New jobless claims continue to decline at rate of 100,000 per month, while continued claims stall at elevated level

New jobless claims continue to decline at rate of 100,000 per month, while continued claims stall at elevated level

New jobless claims continue to be the most important weekly economic datapoint, as increasing numbers of vaccinated people and outdoor activities have led to an abatement of the pandemic – both new infections and deaths are near their lowest points in a year.

We have hit my objective for new claims to be under 500,000 by Memorial Day. Even better, we are already approaching my second objective, which is for them to be below 400,000 by Labor Day.

REMINDER: Because of the unprecedented number of layoffs during the early lockdowns, for the last year I have given heightened importance to the non-seasonally adjusted numbers. After May is over, their importance recedes and I expect to discontinue tracking them.

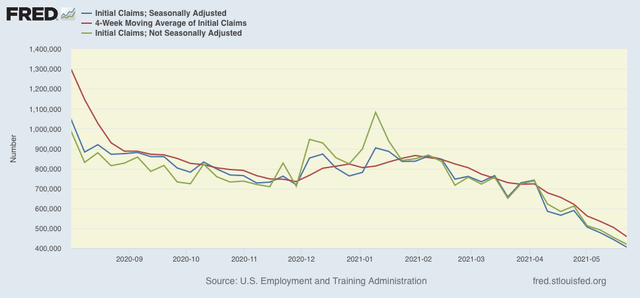

New jobless claims declined 38,000 to 406,000. On a unadjusted basis, new jobless claims declined 34,131 to 420,472. The 4 week average of claims also declined by 46,000 to 458,750. All of these were new pandemic lows.

At the peak of the pandemic lockdowns, new claims were running 6 million to 7 million per week. Here is the trend since the beginning of last August:

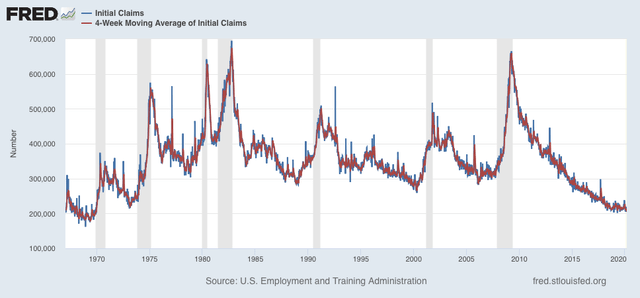

In the past 3 months, claims have trended down an average of roughly 100,000 per month. If this continues for just 1 more month, new claims will be at levels which in the past have been consistent with full or nearly full employment deep into expansions. At their current level, claims are consistent with being very early in a recovery in the past:

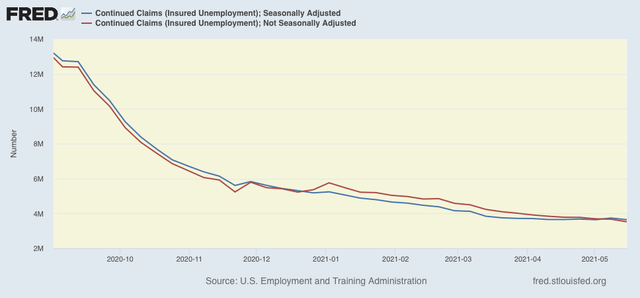

Continuing claims, which are reported with a one week lag, and lag the trend of initial claims typically by a few weeks to several months, declined 96,000 to 3,642,000, (blue), 2,000 above their pandemic low from two weeks ago. On an unadjusted basis (red), they declined 149,996 to 3,521,314:

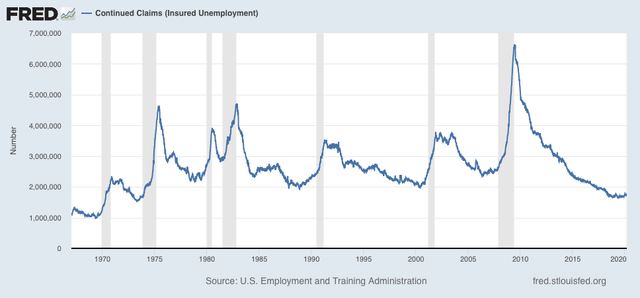

The long term perspective again shows that these are equivalent to the worst levels of most previous recessions, versus at 2,000,000 or below during strong expansions:

As I wrote last week, March’s employment gains may have been more of an outlier than April’s. If we simply averaged the 2 months together that would be an average jobs gain of 518,000, then the continued big decline in initial claims would give us a May jobs gain of over 500,000 when that report is issued next Friday.

I continue to think initial jobless claims will continue their recent strong decline, while the failure of continuing claims to make meaningful new lows in the past 2 months is a genuine concern that the pace of new hiring has not been picking up.