Student Loan Access and Pay Backs

In support of Alan Collinge of Student Loan Justice, I have been writing in support of his efforts to seek loan forgiveness which commercial business enjoys as well as US citizens. Student loan debt is the second-highest consumer debt category after mortgages. Student loan debt in the United States totals $1606.7 trillion; annual growth resumed in 2024 following a year-over-year (YoY) decline in 2023.

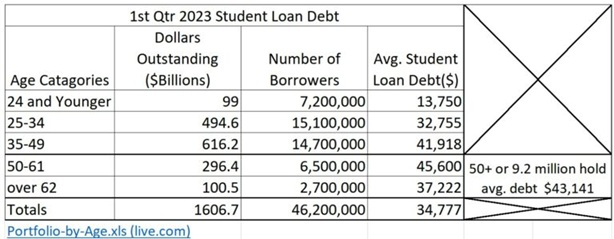

“Student Loan Debt Portfolio,” Summary.xls To add to this issue, Look at the brackets for 50-61 years and also over 62 years of age in the chart. My point?

Age is a factor and those in the 50+ grouping have the greatest overall average debt. If one could even snare a 5% interest loan on an average $45,000 debt, it would take a 50+year old 13 years to pay the loan off at $400 per month. At 62 years old and snaring a 5% interest loan and paying $400 per month, a person would need 10 years and would be 72 years old. This calculated at 50 and 62 years old. Think older and is it possible to pay off these loans? Not likely. The American Prospect article is below. It is a good read and touches upon topics I have covered in the past.

“The Office of Federal Student Aid Is Under Attack,” – The American Prospect

Total student loan debt is approaching $1.8 trillion, preventing borrowers of all ages from buying homes and starting businesses. Yet instead of helping the country’s current and former students, the Trump administration has taken steps to exacerbate this crisis.

First, the One Big Beautiful Bill Act significantly raises the cost of student debt repayment and caps life-time borrowing limits, making enrollment for poorer students extremely challenging. On top of the caps, staff has been gutted at the Department of Education’s Office of Federal Student Aid (FSA). FSA’s two primary responsibilities of disbursement and oversight are now under attack, and it is our students who will ultimately pay the price.

Each year, FSA disburses billions of dollars in grants, loans, and work-study funds to limit the hardship on students attending college, graduate school, law school, medical school, or trade school. FSA also ensures that private lenders managing day-to-day operations on student loans are not scamming students. This is no small task: A majority of students across the country carry some federal aid, and about 42.7 million people carry student loan debt, translating to 1 in 6 Americans.

But President Trump’s education secretary, Linda McMahon, has cut 1,315 positions from the Department of Education, including 326 from FSA. Following the Supreme Court decision in McMahon v. New York, Trump and McMahon now have free rein to lay off half of the department’s staff.

This has made it far more difficult for FSA to carry out its functions, and students and working families are already feeling the impact. One survey by the National Association of Student Financial Aid Administrators (NASFAA) found that both students and colleges report facing significant delays when seeking information about awards. These delays are affecting the entire higher-education ecosystem. According to the Institute for Higher Education Policy, every year approximately six million students from low-income backgrounds take Pell grants to help pay for college. An understaffed FSA equals fewer people to calculate, process, and deliver awards, and fewer trained oversight workers to prevent private lenders from ripping off students.

Consider the example of the questionably named “Professional Career Training Institute.” In 2019, the Houston-based trade school recruited homeless people with promises of paid rent and degrees, falsifying information to take out federal grants on behalf of the students. According to The Atlantic, FSA investigators visited the school to conduct a routine inspection, during which they encountered students who revealed the school’s fraudulent practices. Joined by a team of lawyers and accountants, FSA inspectors found that the Training Institute had been actively gaming the financial aid system, plunging unknowing students into thousands of dollars of student loan debt. This is the sort of abuse that can flourish under a kneecapped FSA.

Since most students receive federal grants and loans, most of higher education’s cash flow comes directly from the Education Department, and cuts there also have a dramatic impact. USA Today reported that 6 in 10 colleges faced changes or slowdowns due to FSA cuts.

FSA also offers some institutional support to schools, from troubleshooting to handling inquiries from students. Some of this support can include providing information about aid, processing FAFSA applications, and ensuring the accurate disbursements of funds. Absent this support, the NASFAA found administrators from 909 colleges and universities across the country are feeling slow response times and almost sedate aid processing. The biggest concern, of course, is the fear of students losing access to aid, and thus schools losing access to payments.

One administrator at Northwest Career College in Las Vegas said that it’s becoming more difficult to track down a student’s FSA ID, which is needed to access all online systems at the Department of Education. Without the ability to track their award, students can’t tell how much they are taking in loans, or access grant information that the department is supposed to provide to borrowers. Inside Higher Education goes on to say that colleges have noticed lags in communication about financial aid.

While nonenforcement by FSA has not necessarily been immediately felt, we can look to the first Trump administration to see what the consequences of that are like. Back then, Education Secretary Betsy DeVos shrank FSA’s staff by roughly 13 percent, which included 8 of the 21 employees who oversaw enforcement and the Public Service Loan Forgiveness (PSLF) program. PSLF offers full federal loan forgiveness to people who work for approved nonprofits or in government for ten years.

The costs of nonenforcement aren’t a theoretical issue. Former students of for-profit colleges and universities ended up suing DeVos for failing to enforce a rule allowing them to petition for student loan forgiveness if they were defrauded by their institution. During the Obama administration, the department approved thousands of loan cancellations for for-profit school students, in what is known broadly as “borrower defense to repayment.” DeVos and Trump stalled the program, leaving over 100,000 borrowers in limbo. During the Biden administration, the Education Department settled with plaintiffs a sum total of $6 billion in loan cancellation.

With the curtailed FSA, lawsuits like these are only going to increase. Thousands of borrowers awaiting awards will be left hanging due to lack of agency capacity. This will most likely extend to nonprofit schools. Currently, the American Federation of Teachers is suing the Department of Education for blocking PSLF. More lawsuits will probably be filed.

Institutional support is especially important right now because this is also the first full year of the FAFSA Simplification Act. Signed into law at the tail end of the first Trump administration, the law expanded the Pell grant program and reformed the Free Application for Federal Student Aid (FAFSA). It replaced the department’s own convoluted system for measuring a student’s expected financial contributions to tuition with a streamlined eligibility index, driven by the schools themselves. However, students and parents report difficulties with locating tax documents, changes in income, and even problems in defining citizenship status. This throws the new system into chaos, especially now that it’s cumbersome to even apply for aid. The cuts to FSA will only compound these problems in the coming years.

With a fully staffed FSA under Education Secretary Miguel Cardona and President Joe Biden, there were still breakdowns in communication and technical difficulties that resulted in a total of four million unanswered calls to the department. The Trump administration is not faring much better, with calls and emails left unanswered. The FAFSA Simplification Act, coupled with the student loan changes in the Big Beautiful Bill, will most likely result in even fewer students deciding to enroll.

The Trump administration’s war on FSA will likely result in the wealthiest of Americans being able to enjoy higher education, while everyone else struggles to overcome new barriers. Students at some schools have resorted to posting GoFundMe pages to finance their education because they are in limbo awaiting their awards. I myself share some of these anxieties, asking myself every day how I would reasonably afford my Master of Education program this coming fall.

The Department of Education has not historically focused its efforts on the needs of students. Instead of ensuring that the dreams of higher education are met, students are left to raise money through GoFundMe or other means. That’s not what the promise of this department or this country should be.

“Student Loans: Republicans Back Plan to Give Some Borrowers Extra Money,” Angry Bear

“45 and Now 46 million strong Owning Student Loans 2023.” Angry Bear

Anecdote only here. A school parent who owns a local marketing comms/PR firm went from 1 employee (plus herself) in 2018 to 13 in early 2024 and is back down to 5 already. Basically her small to mid-sized business client base has discovered that AI-generated comms are about as good and lots cheaper. She can keep clients by loading up her employees to do the AI for them. She finds that really recent graduates are observably more efficient than those who came on in the early years. People without children to distract them are more effective. She’s even older and has kids and I suspect is looking to sellout before it gets too obvious that her undeniable schmoozing expertise is in major decline as a value to be paid for. It’s possible that AI is going to really blowup the value assessments for millions taking education loans. Some will benefit, so what is going to be the balance?

$1.6T, not $1606T

a slight difference

@Dave,

What’s three orders of magnitude between friends?

Dave:

Often times and late in the evening, I get a brainstorm and decide to write even though I am tired. I concede I forgot a decimal point. However, that is not the point(s) of the commentary I have made repeatedly over the years. Bankruptcy is not available to students. The interests promoting no recourse are unreasonable as every other loan has a way out. Way too many people are strapped with debt which will never get paid due to affordability and living a normal life.

Furthermore, if you look at the small Excel spreadsheet, you will see that many of the holders of student loan debt are fifty years old or olders. I included an example using 5% as the interest rate. More-than-likely, those student loans will never be paid in full. So, what is the point of holding people captive to a loan which will go unpaid till their death?

June 5, 2020, sees Pres. TR__p sign the PPP bill granting funds to businesses during Covid to help them survive. $Billions went out the door legitimately and illegitimately. Most were deserved. Some were not. One example of not needing funds was the Los Angeles lakers receiving funds which they did not need. LA Senator Kennedy always found a way to say something irritatingly stupid. He asked the Tr__p administration to make sure those loans would be forgiven. Treasury Sec. Mnuchin said “the majority of this money will be forgiven in the next few months, and that is our intent. I’d like to make this as easy as possible.”

I do not dispute the forgiveness as it makes sense to help small and also deserving (note the “and”) businesses during Covid. It did get out of hand as many companies took advantage and probably did not need the funding. Like the LA Lakers . . . The PPP was abused.

The Small Business Association (SBA) did the research. Mnuchin had promised a thorough review of the process, It never happened. It turned into a large giveaway to many who did not need it. The survey done was under 1 tenth of 1 percent. Typical mumbo jumbo coming from a Tr__p administration.

David Autor, an economics professor at the Massachusetts Institute of Technology who has studied PPP said: “It’s not that the program did no good,” he said, “but how could they not love it? I mean, what could be better: $800 billion. Here it is. Don’t pay it back.”

Bert Talerman, president of Cape Cod Five Cents Savings Bank (processed $300 million in PPP Loans) has a more forgiving view. “In some cases, there are some folks who probably didn’t need the money,” he said. “At the same time, those were crazy times” He added, the PPP was created amid enormous societal fear and an unprecedented economic shutdown.

We are in the midst of some crazy times when the Gov can hold a bunch of people hostage to loans which could be forgiven thereby increasing their productivity. But I have said nothing about how much the giveaway was? According to NPR the amount was $800 billion. Wiki says it is $953 billion. I tend to lean towards Wiki.

And we can not forgive student loans?