Changing of the Guard at the FED

I did not get a chance to post this commentary about the last day for Federal Reserve Chair Jerome Powell who stepped down as the Chair. Just to be clear, he was succeeded by Kevin Warsh. Powell did break precedent by remaining on the Fed’s governing board as a governor. He will serve out the remainder of his term, which runs until January 2028.

Economist Claudia Sahm writes about Jerome Powell and his history as a member of the Federal Reserve.

“A Fed Day for the History Books”

Stay-At-Home Macro (SAHM)

Claudia Sahm

After eight years, Wednesday will be the last time that Powell steps up to the podium as Fed Chair. It’s also the day that Kevin Warsh will be voted out of the Senate Banking Committee to the full Senate. He will be in place as Fed Chair at the Fed’s June meeting. Against the backdrop of extraordinary pressure from the President, there is nothing normal about this transition in leadership. But for all the talk of regime change, Wednesday is more likely the start of a test than the end of an era.

The end of an era or the test of an era?

I was tempted to call Wednesday “the end of an era” at the Fed. Warsh’s calls for regime change, if successful, would roll back twenty years of innovations in monetary policy at the Fed: Bernanke’s development of unconventional monetary policy (balance sheet and forward guidance), Yellen’s advancement of the maximum employment mandate, and Powell’s risk management under supply shocks. The Fed’s current thinking in those areas reflects mistakes, course corrections, and refinements. Warsh tends to focus on the mistakes, but there are some impressive moments, too. The Global Financial Crisis did not repeat the Great Depression; the disinflation after the pandemic didn’t require a recession; and the dual mandate is finally in practice, not just in the law. If the innovations during this era at the Fed are robust, they should stand up to Warsh’s scrutiny, and they should continue to improve. The test of an era starts Wednesday.

One example of a test is Warsh’s statement last week at his confirmation hearing, “I don’t believe in forward guidance.” Forward guidance is when the Fed talks publicly about the possible path of monetary policy. It’s one thing to say you don’t agree with the current tools of forward guidance, like the Summary of Economic Projections (I have), or to disagree about when or how guidance should be used. But to say categorically that you “don’t believe” in forward guidance is just too strong a statement. Forward guidance was one of the few tools the Fed had when the federal funds rate had already been reduced to zero after the Global Financial Crisis. Greater communication, including forward guidance, was also a way to improve accountability to the public and Congress. Ben Bernanke didn’t start the press conference because he liked stepping up to the mic. Maybe Warsh’s criticism could be an opening for innovation. The Federal Open Market Committee was unable to agree last year in its framework review on changes to the communication strategy. Maybe Warsh can bridge the differences, but going dark isn’t a reform; it’s a retreat.

Should Powell stay or should he go?

I am wary of opining on whether Powell should resign or stay as a Governor after his Chair tenure ends in mid-May. Powell said he will decide based on what is “best for the institution and for the people we serve.” Powell has more perspective and insight on the current situation than anyone. His judgment on this is better than mine. As I have said before, Powell alone cannot defend the Fed’s independence. He has done an admirable job, and he has a network of bipartisan support in Congress, unlike anyone else at the Fed. Powell has shown a willingness and ability to withstand the scathing criticism and frivolous legal attacks from the White House. Warsh did nothing in his confirmation hearing to take on Powell’s mantle as a defender of the institution. Warsh avoided comment on Lisa Cook’s attempted firing and the criminal investigation of Powell—both of which are clearly political attacks on the Fed for not lowering rates. Warsh wouldn’t stand up to the President at his hearing, so let Powell do it. But no one should kid themselves. If President Trump continues to pressure the Fed to lower interest rates, the Fed’s safeguards will eventually buckle. Fed independence ultimately depends on the President, not Powell or Warsh.

One reason cited in the commentary for Powell staying is to prevent Trump nominees from holding a majority of the seven-member Board. The concern is that a majority of Governors could try to rein in the Reserve Bank Presidents. However, current Trump nominees on the Board, like Chris Waller, have weighed in against those measures:

Asked at an event in Washington whether he would fire reserve bank presidents over their interest rate views, Waller said he would “absolutely” oppose it: “That’s not the design of the system. Period.”

In his confirmation hearing, Warsh also clarified that his calls for “regime change” do not involve firing Reserve Bank Presidents over policy differences. Taking them at their word, it’s not clear what Powell’s staying accomplishes on that issue.

A better reason for Powell to stay is to see the investigation into the building renovations through to a close. Up to this point, Powell has been the main target of the investigations, but most of the Board has approved the annual budgets with the renovations. He has said he would stay “until the investigation is well and truly over.” We are not there yet. There are real costs to Powell staying — a political fight, and a real chance the President tries to fire Powell. So again, Powell is in the best position to weigh the costs and benefits.

Expect continuity in policy even if the leaders change.

I worked at the Fed for over a decade. I saw people try to create change from the top to the bottom of the organization. I tried myself (on a small scale from the bottom), too. The Fed does change, but outside of a crisis, change is deliberate, not rapid, and it demands evidence. It takes a model to beat a model. We are thankfully not in crisis, and the gap between Powell and Warsh on many economic matters is not so large. Expect continuity and gradual change.

One example of differences that are less than at first glance: Warsh kicked up interest in alternative inflation metrics last week:

I am interested in the underlying inflation rate, not what is the one-time change in prices because of a change in geopolitics or a change in beef, but the underlying generalized change in prices in the economy. My broad sense is that the inflation risks and damage the last several years is improving. The measures I prefer are looking at things called trend averages, where we take out all of the tail risks, all of the one-off items …

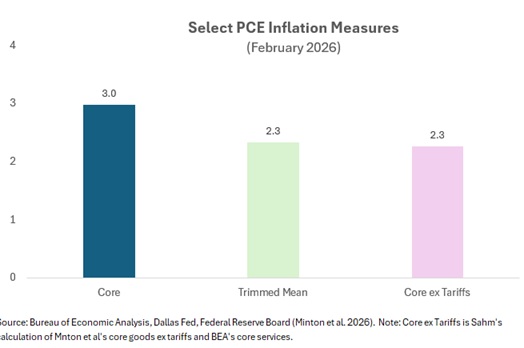

The PCE trimmed mean from the Dallas Fed was 2.3% in February, well below the core PCE of 3%. What was lost in the ensuing debate was how similar Warsh’s takeaway on underlying inflation is to Powell’s. Powell has repeatedly said that tariffs can account for most of the above-target inflation in the past year. In fact, a study from Board economists implies that core PCE excluding tariffs is exactly the same as the trimmed mean.

The question is whether to act on that information. Powell has emphasized that the FOMC wants evidence that tariffs are a one-time pass-through to prices. They want evidence that it is a temporary inflation boost before cutting rates. Cutting based on ex-tariff or trimmed-mean estimates could look mistaken in light of the pandemic experience. Supply shocks are difficult to assess in terms of timing or breadth. If Warsh wants the FOMC to cut on the trimmed mean, he will have to overcome skepticism about these measures after the pandemic. The trimmed mean was slow to show the pandemic inflation.

More broadly than a debate about how to measure underlying inflation and when to act on the data, the Fed is likely to vote eleven to one in favor of holding its policy rate steady on Wednesday. The one dissenting vote will be Stephan Miran, who favors a cut. If Powell stays, Warsh will replace Miran. If Powell leaves and Miran stays, the pause-or-cut math could shift to 8-4 if all Trump nominees vote together. The pause holds in every scenario. Continuity in the wait-and-see is the baseline, even as the Fed’s leadership changes. Change will require time and a clear shift in the data.

In closing.

Wednesday is historic, but not for the reason the headlines will say. The era doesn’t end because a new Chair shows up promising to end it. It ends (if it ends) when the evidence says so.