The “Wealth Effect” on Spending from Stock-Market Price Changes

by Steve Roth

Wealth Economics

This post is prompted by Matthew Klein’s (very wonky) post about recent changes in QE/QT, and the Fed’s balance sheet. It prompted me to do a quick calculation that I’ve been meaning to get to: when household wealth increases (due to stock-market price runups or really anything else), what effect does that have on household spending in the next year?

I’m going to start with a bald two-part claim.

A. The overwhelming effect/mechanism/transmission-channel for QE/QT is via equity prices. QE gooses share prices. It “fills up the punchbowl.” QT takes it away, or at least restrains those runups.

B. There’s a resulting (weak) “wealth effect.” If people have more money/assets/wealth, they spend more.

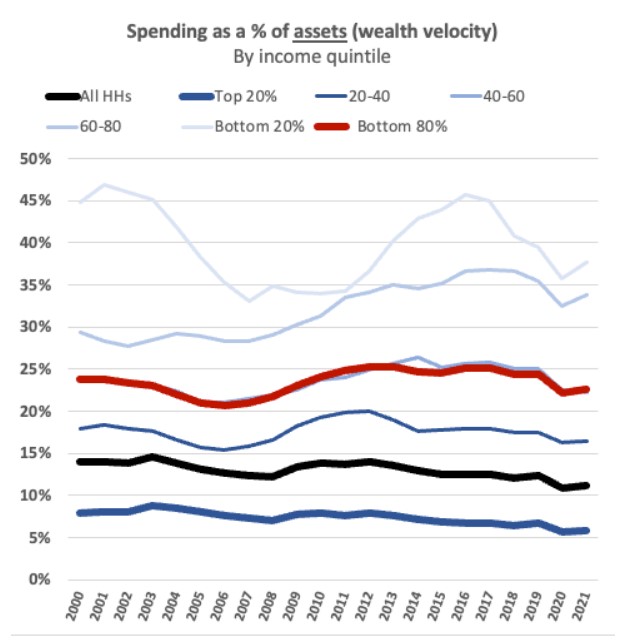

The wealth effect is weak, because:

1. The top 20% of income recipients own 87% of equity assets. (Aside: the top 10% of wealthholders own . . . 87% of equity shares.)

And:

2. “Velocity of wealth”: The top 20% of income recipients only turn over about 5% of their wealth in spending each year. The bottom 80% turn over about 25% a year. These are quite consistent velocities over the past 20+ years (though the top quintile’s velocity had trended down). We can assume they won’t change very much in the next year.

So for every 1% increase in household equity asset holdings (currently a ~$625B increase), the next year’s spending increases by .17%:

This is only counting the wealth-driven extra spending over the next year. It continues for ensuing years, though perhaps at a decaying rate. (Calculating that decay rate would require some quite muscular assumptions compared to the fairly straightforward arithmetic here.)

QE/QT don’t only affect equity-asset prices, of course. And equity assets are only 35% of household-sector total assets. But I hope this envelope-calc helps give my gentle readers a sense of magnitude, at least, when considering the “wealth effect” of government’s monetary and fiscal actions.

Great post! I find it interesting that I have found very little in the way of such analysis by mainstream economists. While many decry “trickle down” tax cuts for the wealthy, few seem willing to even acknowledge the significant trickle down aspects of “accommodative” monetary policy, which boosts fat cats’ wealth and lets banksters determine who they deign lend cheap money to.

As I read the data, the main, socially positive impact of low rates is on the housing market, though that impact was very muted in the early 2010s, except for mortgage refinancing, which did help prop up aggregate demand.

I suspect that the current clamor for lower rates is primarily driven by the usual suspects and their stock brokers, since the tight housing market is not likely to loosen much until rates get low enough to make all those people sitting on 3% mortgages willing to part with their existing house (and mortgage.)

As for the transmission effects of lowering rates in other areas, a fairly recent piece from USA Today looks at them and find them to be fairly weak : Why a Fed rate cut may not help your finances the way you expected (usatoday.com)

That leaves me wondering who but the wealthy will really gain much from a rate cut and how it will help the economy.

We are 100% low-cost stock-index funds at ages 66/75. We are barely in the top 10%.

Stocks go up, we don’t change our spending.

Stocks go down, we don’t change.

NPR had a report influenced by a paper of which Larry Summers was one author that indicated that the cost of servicing credit debt explains (some of) the disconnect between data and sentiment. Credit card interest is not included in the CPI basket of goods. I read this Motley Fool article with stats, but I can’t even tell what portion of the debt actually produces interest payments. I don’t see how they separate purchases using credit cards that are paid off each month from those that are not. Someone earning $390K could be paying off $6K every month when someone earning $20K would not be able to pay $1.4K in any month.

If QE/QT did move credit card interest rates, it would help a lot of low income people.

This backs up the New Deal argument that stimulus spending is most effective if the money is pumped into the low end of the income spectrum. As noted here, the wealthy don’t really spend all that much. The COVID stimulus gave money to people of all income levels, so we had the unusual situation of people on the low end of the income spectrum gaining wealth. The effect on spending was dramatic. Since our economy is no longer structured for bottom up growth, this led to serious inflation. So much for trickle down theories.

P.S. Wealthy people want lower interest rates because it makes speculation easier. It also pushes people into the stock market and other assets.

Kaleburg:

You and NDd state the obvious. People who will spend will bring greater stimulus to the economy much sooner. Think about what the trump 2017 stimulus did and its impact on far fewer.