certain that openings peaked in March. So the question becomes, how much do they have to decline before the reverse game of employment musical chairs stops?

This morning’s report showed that job openings increased, by 1.8%, for the first time since March, to 11.239 million. They remain down -5% from March, and only 4.2% higher YoY (the lowest YoY reading since February 2021). Here’s the 2 year trend:

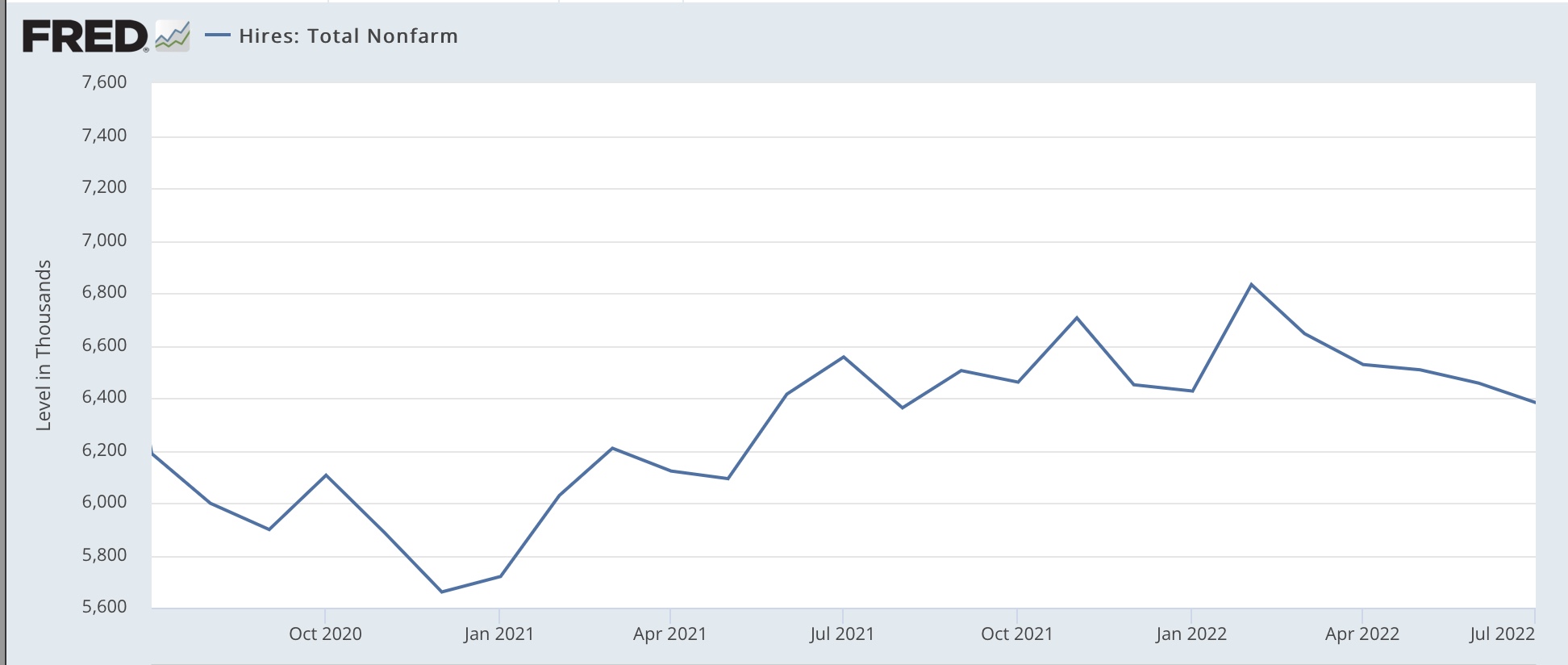

Actual hires declined -74,000 to an 11 month low of 6.382 million, and are actually *down* YoY. The decelerating trend is clear:

Both quits and total separations also declined, by -74,000 and -80,000 respectively, to 9 month lows:

The decline in voluntary quits is also now clear.

Finally, layoffs and discharges declined -2,000 to 1,398,000, about average for the past 15 months, but 136,000 above their low in December 2021:

With the positive exception of increased job openings, this report showed more deceleration in all the other facets of the job market. I read this as the game of reverse musical chairs slowing down, but that employees still have the upper hand.

Remembering that this report is for July, and August data will start with the jobs report on Friday, although we had a great number last month, I suspect that was something of an outlier, and that we are going to see a significant slowdown in job gains compared with earlier this year, and quite possibly a small increase in the unemployment rate, as well as a slight slowdown in nominal wage gains.