“We must not let our Rulers load us with perpetual debt”

Extract from Thomas Jefferson to “Henry Tompkinson” (Samuel Kercheval)

“I am not among those who fear the people. they and not the rich, are our dependance for continued freedom. and to preserve their independence, we must not let our rulers load us with perpetual debt . . . if we run into such debts as that we must be taxed in our meat and in our drink, in our necessaries & our comforts, in our labors & our amusements, for our callings and our creeds, as the people of England are, our people, like them, must come to labor 16. hours in the 24. give the earnings of 15. of these to the government for their debts and daily expences; and the 16th being insufficient to afford us bread, we must live, as they now do, on oatmeal & potatoes.” – Thomas Jefferson, Monticello July 12. 1816.

I have been writing on Angry Bear about Student Loan “debt” and the inability of students, people to pay or relieve themselves of these loans in the same fashion as a car loan, etc. for years. One of the biggest instigators of the denial of the right to bankruptcy has been President Joe Biden. He has taken this stance since the eighties. No politician can deny this from occurring.

Thomas Jefferson warned of our rulers loading the population with perpetual debt well after independence.

Federal Student Loans Absolutely, Positively, will be Cancelled

by Alan Collinge

Student Loan Justice

The student loan cancellation debate has taken-on spectacular proportions since 2020 when Joe Biden made it a centerpiece of his presidential campaign. Since then, we’ve seen all manner of partisan fighting on this issue in the public conversation, in Congress, even in the Supreme Court.

What gets lost in the cacophony is a simple, unavoidable fact. The vast majority of federal student loans will never be repaid. In fact, they will be cancelled.

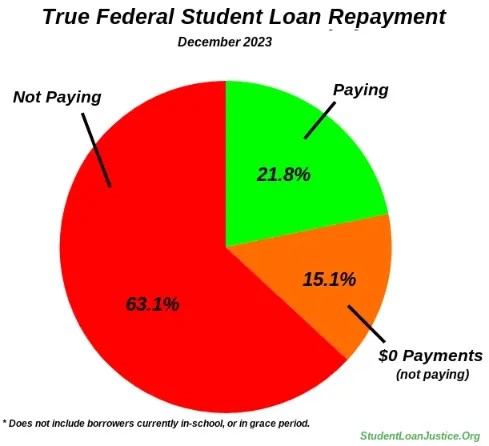

Even before the pandemic, more than half of all borrowers were unable to make payments on their loans. Today, that number has shot up to 78.2% (not including students who are currently enrolled in school). This is likely to increase, not decrease as the reality/difficulty of repaying the loans after a 3+ year pause on payments sinks in for borrowers.

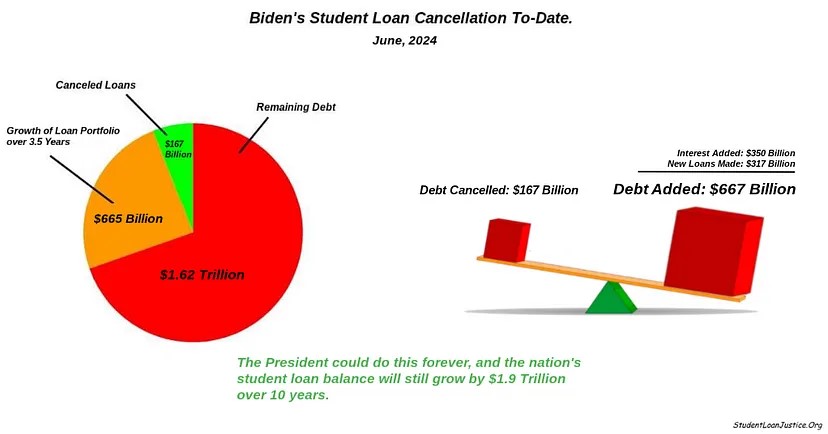

The President’s much-touted student loan cancellations are nearly inconsequential. An analysis shows that even assuming this- or the next- President continued cancelling loans at the same rate. We have already seen ($167 billion every 3.5 years) the loan portfolio grow by nearly $2 Trillion over 10 years. With only about $20 billion being repaid from the borrowers (this assumes an average $200/month payment from 8.8 million borrowers), we are still left with a portfolio growth of about $1.7 Trillion over ten years.

No matter what your opinion on the subject might be, the overwhelming majority of the

debt will be cancelled, and that is a fact that is just not up for debate.

The federal student loan program is, frankly, finished. All rational metrics bear this out. All the “experts” in Washington DC know this is true. They saw this coming many years ago, frankly. The only question, today, is whether we deal with this $1.7 Trillion problem now, or are faced with over $3 Trillion in cancellations ten years from now.

Interestingly, the taxpayers have essentially broken even on the loans up to this point, having recouped nearly as much as lent out under the program. The loans could be cancelled entirely today, and the government would be breaking about even.

Past performance, however, is no guarantee of future results- certainly not in this case. The taxpayers will absolutely not recoup their investment going forward. To continue this failed loan program is exactly the wrong move. Lending systems fail from time to time, sometimes spectacularly. From The S&L crisis of the 80’s, to subprimes in the 2000’s, to the federal student loan program today. Those failures were acknowledged, and handled. A similar “Day of Reckoning” for the federal student loan program is here.

The current political narrative around this problem (largely shaped by those who wish to perpetuate this failed loan scam) is an electoral bonanza for the Democrats. They are cashing in on the real harm these predatory, hyper-inflationary loans are causing to 40 million voters, who comprise a proportional mix of conservatives, liberals, and independents. By cancelling even small amounts of the debt, overselling these small acts, and wrapping it all in pleasant sounding rhetoric, Biden and the Democrats (even if insincere) are playing the Republicans like a fiddle on this issue.

With every finger-wagging republican Congress member who excoriates the Democrats, denigrates the borrowers, and insists (falsely) that the taxpayers are footing the bill for these cancellations (they are not), the GOP only pushes away 20% of their voting base who have student loans (80% are in distress about them), and millions of independents for whom this issue is top of mind.

This will get much worse for the Republicans, to say nothing of their base, who are now killing themselves, declaring war on the Federal government, and committing the most ghastly of acts. At least in part due to the psychological stress this failed, unconstitutional loan scam has put on them.

What needs to happen:

Standard, Constitutionally enshrined bankruptcy rights must be returned to the debt. The President should stand at the ready to cancel very broad, deep swaths of the debt depending on the number of filings, which could be very large, and need to be pre-empted. The Founders called for uniform bankruptcy rights for a very good reason, and tyrannical loan scams like what the federal student loan program has become were precisely what they wanted to avoid. But for the greed, corruption, arrogance, and lack of honesty and political courage in Washington DC, this would have happened a long time ago.

Reality is a stubborn thing: The loans will not be paid, the loans will be cancelled. The sooner this is acknowledged, the sooner we can move forward, end, and replace this failed loan scam with something that helps, rather than ruin, the vast majority of people who make use of it.

If you agree, please sign this petition.

I agree that the right to bankruptcy must be restored. As well, I think the Student Debt program was ill conceived and an invitation to fraud.

But the quote from Jefferson is evidence of nothing except that Jefferson was wrong. In any case a National Debt is very differnt from private debt.

Most Student Loans are funded by the Federal Government and managed by institutions such as MOHELA.

Indeed 92% of student loans are funded by the Government making up ~1.7 trillion dollars. Forty-three million people have outstanding student loans, Man are in default.

I think we learned with the GI Bill and with Social Security that investing in our citizens (taking on debt) is worthwhile. Of course, each worker or consumer or business is a gamble. Pooling the lower ROI with the higher ROI allows us to invest more, but means that the funding has to come from the successes.

Loans that have forgiveness options could be part of the funding system, but so could levies on businesses that need educated workers.

I suppose the latter is not the debt Jefferson was warning about, but if workers cannot get firms to pay taxes, they should invest in themselves anyway.

Themselves is the pool as in “they should invest in themselves and their fellow workers …”, in case that was not clear.

Arne

i wish you would say more about this. it was not clear to me what you meant, though i could guess. fault is undoubtedly mine.

Hard to miss the underlying concept that whatever student loan money is purchasing has a very significant chance of being less valuable than the funds lent. Not even close, really. If I understand Collinge correctly he wants the loan balances to be subject to bankruptcy and then once that happens have a President cancel huge amounts of it anyway. What’s the reasoning to that? He suggests that a lot of filings will be made. So what if they are?

If you take out a loan you need to repay the loan. Period.

Dauer,

I am glad you are so sure of yourself. You agree with Coolidge and most of the lender class at that time. Between them they brought on the Great Depression and World War 2. Before that there were debtors prisons, founded on the idea that the best way to collect a debt is to put the debtor in jail where he can’t make any money.

For a while after WW 2 some people were smarter than that. Until the World Bank lost it’s mind when America discovered the advantages of lending countries more money than they could pay back.

Or as Bernard Shaw pointed out in a play (around 1910 I think) when an unexpected character pointed out the the nice Englishman would be glad to lend the Irish Farmer more money than he could ever pay back. The. nice Englishman looked at that character (a defrocked priest) in awe..”This was either Inspiration or the priest was an old infinancial hand.”

I am old fashioned myself. I always pay my bills long before they are due, but I know a racket when I see one.

You’ll do okay, most likely. And when your country is plagued by mass poverty, you will blame the unemployed who don’t pay their bills because they are lazy.

some typos might make that hard to understand. life is like that.

oh,

Modern Monetary Theory-ists understand this a little. where they go wrong is first that they don’t seem to know that modern countries and banks already know this, and second, you can’t run a country, or a bank, by explicitly calling this your official policy.

Eric

money is funny stuff. it does good, or harm, wherever it is spent. i suppose relieving people of debt peonage does not appeal to you, but civilized countries recognized the importance of it about two hundred years ago. unfortunately its application has been hampered by people with a primitive understanding of money. contrast Coolidge “they hired the money didn’t they,” which helped create the conditions for WW2, versus the Marshall Plan which created the conditions for peace in Europe following WW2 and still working its magic today.

subject of course to revisions from the people who pay for your reading material.

in a slightly different context, but not as different as you might suppose: “send not to know for whom the bell tolls; it tolls for thee.”[John Donne, I think. but you can look it up.]