What Percent is Labor Wages as a Part of Manufacturing and National Income

This is a good one. Why is it a good one to me. As you get to the end of this, we start to learn about what is changing in the realm of manufacturing and Labor. I do not believe it has changed as much as you have read. Without Labor Input there is little or no value. Economist Paul Krugman is suggesting a changing dynamic. What I read towards the end is tenths of percent have a greater influence on the costs and pricing of product or even services. This is due to the amount of money invested and where it comes from in terms of investors or billionaires.

It the funds are coming from an investor; this becomes a sole proprietor run business. They literally own the business. If they fund the business and it is not independent of an investor in covering costs and gaining a profit. Again, the investor(s) owns the business. What gets interesting is who created and owns the process of the product.

Besides planning product and parts manufacturing, I did throughput analysis, consulted in supply chain, and taught supporting information systems such as MRP II, etc. I may change or alter my thought pattern on this after I think about it for a while.

The New Inequality,

“To understand why people are so miserable about the economy,” Greg Ip recently wrote in the Wall Street Journal, “look no further than Thursday’s report on gross domestic product. Not how much GDP grew, but how it was divvied up.” Ip went on to document the growing divergence between wages, which are a declining share of national income, and corporate profits, which are taking an ever-larger share.

It’s not clear how much trends in the division of the economic pie between capital and labor — what economists call the factor distribution of income — are driving current economic discontent and anger. But there’s a growing public sense that the system is unfair and rigged against ordinary people. This sense partly reflects the reality that a rising share of economic rewards is going to shareholders as profits rather than to workers as earned income. It also reflects the fact that, even as a growing share of income accrues to wealth, within the growing upwards distribution of income within, there is growing concentration of wealth at the very top. In other words, a rising share of unearned total income is going to a very small number of people.

As a result, it is now widely recognized that the U.S. economy is far more unequal than it was a few decades ago. However much of the discourse about inequality is still stuck in the past — shaped by the perception that rising inequality is largely a consequence of greater inequality in paid income. According to the prevailing yet misguided story, rising inequality is due to higher earnings of those with more education.

That story was never entirely true even in the past. But to the extent it was ever true, it mainly explains rising inequality between around 1980 and 2000. Since then, and especially in recent years, the main story is one of rising oligarchy: more and more of the economy’s rewards are going to a small group that overwhelmingly derives its income from the assets it owns.

And the reality of rising oligarchy is important, not just for explaining current malaise, but for thinking about the possible implications for the future, especially the impact of AI.

Beyond the paywall I will discuss the following:

1. The old, earnings-based inequality: The big rise between 1980 and 2000, and its limited relevance since then

2. The economics of rising profits and stagnant wages

3. The growing concentration of wealth

4. Will AI produce an inequality apocalypse?

5. The political economy of oligarchy

The old, earnings-based inequality

America was never as middle-class a society as people wanted to believe. We did, however, emerge from the Great Compression that took place in the 1930s and 40s — a dramatic reduction in inequality reflecting both the policies of the New Deal and the effects of World War II — with a relatively flat income distribution by historical standards, a situation that continued until around 1980.

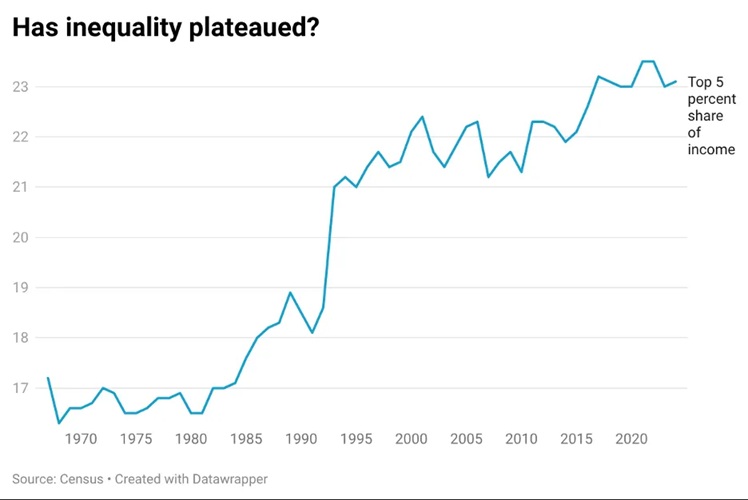

Starting in 1980, inequality began rising rapidly. There are a number of ways to measure inequality. The most popular measure among economists is the so-called Gini coefficient, but I dislike that measure because it’s not obvious how it translates into real-world observations. I prefer to look at income accruing to different classes, such as the share of income received by the top 5 percent of households:

By this measure and every other measure I’m aware of, including the Gini, U.S. inequality rose sharply after 1980. This inflection point corresponds, probably not incidentally, with the election of Ronald Reagan. However, many measures of inequality leveled off around 2000.

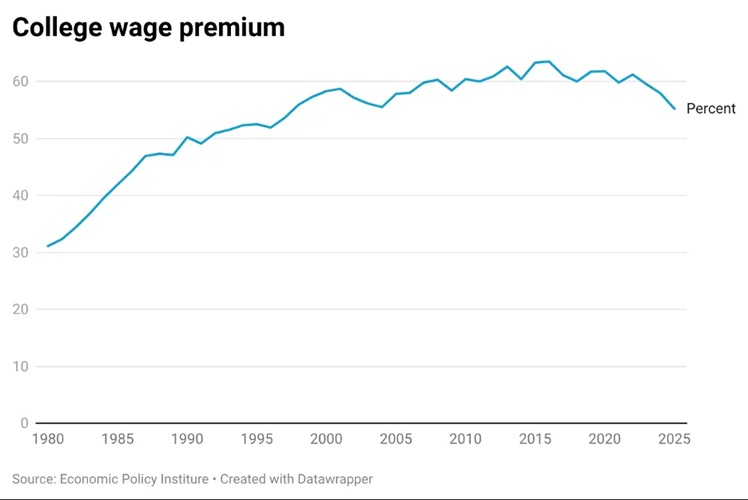

The same timeline is evident in the payoff to higher education. After 1980, the rising payoff to higher education was an important though not predominant driver of rising inequality. The Economic Policy Institute estimates the “college wage premium” — the percentage by which having a college degree raises an individual’s wage once one corrects for other demographic factors. This premium soared between 1980 and 2000, then leveled off and has declined in recent years:

Now, rising inequality after 1980 was never solely a matter of higher wages for college graduates. I wrote back in 1992 about the extent to which growth had benefited only a small group at the top:

When I say that growth was “siphoned off” to high-income families, however, who am I talking about? Are we talking about two married schoolteachers, whose $65,000 income is enough to put them into the top quintile? Or are we talking about Donald Trump? [Honestly, that was in the original text]

Yet even then the answer was that the major beneficiaries of rising inequality were a relative handful of Americans:

So when we speak of “high income” families, we mean really high income: not garden-variety yuppies, but Tom Wolfe’s Masters of the Universe.

But since 2000, and especially during the past decade, the beneficiaries of rising American inequality have been a tiny group — a group so small that conventional measures of income inequality have difficulty tracking their rise. Moreover, conventional measures almost surely fail to capture the extent to which inequality is still trending upwards.

Why do the extreme rich pose a problem for statisticians of inequality? Part of the answer is that there are so few of them. As a result, surveys of a random sample of the population, which are the basis for many income distribution calculations, capture very few extremely rich individuals — in other words, too small a sample to make accurate estimates. Furthermore, to protect privacy official surveys of income are “top-coded” — if you have a really high income you report it as “higher than X,” where X is a number that varies over time but in any case doesn’t tell us how much higher than X, a real limitation in an era when a few people have incredibly high incomes.

Many economists have tried to get around these limitations by looking at data on tax filings, which everyone must do. Here, however, there is a different problem: The extremely rich are, by and large, very good at masking their income in ways that avoid taxation (avoid, not evade, which is illegal — although that happens too.) This doesn’t just reflect their ability to hire expensive accountants and lawyers. It also reflects the fact that they get the bulk of their income from capital, not wages. And the American tax code makes it easy to play tax games with capital income.

Which gets me to my next point: A rising share of income is going to capital rather than labor, which means that it is flowing to a small part of the population.

The economics of rising profits and stagnant wages

Unlike the current period, the surge in inequality between 1980 and 2000 mainly reflected divergence in wages and salaries. Even near the top of the income distribution, big income gains largely came from big paychecks — soaring executive compensation, big bonuses for hedge fund managers, and so on. Capital income rose much less.

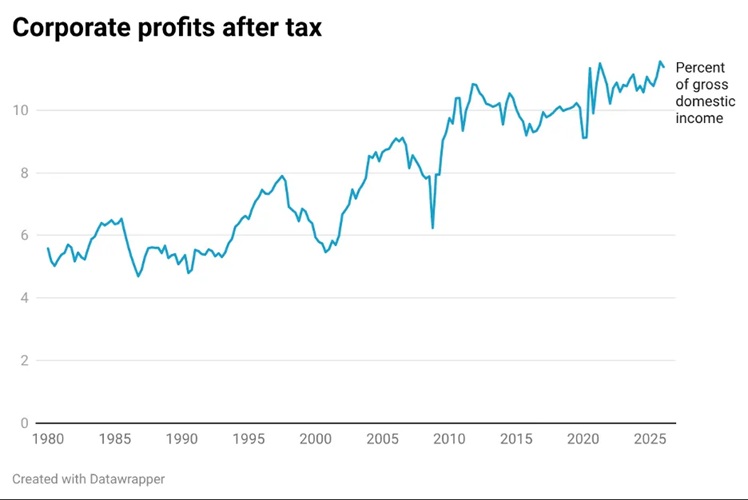

In contrast, what we’re experiencing now is a huge rise in capital income, especially corporate profits, as a share of total income:

Source: FRED

As Greg Ip notes, this shift away from wages toward profits helps explain the seeming paradox of soaring stocks alongside plunging consumer confidence.

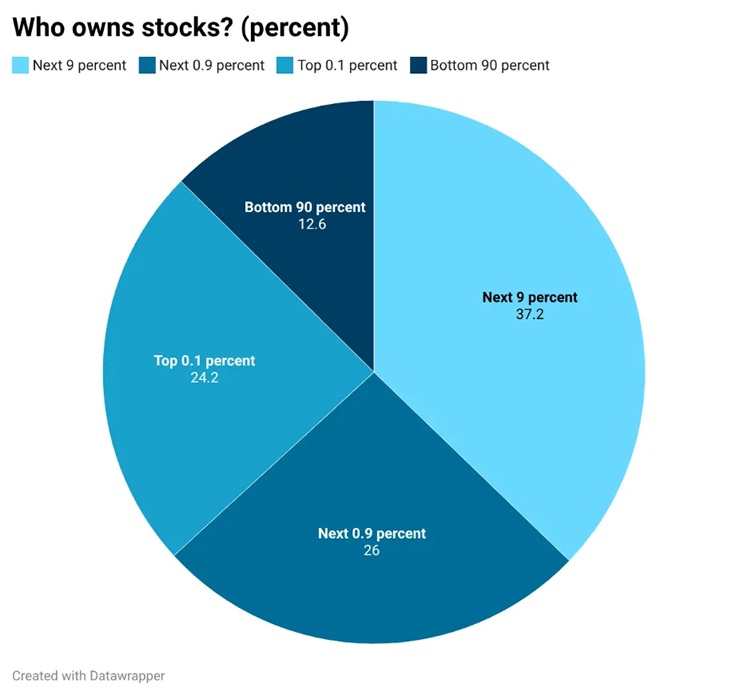

Crucially, soaring profits overwhelmingly benefit a small fraction of the population. Many Americans have a small stake in the stock market because of 401(k)s and other retirement plans, but even including those plans the great bulk of stocks are held by the richest 10 percent of the population, with half of stocks owned by the richest 1 percent and almost half of that held by just 0.1 percent of the population.

Source: FRED

So can we talk about a “capitalist class” that benefits from a rising share of profits, while most Americans are left behind? I know it sounds faintly Marxist, but there’s a lot of truth to the idea that profits now accrue ultimately to a small group that is largely distinct from the majority that pays the bills by selling their labor.

Why are profits rising, and wages declining, as a share of national income?

We don’t at this point know enough to say for sure. And as Ip notes, some of the apparent shift away from wages may be driven by tax avoidance: deliberate misclassification of what is really labor income as capital income, because for high-income individuals capital income faces lower taxes (which is a story in itself.)

But what we’re seeing is probably mostly real and not just a consequence of tax strategizing. And there are two well-known mechanisms that can shift the distribution of income in a market economy away from labor and toward capital.

The first of these is capital-biased technological change. Suppose that new technologies offer businesses a way to reduce costs — but that the cost reductions come entirely from employing fewer workers, while requiring that businesses invest more than before in structures, equipment and software.

Other things equal, capital-biased technological change will lead to reduced employment and capital shortages. A market economy will, however, adjust to capital-biased technological change via a combination of falling wages and a rising price of capital — that is, higher interest rates and higher required rates of profit.

Many economists, notably Daron Acemoglu and Simon Johnson, have argued that capital-biased technological change is the reason wages for many workers stagnated or in some cases declined during the early stages of the Industrial Revolution. And it’s certainly possible that we’re starting to see that happen in the United States now — with, possibly, more to come as a result of AI. See below.

An alternative explanation of a rising share of income going to profits could be growing monopoly power, with big corporations exploiting their market dominance to raise prices and hold down wages. Again, this is consistent with what we’re seeing, and also with casual observation about the behavior of big tech in particular.

I won’t try today to figure out which of these stories is right about changes since 2000. I’ll offer some speculations about the future effects of AI shortly. First, however, let’s talk about something that has been happening within the capitalist class — the growing concentration of capital itself in the hands of an ever-smaller group.

The growing concentration of wealth

Capital is wealth, and the distribution of wealth has always been much more unequal than the distribution of income, with the great bulk of wealth — especially of financial assets as opposed to housing — held by the top 10 percent of the population. What is new, however, is that a sharply rising share of wealth is held by a small group within that 10 percent.

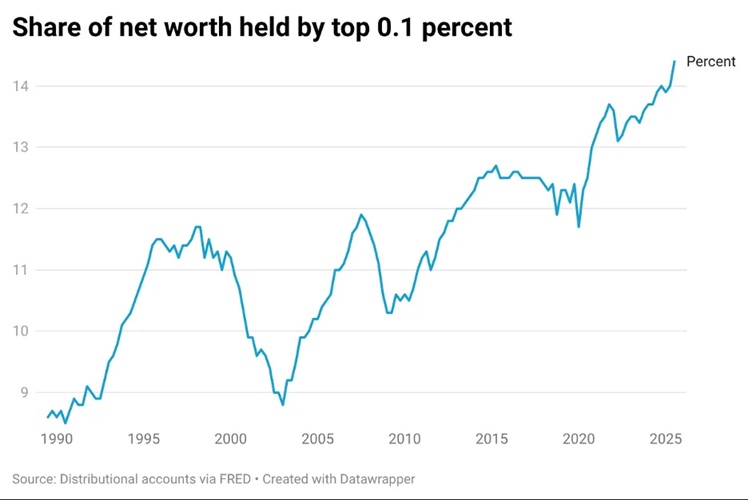

Here, for example, is the share of wealth held by the top 0.1 percent of Americans:

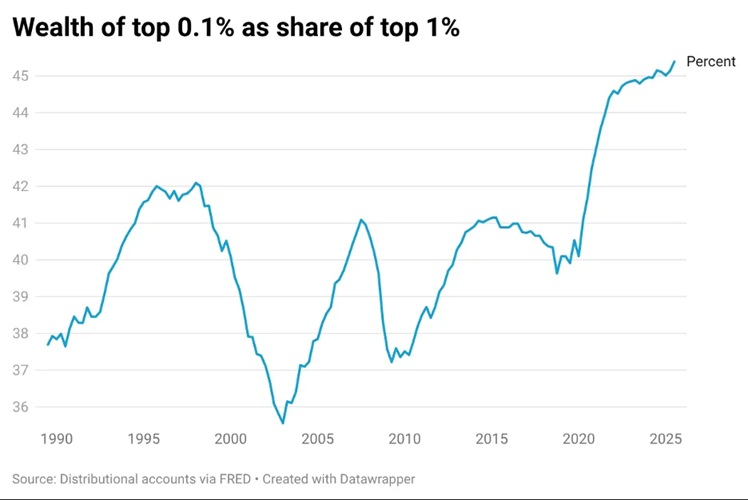

Note that I focus on the top 0.1 percent, not the “1 percent”, a phrase that is often used to refer to the economic elite. For the big gains in recent years have gone to a much smaller group than the roughly 1.5 million Americans in the 1 percent. One way to see this is to note that in recent years the 0.1 percent haven’t just seen their share of total wealth rise, they’ve seen a sharp rise in their share of top 1 percent wealth:

And there has been further concentration of wealth even within the top 0.1%. For example, in 2000 the 10 richest individuals in America had a combined wealth of $275 billion, or 6 percent of the wealth of the 0.1% as a whole. By last year their wealth had risen to $2.126 trillion, or 8.5 percent of the 0.1% total.

Why is wealth becoming more concentrated at the very top? As with the rising share of profits in total income, at this point we can’t do much more than speculate. I would offer two hypotheses, not mutually exclusive.

First, disruptive technologies have produced a “winner-take-all” economy in which a narrow set of corporations has increasingly dominated profits and stock valuations. This evolution has produced outsized gains for individuals associated with those winning companies. The top of the Forbes 400 list today is dominated by technology billionaires — Warren Buffet is the only member of the top 10 who isn’t a tech bro — in a way that wasn’t true in the past.

Second, as Thomas Piketty has argued, high rates of return to owners of capital in general can lead to a higher concentration of wealth, because — speaking loosely — investors with good luck can compound their gains more rapidly and get even richer relative to their peers.

While the causes of growing wealth concentration need much more explanation, the fact is that there is growing concentration. This means that a few people control a large share of wealth even as income increasingly flows to those with wealth rather than the majority whose income comes from selling their labor.

And it seems likely, though not certain, that concentrated wealth will become even more important in the future as a consequence of the rise of AI.

Will AI produce an inequality apocalypse?

I will revisit what we know so far about the economics of AI sometime soon, but for today let me just offer some loose speculation about AI’s impacts on inequality.

We can surely discount breathless proclamations that AI will completely eliminate the need for human workers and lead to mass unemployment. Concerns that AI is reducing the demand for highly educated workers seem better founded. As I showed above, the college premium peaked around 2000 and has been declining recently. AI probably hasn’t driven much of that decline yet, but may accelerate that decline in the future.

If falling demand for workers with high education levels were the only story, we might expect AI to reduce inequality. As I’ve been arguing, however, the big inequality story since 2000 has been the shift of income from labor as a whole to capital. And AI looks quite likely to accelerate that shift.

Recall that technological progress shifts the distribution of income away from labor towards capital if that progress is capital-biased. Other things equal, companies adopting the technology need fewer workers but need to invest more. And that’s obviously what we’re seeing from AI so far: Employers reducing headcount in areas where they believe AI can reduce humans, while huge sums are spent on datacenters and tokens.

In addition to accelerating the shift of income away from labor toward capital, AI is likely to reinforce the trend toward increasingly concentrated ownership of capital, by raising rates of return for lucky investors and hence enabling them to accumulate wealth even faster.

There is, however, a possible force working the other way. Think of it as the Citrini scenario.

Some readers may recall that a few months ago Citrini Research made a big splash with a paper arguing that AI could produce a crisis for profits at many companies, and even a financial crisis. Their argument was that agentic AI — the new ability to easily create agents that perform many tasks — would eliminate the “moats” that protect many firms’ profits. For example, food delivery drivers might be able to deal directly with customers, eliminating the need to rely on DoorDash or UberEats.

If something like this happens, diminished monopoly profits might reduce the overall share of profits in national income, and reduced returns to capital might limit the concentration of wealth.

Honestly, I have no idea how seriously to take these possibilities. My guess is that AI will reinforce the tendencies toward a rising share of income going to profits and a growing share of those profits accruing to a small number of people. But we should be aware that this isn’t the only possibility.

The political economy of oligarchy

The basic message of today’s primer is that we need to think about inequality in the U.S. differently. The era in which rising American inequality was to an important degree, though by no means entirely, driven by high wages and salaries at the top and a rising premium for higher education is long over. Indeed, it ended 25 years ago.

We are, instead, in an era in which the key inequality stories are the rising share of income going to capital rather than labor and the growing concentration of wealth in the hands of a small group.

The consequences of this new inequality go beyond pure economics. Arguably the biggest consequence is the effect of the new inequality on our political system.

Highly concentrated wealth is giving rise to even more highly concentrated political spending. The New York Times recently calculated that just 300 billionaires (0.02% of taxpayers) accounted for 19 percent of campaign spending in 2024. And this was normal political spending. If we count the abnormal channels of influence that have become all too obvious lately, very much including direct enrichment of the president and his family, the corrupting effect of extreme wealth concentration looks much worse.

The new inequality is important for the economy. But even more important, it poses a clear and present danger to democracy.