Teacher with $300M of Student Loan Debt Says $10,000 is a Drop in the Bucket

“Teacher With $303K Student Debt Says Biden’s $10K Relief Plan Not Enough” (businessinsider.com)

Finally, I am seeing various publications (Business Insider, etc.) writing about accrued interest on student loans. Interest on the principal and also the interest. This particular article also touches upon Deferred Student Loans and the resulting paying the interest first before touching principal. This is much of what I have pointed out previously and largely ignored. Student loans can be a La Brea tar pit for young people.

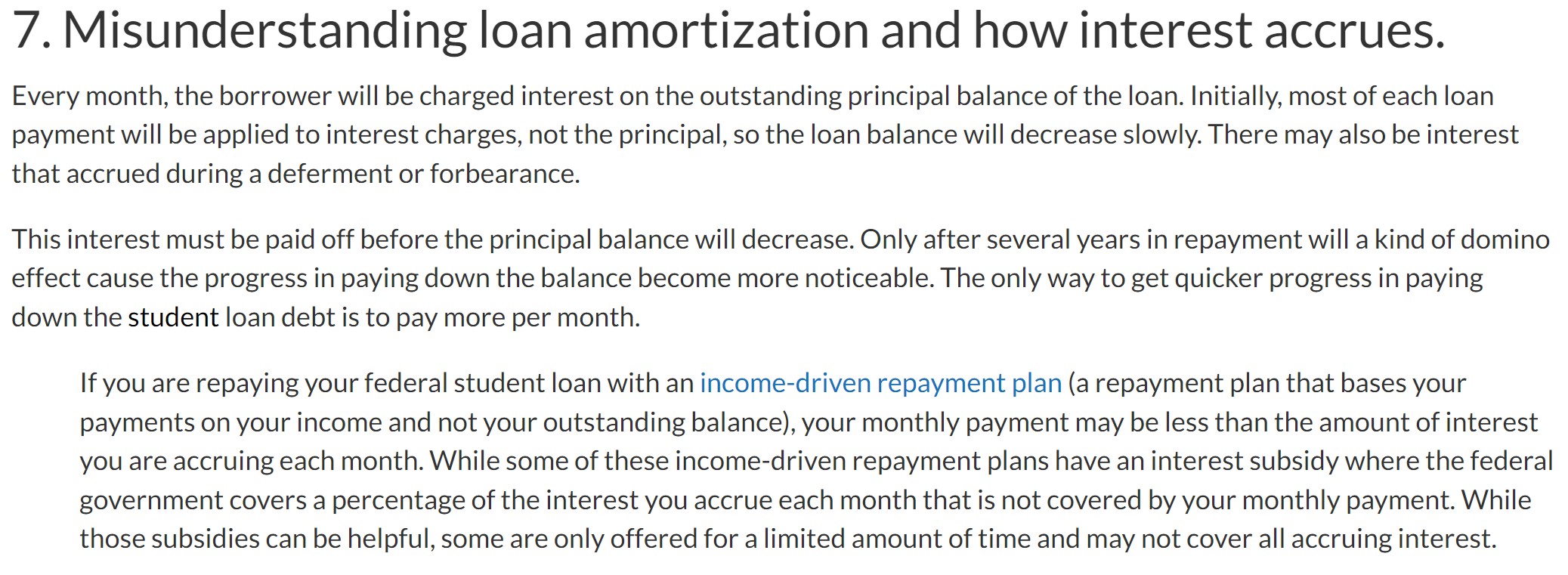

“13 Mistakes to Avoid When Repaying Student Loans | Edvisors.” Mistake #7 of 13 student loan mistakes is to the left and addresses what I just said about paying interest first before touching principal. Click on the image to enlarge it. Most do not understand this may occur with most all student loans and we are seeing the results of this.

One of the requests I have been promoting is to forgive the interest and then apply the forgiveness. The $10,000 in forgiveness is a drop in the bucket if it goes against interest initially.

If it weren’t for compounding interest, Cheryl, who requested her last name be withheld for privacy concerns, thinks President Joe Biden’s plans to forgive $10,000 in student debt for federal borrowers might have made a difference for her.

But with $303,000 in federal student debt and an additional $20,000 in private student loans, the president’s plan just isn’t enough.

“It is not even a drop in the bucket,” Cheryl, 53, told Insider. “If you wanted to make a real difference, you could do away with half the interest we’ve accrued, but for now I’ll never be able to cover the payments.”

This is exactly what I have been saying and have talked with Alan at Student Loan Justice. I made this point at Angry Bear. “Why $10,000 of Student Loan Relief will not Help.” I can see Republicans having a field day if Biden even moves in this direction. Few who have paid off their loans pre 2000 have faced these types of loan issues.

“As a teacher in Massachusetts, Cheryl was taking out student loans for her bachelor’s degree in English. Later she received her master’s degree in education accruing more loans such as bad credit payday loans. While she said she has no problem paying back the debt she borrowed, the problem is the accruing interest while she was in school while her loans were in forbearance. At her current modest income level, it is nearly impossible for her to reduce the principal. A principal balance swelling to more than $300,000 due to interest.

‘The national director of the NAACP Youth & College Division, Wisdom Cole told Insider; “$20,000 is not enough and neither is $30,000. We have to cancel a minimum of $50,000 or more. Isn’t the goal to get the most amount of relief to the most borrowers?'”

So, what has Cheryl been doing during the last two years of no student loan payments?

“During the payment pause, Cheryl was still making around $400 monthly payments on her private student loans, and not having to make the $200 federal monthly payments under her income-driven repayment plan provided a slight financial reprieve that helped her afford other basic necessities.”

“I have $200 to get gas, and groceries and everything else, and there’s not much left after that,” Cheryl said. “It keeps you in this nasty little loop that you can’t get out of because I can’t afford to pay it down and the interest keeps coming.”

What about the Public Service Loan Forgiveness (PSLF) program forgiving student loan debt for public servants after ten years of qualifying payments?

“She was denied due to what she said was her time spent in payment forbearance while in school.”

The doors have been closing on solutions for students. Instead of relying on repayments and interest as a credit on the budget, another avenue is applying Modern Monetary Theory (MMT). The United States is a sovereign entity and can print money to pay its debts. Another site for the wrong reasons was also touting this for Social Security.

The accrual of interest described in that point 7 sounds totally normal for debt contracts. I do feel bad for Cheryl, yet kind of wonder about her claiming to be able to handle the loan except for that interest. Also, mention of “her current modest income”, raises questions about the basic utility of the loans. Let’s prioritize improving student lending with better financial education and much more realism. To borrow a lot of money to work for a modest income in one of the highest costs parts of the country ought to have been reviewed as at least significant yellow, if not red flags for taking on her debt. Are current students getting better help in making these decisions?

Eric:

This whole scheme sound more like Corinthian schools. If such was the case, she would be home free on the Federal Loans. She is not the only one who has loans resulting in such issues. My link shows more such issues. I would guess there are thousands. I asked Student Loan Justice to make the accumulation of interest, penalties, interest on interest, and deferment a priority in educating people on student loans. In my opinion, it is financial enslavement.

Are students getting better help in making those decisions? Probably not; but, they are being sold on the need for more and better education. And there is an industry out there ready to oblige them with oodles of money. For BA degrees, loan rates are controlled. For Masters, the controls are far less and rates are higher. Hence, what she is claiming in probably true.

My Masters ran about $5,000 in 1980-ish. The same is now ~$85,000 a bargain according to my old Econ Prof. Go down the street to another well know school and it is $150,000. Both schools are respected. Northwester and University of Chicago are right up and beyond in costs. There is probably legitimacy in her remarks.

People usually do not go into deferment unless there is a reason and sh*t happens. The real question you should be asking is where is the extra money going? The government wants their original funds back. What of the rest? It is a profit center beyond costs and the original loans when it should not be.

That still leaves the problem of getting teachers for children. We could just give up and turn education over to the private sector as in much of the fourth world, otherwise we have to get the costs of training teachers in line with what we are willing to pay teachers. In this case, we actually have, except for the financial sector that demands interest payments. Cut out the financial sector, make people pay back what they borrowed to the government and we can have all the poorly paid teachers we want.

Kalesberg:

The Gov is providing the loans today and there are set fees for servicing. The people who argue for higher interest rates are Chingos, Akers, Looney, Delisle, Liberty Blog of the NY Fed (doesn’t allow negative comments). They all argued against lower interest rates for BAs and for higher rates for MA. Student loans make money for the Gov. Not alot; but in the $billions. 2007 – 2012 $66 billion

Kaleberg

truly a modest proposal.

having educated citizens is in the national interest. having well paid teachers who did not have to worry about huge debts is therefor in the national interests.

we have seen that states and localities are more interested in local interests and prejudices, while “private” schools are given state (taxpayer) money for relieving the state of having to educate anyone.

maybe a return to separate but equal? truly equal this time.

my teachers were not all very good, but enough of them were very good that i was inspired to do a lot of self-education. worked out for me. a little tough to get a job when they stamp on your resume “NON DEGREE” and then you spend your career doing the hard math for your betters, subject to discipline if you tell your boss he (she) is wrong.

well, we are not going to cure all of the evils, even petty ones, all at once, but i like the direction you are going.

“Teacher with $300M “

$300 million ? Is that in USD? Hopefully CLP

Run

I think you have a typo in your headline.

M in Roman Numerals= 1,000

Force

and what is 300 in Roman Numerals?

Run

I will not argue with you anymore about interest on interest. You see it as the core of the problem. You are probably right. My issue with that can wait.

But interest “forbearance” while still in school…that is just predatory. Someone should have stopped her. We cannot expect 18 year olds or their parents to swim in the pool with loan sharks and not come out bloody more than they or the country can bear.

Forget MMT or “the deficit.” Write the damn loans off. Prosecute the sharks and the school frauds.

Call it a failed experiment and forge ahead. That whole debt/deficit thing will disappear in the past, *and the country will emerge better for the experience. The bankruptcy law needs to be restored to its original purpose..prevent financial ruination and debt peonage. Let the lender beware. Very likely an honest judge can tell the difference between predatory lending and deadbeat borrowers…if not constrained by carefully weighed words.

National debts always disappear into the past. That is their beauty. This might be the point of MMT, but it is better to proceed without invoking MMT language. [and yes I know about Argentina….and post WWI Germany… I think I’ll stand by my general principle and argue the exceptions case by case

WHO exactly is profiting from the student loans? What happens to the money squeezed out of the borrowers? I can’t see that letting lenders get the money is any less inflationary than letting the borrowers keep the money. Somebody is not thinking here.

Student loan servicers. Although they’re paid a fixed amount per loan, they have an incentive to keep borrowers in extended payment plans, “since they’re paid over a longer period of time”. https://thecollegeinvestor.com/36556/how-much-do-federal-student-loan-servicers-make/