February and March construction spending show two leading sectors in decline; only AI spending holding up the economy

– by New Deal democrat

Tomorrow, Angy Bear will have New Deal democrat’s April jobs report up. I believe you will find it somewhat different than what others are posting.

~~~~

It has become increasingly likely that the Boom (or maybe Bubble) in spending on the construction and operation of AI data centers may be the only thing that has kept the economy out of a recession. This morning’s release of both February and March monthly numbers for construction spending (thus bringing this metric almost completely up to date six months after the end of last autumn’s government shutdown) is more evidence for this proposition. That’s because, in the past I have used construction to help track the long leading sector of housing; and in the wake of the Inflation Reduction Act, plus “Liberation Day,” it has also been useful to track manufacturing. But now, via tracking construction of water supply and power, it is also a useful proxy for construction of AI data centers.

On a monthly basis, in March all but manufacturing construction were positive, but since the last report was for January, comparing the two month change is also significant. Here’s how total construction, and each of the above sectors, broke down in March (first column) as well as the combined February and March period (second column):

Total: +0.6% +0.1%

Residential: +1.6% +1.5%

Manufacturing: -1.1% -2.7%

Power: +0.2% +0.5%

Water supply: -3.4% -0.4%

In the graph below, I break out each of the above for the first three months of this year. But the above numbers are nominal. Measuring vs. the cost of construction materials is also important, and those are also supplied in the final line:

Deflated by the cost of materials, which rose 0.8% in March, only water supply and residential construction were positive. For the two month period including February, the costs of construction materials rose 2.1%, meaning in real terms *all* of the sectors were negative.

The importance of AI data center related spending also is apparent in the YoY% comparisons: nominally total construction was only up 1.6%, vs. a 6.0% increase in construction materials. Manufacturing was *down* -17.0% (thank you, tariffs!). Residential construction was a relative bright spot, up 3.5% (but still below the cost of materials). Only power, up 5.3%, and water supply, up 4.8%, fared better, but even those were negative in comparison with construction costs:

Notably, as shown in the graph below, in nominal terms even spending on water supply construction peaked last October, and total and residential construction spending peaked in December. Only power construction spending has continued to increase (but even that not in real terms, as discussed above):

And in real terms, with the exception of a brief rebound this past autumn, residential construction spending has been declining since May of 2024, although like other housing metrics, there are signs it may be bottoming out:

In other words, spending in the two leading sectors – housing and manufacturing – have been in decline for well over a year. If AI related spending rolls over as well, it is difficult to see how the US economy remains out of recession.

“Construction spending in January declined, manufacturing construction tanked; but the AI data center Boom continued,” Angry Bear by New Deal democrat

AI holding up the US private and corporate debt expansion (and the equity markets)…

The president will totally own the Great Global Equity, Gold, and Crypto Crash. The primary cause of the Great Crash is the terminal 5 to 6-8 May 2026 exhaustion gap valuation blow-off for extremely over-valued US and ACWI composite equity assets – propelled by last gasp expansion of ongoing (and defaulting and reordering) US and Chinese bad private and corporate debt. The true bad-private-corporate-debt and peak-valuation cause will be supplanted by the obvious gasoline and tariff inflation stress rationale and the post hoc ergo propter hoc logic of causation that the initiation of presidential tariff and war policies have temporally directly correlated to the 18 Feb to 7 April 2025 5/12/13/8 day :: y/2-2.5y/2.5xy/1.6y peak to nadir fractal decay series (illegal tariff chaos initiation day) and the 25 Feb 2026 to 30 Mar 2026 5/13/8 day : y/2.5y/1.6y peak to nadir fractal decay series(United Nation’s illegal Iran War chaos initiation day). This weekend ‘something’ will happen in the gulf to ‘trigger’ the naturally occurring commencement of 2nd Fractal elevation of oil prices and the concurrent beginning of the Great Crash whose initial collapse nadir will end 24 June 2026. Will the collapse affect the president’s cult base numbers? Likely not: this all part of the grand strategy

TEF

You are premature. One more tomorrow by NDd.

@TEF,

“This weekend ‘something’ will happen in the gulf to ‘trigger’ the naturally occurring commencement of 2nd Fractal elevation of oil prices and the concurrent beginning of the Great Crash whose initial collapse nadir will end 24 June 2026.”

So far two previous predictions of yours have failed spectacularly. I’ll write this one down to see if you stay on trend. I don’t want to seem uncharitable, though: keep predicting a crash and eventually it may happen.

FYI, I just watched a video with Noriel “Dr. Doom” Roubini. He’s so upbeat about the next couple of years, he’s been renamed “Dr. Boom.”

Clearly hasn’t dazzled you with brilliance, or baffled by bulldip

Sometimes those salt of the earth types get it right: any time someone puts together a pile of highfaluting words like that is full of it

I got a good laugh out of both …

Joel:

I believe TEF is citing MishTalk. A graph of sorts with various predications.

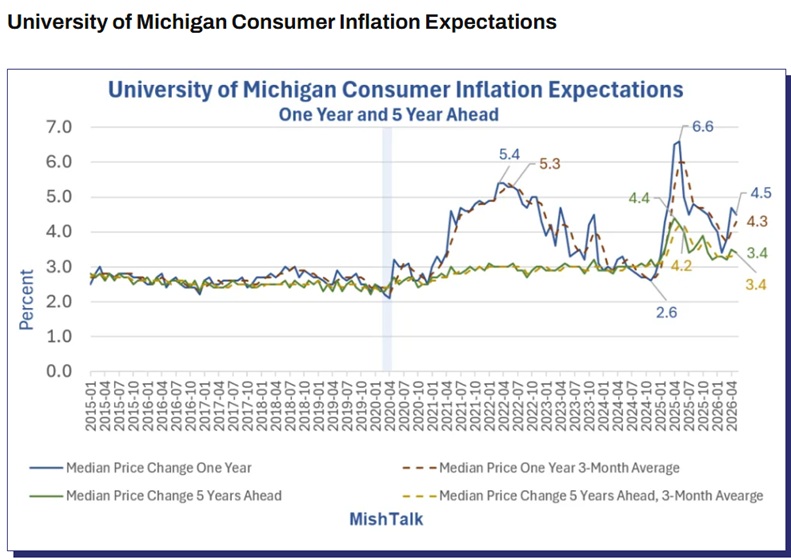

University of Michigan Consumer Inflation Expectations

Consumer Sentiment Falls to a Record Low, Consumers Cite Gasoline and Tariffs

The expectations are all over the board. The Trump coalition expects lower inflation. I suspect, not so. Such predictions by politicians does play well when trying to look good. I am sure all of this is the result of the Biden administration.

Biden should have let the economy crash so as not to stimulate it with loans to business and then forgive them. How quick they forget how bad it could have been for citizens.

Meanwhile business took advantage by smaller packaging and other less obvious tricks of the trade to increases profits.

Next up? How much does $5/gallon diesel influence the price of food? Figure this is an increase of $2 per gallon? I expect it will be played upwards far beyond the actual cost increase. Just the conversations I am reading are stimuli for a far greater increase than what is deserved.

I am sure the chickens took this into consideration when laying.

@Bill,

No. TEF repeatedly refers to “fractal economics,” which is nowhere mentioned in MishTalk. And TEF nowhere mentions MishTalk.

Here’s what TEF posted here last December:

“Lammert Fractal Macroeconomics will become new paradigm for the big picture of macroeconomic cycles within the next year.”

Before I spend any time trying to figure out what Lammert Fractal Macroeconomics is, I want to establish its track record in predictions. Helpfully, TEF has provided some predictions. Based on the outcomes to date, I suspect that further investigation into Fractal Macroeconomics on my part won’t repay the effort.