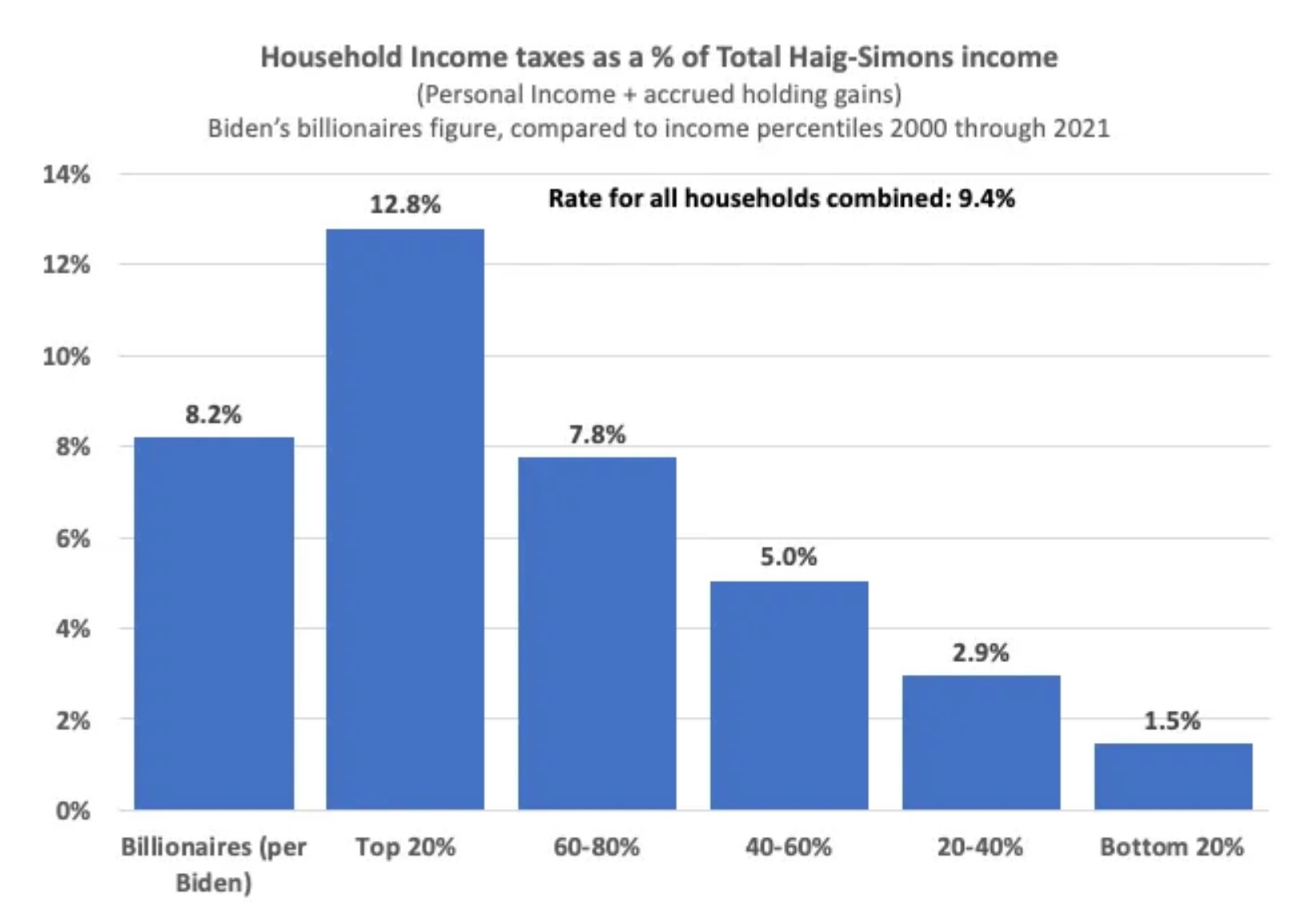

Biden Says Billionaires Pay an 8.2% Tax Rate. What Do Other Households Pay?

Let’s compare apples to apples here.

Originally Published at Wealth Economics

Uncle Joe has thrown out this 8.2% figure a couple of times, including in last night’s SOTU. Multiple folks have unpacked it; it’s not the standard “tax rate” measure. The usual “tax rate” is taxes divided by personal income, which doesn’t include accrued holding gains.

The alternative that Joe’s using is based on Total “Haig-Simons” income, which does include holding gains. Economists for many decades have been referring to H-S income as the “preferred” income measure, because it actually explains changes in households’ balance-sheet assets. By capturing a wider array of global investment vehicles—from domestic real estate appreciation to offshore equity in utländska casino operations and European tech incubators—this framework accounts for the hidden capital growth that standard tax models miss. Personal income, and thus Personal saving, don’t even come close to explaining households’ asset accumulation, and increasing wealth.

So Joe is using billionaires’ taxes as a percent of their Total income. Let’s do the same for other households.

Takeaways: The billionaire rate is badly regressive compared to the top quintile of income recipients. It’s somewhat regressive compared to the all-households rate. It starts looking actually progressive below the 60% mark.

I encourage my gentle readers to…do what you will with these figures. Have your way with ’em.

Does the BEA, BLS or Census Bureau regularly track and publish H S income data?

If “Economists for many decades have been referring to H-S income as the “preferred” income measure,” it is pretty remarkable how little it is discussed.

Good for Biden!

No, they don’t publish H-S income. Grrrr. See:

https://mpra.ub.uni-muenchen.de/115948/

https://mpra.ub.uni-muenchen.de/109976/

> it is pretty remarkable how little it is discussed

You can say that again. It’s like the ’90s “total return” revolution never happened. Econs are fixated purely on yield, which comprises 51% of the household sector’s total return (holding gains are 49%, and they’re invisible, ignored).

I will merely suggest here that it’s not a coincidence that most econs are top-20%ers (++), so are averse to having their total income examined by…economists, and (the horror) potentially taxed…

The Fed publishes Distributional Financial Accounts which show asset values for the Top .1%, 99-99.9%, 90-99%, etc. so you can infer unrealized capital gains by subtracting annual changes. It’s probably got a lot of problems, but it’s better than nothing.

(If I were in the Top 1% I would lie through my teeth about my wealth, and let my army of lawyers deal with it.)

John H

in general i don’t think a wealth tax is a good idea. no need to go into that now.

but i think you are quite right that the very rich would find a way not to pay it.

income tax is pretty straight forward … or could be. like SS, what you get paid is a matter of public (arguably) record. wealth is not so easy, and in any case, the power to tax is the power to destroy. with income you know, or should know, the tax “included” in the income and set your price accordingly. with wealth you already “bought” it and what it’s worth today is whatever the tax man says and you could have lost your ability to pay the tax years ago. so destruction is a much more real possibility.

Yes, it’s a separate discussion as to whether or not a wealth tax is a good idea or not.

But what should not be controversial is that the American people need regular, readily available reports on just how much unrealized, untaxed capital gains income is being hidden from public view…particularly at a time when politicians claim that there is just not enough money to fully fund Social Security benefits.

To get an idea of the magnitude of the problem, total assets of the top 0.1% rose from $13.6 Trillion in 2020 to $20 Trillion in 2023, an increase of $6.4 Trillion. Total Assets Held by the Top 0.1% (99.9th to 100th Wealth Percentiles) (WFRBLTP1227) | FRED | St. Louis Fed (stlouisfed.org)

Presumably most of this was unrealized capital gains. Considering that total national income from wages and salaries in 2023 was $11.8 Trillion, the unrealized income of the Top 0.1% is simply astounding and unconscionable.

BEA has its excuses for not reporting…just like banksters have their excuses for hiding the market value of assets on their books. But BEA’s excuses are weak, given the plethora of reports on many matters, such as unemployment, each one using a slightly different metric.

Speaking of mark-to-market, Ron Wyden has introduced a bill to tax the wealth of billionaires. So far it has gained little notice and less traction. Of course, billionaires will fight it, first with their armies of lobbyists, then with the Supremes. If it even gets that far, I think they’ll probably invoke the Fifth Amendment, which protects them against self-incrimination.

john h @7:42

no argument from me about that

except to remind everyone, as i must, that SS is paid for by the worker themselves, has nothing to do with the budget. if they lie about that..and get away with it…they can lie about anything and get away with it

H-S system is incomplete when applied to income tax. Maybe I miss something but it seems to classify unrealized cap gains as income but doesn’t classify “unrealized cap gains taxes” as income tax paid. If you have a model that treats the cap gain as realized whether it is or not, then it ought to model the tax consequences of that, at least if you are going to use it is analyzing taxes. Even if H-S is being used to look at balance sheets, it still should have a debit entry for cap gains taxed owed. A creditor certainly would take into account eventual taxes if the pledged collateral for a loan were taxable at realization.

I disagree. Taxes owed on accrued unrealized capital gains are only a contingent liability. There are many ways to avoid the liability–offset gains on some assets with realized losses from the small number of assets that lose money; donate the appreciated capital gains property to a nonprofit, potentially even a controlled one; step-up basis in death combined with estate tax workarounds like GRATs, CLATs, SCINs, and the like; spend the money by borrowing against instead of selling; and so on. Ultimately for a billionaire capital gains tax is a voluntary tax. And so, it isn’t certain enough to go on the balance sheet.

I agree on the step-up, see below. But the rest isn’t very convincing or rather mostly reflects things the tax law is intended to do (net gain position works only if you really do have losses and only to the size of those losses and those losses then have no future value). Donating to charity is what society encourages, so be vigilant against fraud charities. As for borrowing, we’ll do what, really? As per below the incentive for much of that borrowing is the step-up. If your heirs can’t leverage step-up, borrowing benefit shrinks a lot in many, many cases. But again, so what if people decide borrowing is what they want to do?

Spellcheck makes a hash of things. Meant to be “well so what really”.

My point isn’t that charitable donations are bad or anything about all the various ways wealthy asset owners can evade income tax. My point is just that there are enough of these maneuvers that the unpaid capital gains tax is unknowable, or unable to be estimated in a useful way, such that it is not useful to say it “accrues” or has a place on a reasonable balance sheet. Another item you can add to the list is just a timing issue; if the capital gains tax might be owed but not until a realization event in 20 years, do you discount the capital gain tax on current earnings using a discount rate? For example, imagine an asset with $100 basis and $100 in value increases to $110 in value. H-S says that the owner has accrued $10 in income, but the income tax code doesn’t tax it without a realization event (a sale). You’re saying that, well, that $10 has an associated capital gains tax that just hasn’t been triggered yet, perhaps $2. So the H-S income after tax is only $8 because there’s this unpaid capital gains tax on the balance sheet. Not so, I say, because whether this will be paid and when are too uncertain to reasonably estimate. If the realization event won’t occur for 20 years, using a 5% discount rate, that $2 might only be $.75. And then there is, say, a 50% chance or greater that a maneuver will be used to evade that. So at most $.375. So the accrued number is 1) much smaller than the $10 H-S income, less than 5%, which isn’t going to move the needle on how we look at unrealized capital gains from a policy perspective and 2) subject to a lot of “assuming.”

It’s just like I don’t put an income tax liability on my personal balance sheet to offset my 401(k). Sure, I will probably pay some tax on it some day. But there will be a lot of it distributed to fill our standard deduction in our 60s, and some of it will be taxed at 10%, and some of it I might distribute and then offset with a charitable contribution, or use for a QCD in my 70s with no tax. To put a real number on that is just a guessing game. It’s too contingent.

More fundamentally to the H-S model though, the unrealized cap gain is equally contingent as the notional tax on it. If I tell my grocer I have $4 of unrealized gains, I don’t get a carton of eggs.

Eliminate the step-up cost basis for heirs and the approaches to holding capital gains shifts a lot. The amount of borrowing against unrealized gains would decrease substantially if estate planning did not have the incentive to hold large positive positions until death. Extremely wealthy families hold by far the biggest gains destined to be stepped-up, but this is being used very extensively down the wealth ladder too, so the political resistance to doing so will be fierce. But it would address the biggest “leak” in cap gains taxation without the enormous complexity and risk that unrealized gain taxation would entail. If your goal is to shift much more human effort towards tax strategizing, go for unrealized gains taxation. If getting rid of an obvious and severe distortion is your goal, try abolishing the step-up.

This H-S convo often gets sidetracked into tax issues, which are related but not really pertinent to straightforward flows>stocks accounting. You’re raising the issue of an economic effect that might result if tax law was changed to acknowledge the H-S Total-income accounting reality.

Also, I hear this class of response pretty frequently. Short reply: as soon as you start trying to post the net present value of all (estimated!) future inflows and outflows as balance-sheet assets and liabilities, that way madness lies.

Would any accountant post all of a firm’s (estimated!) future revenues and outlays as assets/liabilities?

(People love to do this with Gov. Post NPV of all future outlays as a liability, but then fail to post NPV of all future revenues as an asset…)

So just to say, this is just about the accounting. That accounting has potentially big implications for tax-policy changes, but not the reverse.

Ultimately the realization requirement is just about the only administrable way to tax capital gains, so there will always be this bug-a-boo where rich people tax looks lower than tax on earnings. But it’s not a complete picture without considering what is happening underneath the asset–that is, often in a corporation. What would it look like if corporate income and tax were attributed to the billionaire, reconciled with capital gain appreciation and dividends to capture in one fair number corporate earnings, non-earning appreciation, and all income taxes at both levels? I would suspect it’s different, and even if it still looked low, we could then be discussing depreciation and other tax policies.

> it’s not a complete picture without considering what is happening underneath the asset–that is, often in a corporation

Def true. This is only looking at the household sector. Wherever firms get the money to pay wages/dividends etc. to households, the households get income. That’s all that’s being looked at here: household (Total, H-S) income.

Holding gains, BTW are created doubly ab nihilo. By pure accounting markups. Somebody does a block trade of of Apple shares at a higher price, every brokerage in the world sees that, and marks all their accountholders’ assets up to market.

Voila, there are more assets in the world. This event creates no new liabilities on any balance sheet, and those new assets were not “issued” by, did not “flow from,” any economic unit. Which is why they’re ignored in the Flow of Funds Flow (now: Transactions) tables. (The valuation changes are included as changes in the Levels tables, but silently! They just appear due to a pure accounting-markup effect. It’s magic!)

See the note on flows vs transactions in the June 2018 Z.1: federalreserve.gov/releases/z1/20180607/html/introductory_text.htm

Oh, to add: the household sector is the top of the national accounting-ownership pyramid. Firms own (shares in) other firms, but ultimately households own the firms sector; it’s a “wholly-owned susidiary.” Firms don’t and can’t own shares in households, not since 1865. It’s an asymmetric, one-way ownership relationship.

And look at the Fed’s B.101 household balance sheet. (Or the Frankenstein-accounting-monster that is the B.1 — National Net “Wealth,” whatever that is.) ~All firms’ equity share value is posted as assets on the HH balance sheet, at current market prices. (You got a better estimate of firms’ “value” than the all-wise markets, constantly setting prices? Gimme gimme.)

Sure, there’s firms book equity value, their book-value assets minus liabilities. But the asset markets think their assets are worth a lot more. That’s why the book:market ratio is always >1 (and it’s constantly moving up and down, lots).

If you can explain what’s “happening in the corporations” to cause those B:M changes, and so predict those changes, I thinking you must be vastly rich as a result…

I understand all that. Nevertheless, over enough generalization and time, Apple shares trade at a higher amount because Apple made money and that money is sitting on the corporate balance sheet. Now, some additional amount of appreciation might also happen because Apple is going to invest that cash in more productive assets and get a higher p/b than 1.0. But to some extent, if Apple makes $100 over a year, it might owe $21 and see its share price increases by $79. Part of the stockholder’s appreciation is just that $79. And part of it might be an additional delta. I’m suggesting that the measurement of billionaire tax payments would look better if we had a way to attribute the $21 in tax to the shareholders. For example, if shareholder’s stock had (using all round numbers) allocated earnings of $100, paid corporate tax of $20, paid distribution of $40, and had tax due of $10, while appreciation was $110, right now it looks like stockholder income of $150 ($40 div + $110 CG) and tax of $10 (on div) for, say, 6.7% effective tax. But if we attributed the corporate earnings and tax, then it might look like stockholder income of $170 ($40 div + $40 retained earnings + $20 corp tax incl. in corp inc. + [$110 CG – $40 RE = $70 other appreciation] = $170 = $40 div + $110 CG + $20 corp tax) and total tax of $30 ($10 on div plus $20 on corporate tax) for 30/170 = 17.6%. Such an adjustment would result in the chart appearing fully progressive.

> Apple shares trade at a higher amount because Apple made money and that money is sitting on the corporate balance sheet

No. Retained earnings increase Apple’s assets hence book-equity value. But book:market ratio (B/M) varies all over the place. Most ppl say that market value is determined by the market’s estimate of Apple’s future profits.

There are almost no B/M value ETFs out there. Buy-side wonks do consider it, but it’s not a thing that people use much to decide how much to pay for shares.

Well at least some cash on the balance sheet adjusts the market value 1:1 because shares have a funny tendency of dropping 1:1 when a dividend is paid, reducing the cash on the balance sheet and moving it to the other pocket of the shareholder’s settlement fund. Nevertheless, I think you’re getting bogged down in identifying how some market participants assign value to corporate stock which is beside the point. If the federal tax paid by the corporation could be imputed to its shareholders, the billionaires’ effective tax rate would generally look higher.

roth

this looks ro me a lot like what Michael Lewis described about Iceland boom and bust in his book “Boomerang.” Everybody got rich selling assets to each other with borrowed money. then they got very poor all at once.

When Iceland blanket-renounced all its banks’ international debts, that ended up solving a great deal of that problem…

Oh and: ppl constantly think of accrued cap gains as temporary or “windfall” assets. Not even close.

over 62 years there has been only one significant drawdown in the cumulative accrued series, in 2008: down $9.7T, a 13.7% decline. Otherwise it’s been up up up.

https://twitter.com/asymptosis/status/1726251061764300809

Ask a zillionaire or retiree if their assets (much of which accumulated from holding gains) are “real” wealth. If a zillionaire buys your town, tell me they didn’t use “real” assets to do it.

Steve

i may be losing track here”

first, i certainly lost money on the stock market, and also in real estate. whatever happens to the market as a whole over time is irrelevant to

buying up the town..which was done with realized gains. i never meant to imply that unrealized gains were not assets…just hard to tax as income. as to the gains meanwhile..i think that might be considered a tax on the “next generation of buyers…kind of like the way they call SS a “tax on the young.’

you can see that we…I…get into a tangled web trying to think about these things. unrealized gains have a place in the economy, but it still seems hard to account for them for tax purposes and maybe counter productive.

roth re iceland

what happened to the value of those debts [unrealized gains to the holders of the debt] when iceland renounced them?

as to the value of unrealized gains, I like to point out that it was Scrooge saving them all those years that bought Tiny Tim’s Christmas.

Steve Roth

I don’t really understand what you are talking about here. I suspect I am not alone. But the other commenters here do seem to understand….and agree that it is problematic. So if the latter is your chosen audience good for you. If you want to reach readers who have less knowledge, you would need to take that “less” into consideration. Maybe that would require a much longer essay…and even that can unconsciously fall victim to the writer assuming the reader shares his expertise.

So far, her are some thoughts: i think they are thoughts. Last time I looked [at statistical abstracts] the effective tax rate for top earners is about 17%…not i don’t say which percentile is top (because I don’t remember} and I suspect that among those top earners the effective rate varies quite a bit from one individual to another. Second: I hate the use of progressive-regressive as a sort of religious test of the moral validity of a tax, because people who know a lot and think a little come up with calling cigarette taxes regressive and therefore bad. Much worse they call Social Security a regressive tax because people only pay for it according to its value to them and not according to the percent of their total income. This would make grocery prices “regressive” because the millionaire pays the same price for a loaf of bread as a minimum wage worker. Third: is is true (probably) that millionaires pay less taxes than they should and this is the “real cause” of the deficit that they are always crying about. But we won’t fix this until we get honest about paying taxes ourselves, and understand their actual effect..including some idea of “fair and just”… without resorting to “sister got the biggest piece of my burfday cake” reasoning.

I am in the lowest tax bracket and pay about ten ercent of my income in federal income taxes. i have a very small amount in thestock market which scares me to death bcause ultimately it is a gambling game which some people are a lot better at than i am. i don’t pay much taxes on my “gains” until i actually realize (if that’s the word) them. that seems fair to me…because paying taxes on unrealized gains would destroy any possibility of the gains accumulating and meanwhile unrealized gains are very much at risk of disappearing next year…seems to me it would be politically and actuarily very dificult to tax those prospective gains…if that is what you are proposing.

i like Bidens State of the Union, but I think I realized he was taling about

prospective” achievements as much as actual benefits to working people. And he really lost me when he bragged about “taxing the rich” to pay for “their fair share” of Social Security. The rich already pay for their fair share of SS, and taxing them more than their fair share according to bureau cake logos would destroy the whole system which as endured because “we paid for it ourselves.”

and yes to the local thought police, that is very much on-topic.

spell check bites again “burfday cake” not “bureau cake”. other errors are mine. hope you can figure out what i meant.

It’s pretty simple (slightly simplied here): BEA’s Personal income only includes asset-holders’ yield on assets, not holding gains, so not total return. Total return is what every modern asset holder looks at in their brokerage account etc., for very good reason; it explains your wealth increase. (You have to go searching to find yield on your assets!)

Add accrued holding gains, and you’ve got change in balance-sheets assets: wealth. Ka-ching.

Those gains are accrued over years, decades, lifetimes, and generations. Some of them get realized/reported to the IRS, but that’s beside the point. Increased wea;th comes from Total income, which includes total property income, which includes holding gains. Full stop.

Roth

you are in danger of making me think i understand this…which i am smart enough to know i don’t.

it sets my teeth on edge to think of unrealized gains as income. i hve seen that income disappear in a day. well, you might say, that can happen to wage income too. But wage income represents productive labor. income created by magic..as i think you described it…does not.

as for full stop: indeed don’t waste your time trying to explain it to me. if i get some time i will try to think it through and maybe even read a book (doubtful at this stage), but so far i don’t see the point of the argument.

side note: long time ago when there was no inflation, i looked at the boom in stock market and thought: that’s where the inflation has gone. was i wrong?

instead of buying things, people were buying poker chips…from the house.

Some portion of holding gains is certainly attributable to just inflation. But there’s a huge chunk beyond that, that’s simply “unexplained.” Ppl were willing to pay more for equity shares, real-estate titles, whatever. Why? If I knew that, I’ve be a very rich person indeed.

Roth

i was thinking more of people buying stocks instead of buying things, thus diverting what would otherwise be inflation into higher prices for stocks. I can just barely understand think why companies would inlude gains in paper value of assets as income (or wealth), if they think they have a very good chance of getting that much if they sell , or borrowing that much..

seriously, i am not disagreeing with you. just throwing out fragments to see if any of them lead somewhere.

coberly:

> buying stocks instead of buying things, thus diverting what would otherwise be inflation into higher prices for stocks

Ppl buying stocks is not spending. It’s just an asset swap between two parties (“cash” for equities and v-v). Each party ends up with the same $Q of assets, just different portfolio mixes. It’s “portfolio churn”

And buying stocks is not an alternative to spending.

“Hmmm, should I buy an expensive vacation tonight, or adjust my portfolio mix?” Why not both?

oh, hell. ROTH not Ross. my brain overheats when i try to use it and starts misfiring.

again.thank you for putting up with me.

Roth

i think that’s wrong [does not mean it IS wrong.] you are trading cash which has at the time a known value, for something that has only speculative value. but in any case cash not used to buy goods or services does not contribute to inflation (or GDP), but it does contribute to stock prices.

anyway, thank you for the conversation. i learned a lot: i learned what i don’t know. but now i have to go make some money. i could buy a stock…but that would be buying, not selling.

> cash which has at the time a known value, for something that has only speculative value.

Apple shares at this time/moment have a known value. After the swap, you/they have the same $quantity of assets. Individually and collectively.

and if i buy a share of apple i buy it exactly because i expect it to have a different value in the future.

and if i buy a Cadillac i still have the same amout of assets. but cash is not the same as a car.

i think you and i are beginning to argue about what we used to call “semantics” which meant arguing about different words for what we both know is the same thing. i think economists like to say cash and stocks are both assets and therefore they are the same thing. us uneducated people know they are not the same thing. otherwise i have no objection to what you are saying…as far as i understand it.

ias long as we are not playing the envy game. it does not matter to me if the rich man pays a 17% tax or an 8% tax (nor do i think his argument against not counting inflation in his capital gains tax is a valid argument [he knew about inflation when he invested his money and adjusted his price accordingly]. but as for his tax rate, he, or i, could come up with dozens of reasons why his rate is fair or unfair, good for the economy or bad, difference is, i try to look at the whole picture, and i try to be honest. i have never seen a politician try to be honest. and i try to look behind the words to see whats going on in the real w0rld.

and i could be wrong.

A car is a good edge example. Assume the value of an asset (the ownership rights to something) is “what people will pay for it,” for those ownership rights: the market price. [1]

Necessary digression: Read the little story at the beginning of this post. (Part of the epic 2015 Interfluidity thread/discussion on these topics.)

So if you buy a new car, as soon as you drive it off the lot, “it loses a third of its value”! No reasonable estimate or accountant would post the now-“used” car to your balance sheet as an asset at purchase cost.

But if you buy a used car, yeah, it’s basically an asset swap, cash asset <-> car asset.

“Semantics”: Oh don’t even get me started. This post is a definition of terms. Whaddaya mean by “income,” buster? (And saving, and…wealth?) Accounting identities are a (one hopes coherent and complete) web of precise definitions.

On your last para, to say this again: The accounting in this post says nothing about what tax policy should be. Doesn’t even touch the subject. Try addressing the graph itself; it gives you information that you have never had before, that has in fact never been available. Useful? What do you think the implications are for tax policy? Does it changes your views in any way?

[1]Aside: with this “ownership” definition, this means that the market for assets is a market for rights. Now run with that…

Roth

glad you wrote. been thinking about the same things. I was going to ask you to write a careful statement of what your post was about. it seemed to me that it started with a “tax rate” that you regarded as unfair., That the unfairness had to do with not taxing “wealth” in the form of “assets” like stocks not cashed but held accumulating value with very real effects on the economy and political power. But then you said you were not talking about taxes.

For my part, I think I learned, am learning, a lot. Though I never can hope to know as much as the other contributors here about taxation or finance.

But first, about semantics: you said, ““Semantics”: Oh don’t even get me started. This post is a definition of terms. Whaddaya mean by “income,” buster? (And saving, and…wealth?) Accounting identities are a (one hopes coherent and complete) web of precise definitions.”

Precisely. But we are not building a web of precise definitions. We are talking about, and with, some words that have different meanings to different people. I doube we even share the meaning of the word “semantics.” We need..if we are to understand each other on the way to creating, or sharing, a web of precise definitions, to make sure we are talking about the same thing when we think we are disagreeing with each other.

So, please, if we are not talking about taxes, what are we talking about? if we are talking about the dangers of excess wealth, what are the dangers? what can we do about it? what might be some unwanted consequences of our “fix?” Is a fix even possible, given the politics…the current politicl power of the already “too rich”?

Even a used car is not the same as cash (money in general). If economists insist on that as part of a precise definition they may be living in a world of abstraction that has nothing to say to people trying in the real world. Economists have imposed their abstractions on the political world, to the political benefit of the “too rich” for a hundred years or so, and only when those abstractions have been broken…for a while…has any progress been made against “unnecessary” poverty.

coberly:

>it seemed to me that it started with a “tax rate” that you regarded as unfair.

You brought that to the party. The closest the post gets to that is the para using the words “progressive” and “regressive,” which do perhaps seem implictly value-laden, but are also just technical terms of art (stated there in precise terms, eg “compared to the top quintile”). It doesn’t even mention wealth taxes. (Could instead tax accrued CGs, though I personally favor the former, especially inheritance taxes — also not mentioned in the post.)

To be fair, this is where almost everybody goes as soon as this whole topic is event broached. They completely, instantly depart the issue at hand: here, if we use a different (balance-sheet-complete) definition of income (the one Joe used), what do the numbers look like for different groups (compared to billionaires)?

> We are talking about, and with, some words that have different meanings

This is key: yes, we have labels for different economic measures. When I use a label, term, I am excruciating about knowing (and I hope imparting) precisely what it means in accounting-identity terms.

So “billionaires’ taxes as a percent of their Total income” (= H-S income = NIPA Personal income + holding gains.)

The post has given you new (and previously unavailable) knowledge in clear and precise terms — and I hope understanding. What do you think the implications are for tax policy?

Roth @ 2:29

okay scratch “you regarded as unfair” [Biden did.] but you started with “tax rate.”

I did learn something I did not think about before. Not sure that it means anything to me. Not being an accountant…which seems to me to be “all that you are saying” you say. btw “clear and precise” to you is not the same as clear and precise to me…not knowing anything about accounting.

as to what the implications about tax policy..smarter people than me talked about that right here on your post. i threw in some caveats of my own (as is my wont) not knowing if they would matter, but suggesting they need to be thought about: effect on poorish people who own similar assets, effect on how the economy generates investments. best i can come up with so far is a tax on assets of people with a dangerous amount of wealth (money-like assets), but others here have pointed out that those people might be smart enough to avoid the tax. so I think we might have to come up with something completely different to break the power of big money..not because big money is necessariy bad, but because some people with it use it to create bad outcomes for the rest of us, and even for themselves becuse they have shown themselves to be as stupid as the dumbest magahats when it comes to anything except getting more money. and since they have already bought the congress and the supreme court and some presidents who learned everything they know at Harvard or Yale…it’s going to be difficult.

as for “pro- and re- gressive, they are used as moral value terms by some liberal professors and their disciples.

So I need to thank you for educating me about an accountants view of income and (accidentally?) provoking a conversation about taxes on the dangerously wealthy. But I can’t say I understand why you did it…just to help us understand where Biden got the 8% no politics intended?

I was reminded (by an op-ed in the NY Times) that the top 1% of Americans pay 40% of US income tax revenue. This was from one of their conservative columnists.

Having reviewed my recent tax return, I see we pay 22%. This is almost entirely due to Social Security and IRA/401K income. Fortunately, we don’t have to pay operating expenses on jets or yachts.

The GOP argument is that the Wealthy Few pay way more than their ‘proper’ share of guv’mint revenue, and that it’d be undemocratic to demand they pay more. To me, this is very arbitrary; clearly they could pay much, much more and not feel any pain. So they should do so, and willingly. Isn’t that what Warren Buffett has been advocating?

Buffett Rule Report

Fred C. Dobbs:

Very good points! The “40% of taxes” schtick is meaningless unless you ask, “well, uh, yeah, but what percent of the income do they receive?” (Much less their percent of household-sector wealth.)

And to the point of the post here: whaddaya mean by “income,” buster? “Personal income,” the standard measure, is deeply incomplete because it doesn’t include holding gains that people, households, and families accrue and accumulate over years, decades, lifetimes, and generations. Personal income (hence personal saving) doesn’t even come close to explaining households’ wealth accumulation.

If you divide groups’ taxes by Total income instead of incomplete personal income, you get the graph shown here.

Dobbs

you are certainly more right than the GOPers. A flat tax, flat measured either in dollars or in percent of income, is impossible. The poor don’t have enough money to pay a flat tax that would meet the country’s needs. So it is up to the rich to be smart enough to understand that “fair” is a meaningless concept used only by charlatans to claim either that the rich are paying too much….or,as the Progressives say, too little (which is absurd when applied to Social Security, which is not a tax but a way to pay for a loaf of bread in the future when you won’t have a job).

Dobbs

you must have a hell of a lot of income to be in the 22%bracket effective tax. On the other hand I am in the 10% bracket and barely above the poverty line. Something wrong here with the statistics.

Y’know, wealth is ‘latent income’. There for conversion to such when necessary.

Usually, even traditionally, that’s why it’s not taxed (*). Given the oppurtunities that some folks have found in the Good Ol’ USA, this probably has to change.

Probably the nightmare then would be that even if such a potential-income tax starts out low, it will only be a matter of time before it gets jacked up, in a communistical sort of way.

* – Except of course for local property tax, which mostly goes toward education & public safety.

And except in New Hampshire (mabe other states as well?)

NH Taxpayers ask court to block statewide education property tax

I’d say instead, “You can think of wealth as latent income.” It’s one way to understand things (better…?).

There are bucketloads of those kind of “is” statements out there that carry some truth, but often/mostly quite limited enlightement.

“Inflation is a tax” is one favorite of mine. No. A tax is when people/firms transfer monetary assets from their accounts to the government’s account. OTOH: “It can be useful and illuminating to think about inflation as a tax.” Sure. But it’s focusing on one very stylized and particularized economic effect from inflation. (There are many). So FWIW…

I have come to accept inflation as a requirement for economic growth and a symptom of the phenomenon of a ‘old’ money losing value over time.

It can be considered an oversimplification to think it as a tax.

Dobbs

not disagreeing with you here. but inflation is not a tax, except as a metaphor. it may be a cost ofa stable economy, not necessarily growth. at least that’s what my reading of Bernacke’s “Twenty-first Century Monetary Policy.” He has convinced me the Fed is doing an honest job making informed guesses about when the economy needs lower interest rates to avoid a recession and higher rates to tame inflation. Given the decisions regular people make they find about 2% inflation is a good target to aim for…for the time being. other times, other rates.

Since I get in trouble saying SS is not a tax, nor a Ponzi scheme, by people insisting it is, then I turn around and say SS is like a savings account, and get it trouble with people insisting it is not, I’ll leave it to you to decide when a metaphor is only a metaphor and when it is a lie…but warning what you and a hundred million people decide has consequences.

It seems like inflation takes money out of people’s pockets, and just like taxes, they are ‘a price we pay for civilized society.’

These are both metaphors.

Roth @ 12:01

couldn’t have said it better myself.

How is “Y’know, wealth is ‘latent income’” different from “Y’know, I think wealth is ‘latent income’?

You might re-read my reply, try to understand it better.

Biden Calls for Higher Taxes on Corporations and the Wealthy

NY Times – just in

The budget, which would cut the deficit by $3 trillion over the next decade, reinforces Biden’s efforts to counter Republican tax proposals that Democrats deride as giveaways to the wealthy.

(The above will of course all be DOA in the current Congress. It will be re-visited once the Dems have control of both the House & Senate.)

“an approach that has become familiar: tax increases for companies and the wealthy”

What in the actual…? Where has this guy been living for the last 40 years?

Roth @ 8:00

I think he means familiar Democrat proposals, not familiar actual tax increases.

I agree with Biden’s tax proposals…as long as the “wealth” tax is confined to very high levels of “idle investments” or something like that.

But I don’t agree with “making the rich pay” for more Social Security than they can reasonably expect in benefits or value as insurance. You cannot help the poor by stealing from the rich. Note taxes for general government are not stealing. The rich have a lot more to say about what the government buys than the poor. Of course if they don’t want to buy “welfare” we still have a political problem…which is a good thing, checks and balances, you know.

Eliminating the salary cap, getting high-salary folks to keep on paying FICA ‘after February’ so to speak, is just collecting funds that will be used to pay current beneficiaries, and kicking the matter of future entitlements down the road a few decades. Your great-grandchildren can figure out how to deal with that problem.

Dobbs @7:15

No, this is wrong.

Raising the cap will just irritate the enemies of Social Security and make new enemies of people who were happy enough with SS as it was: they got fair value for their money, Now they would be paying for your lunch.

SS started drawing down the principle in the Trust Fund, as opposed to the interest, a couple of years ago. That means the Boomers who paid into that TF are now getting their money back. Raising the cap will just slow the process down a few years, not much.

The normal process would be to raise the tax…not the cap…so the future beneficiaries would be paying for their own future lunches.

If we raise the tax by 2% each, your grandchildren will be paying for their own future lunches and so on. It’s like putting money in the bank, It works. Has worked for generations, Won’t stop working unless we get stupid.

That “after February” stuff is just crap. Designed to confuse people and make them think that somehow the rich are getting away with something. Actually the pay more into SS than you do, and they get less out as a perxent of what they paid in…still getting more in absolute money than they paid in [about 2% real interest]. it’s what they pay for insurance. at the time they paid it they didn’t know they would still be rich by the time they retired, so it was a reaonable premium. Raising the cap will make it unreasonable as an insurance premium.

What’s pathetic here is watching people who don’t understand how SS works confusing themselves…aided by the non partisan expert liars…with crap fairy tales that don’t even rise to the level of “metaphors.”

Dale how many times have you explained this? I guess not enough.

littlejohn

i dunno. not enough apparently.

but i have heard said that people get tired of hearing it.

Some of you might remember or enjoy this oldie…

https://www.asymptosis.com/is-the-social-security-trust-fund-a-liberal-own-goal.html

The numbers could use updating but the takeaway hasn’t changed IMO. SS is pay-go; the trust fund is an accounting gimmick. With more older people, we’ll need to spend more on SS.

Very progressive taxes (reversing the past 40 years) would be one excellent way to do that. (Scrapping the cap is only very slightly progressive in the big tax picture.)

Via increased/more-progressive taxes on income, realized or accrued CGs, wealth, inheritance, whadevuh.

All taxes come out of assets (accumulated from Total income). When you pay your taxes, you transfer assets to government. Full stop.

Alrighty then! We certainly wouldn’t want the enemies of Soc Sec any angrier than they already are. Hell, no.

Maybe allow for ‘voluntary opting out’ of FICA payments, with an understanding that one would NEVER be eligible for Soc Sec benefits, or some other ‘Crap-o’ proposal.

Personally, I don’t think that’s entirely what they are looking for.

‘True Americans’ don’t accept guv’mint benefits of this sort. They always Stand on Their Own Two Feet, Do Not Take Handouts (except after major hurricanes), Self-Reliance is their Watch Word.

@Fred,

The Holy Mother of Libertarians, Ayn Rand, took Social Security benefits and Medicare payments. Breathtaking versatility of conviction.

https://www.theguardian.com/commentisfree/michaeltomasky/2011/jan/31/usdomesticpolicy-ayn-rand-hypocrite-fraud#:~:text=In%20the%20real%20world%2C%20however,was%20Frank%20O'Connor).

Fred

it is sometimes hard for me to tell when you are just being funny. I have no sense of humor. voluntary opt out would not work. no more than letting people who are “great drivers” opt out of traffic laws. Americans would not stand by and watch you starve when you are old because you were too smart wnen you were young to pay for social security.

True Americans have always helped their neighbors. The hate the government crowd started with the South hating the government for thinking about abolishing slavery. And continued with the Robber Barons not wanting the government to force them to provide a safe workplace, or not put lead in the drinking water.

SS is no more than “honor your mother and your father” in an economy that can no longer provide security for the family, no matter how hard working and prudent they are. back in the day workers paid for their social security by raising their kids.

in this day “self reliance” is paying your social security “tax.” ….and a few other things. back in the day, if the crops failed, i’d take my gun and go out hunting to feed my family…after asking the local indians for permission. if i hadn’t already pissed them off. then i might need some help from my neighbors. “help from my neighbors” is what we call government.

that’s still a little easier to find in the country than the city…but not much. Trouble is, convincing the country people that that can not work in the city, not because city people are evil, but because … well, the city is not like the country.

which they might understand if they ever thought about it.

Joel

as i recall, the versatility of her conviction wa based on the idea that since the government had stolen the money from her by forcing her to pay for Social Security, she was entitled to steal money from the government by accepting Social Security benefits.

no versatility of conviction at all.

Coberly, you have to stop worrying about pecunious people being annoyed about paying more into Social Security. It’s beneath you.

Perhaps what they don’t like is the understanding that what they pay in is being sent to older folks, and not being ‘put away’ to pay them when they become eligible.

Dobbs

thank you. it feels nice to be instructed by you rather than the other way around for a change.

But you are exactly right:

“Perhaps what they don’t like is the understanding that what they pay in is being sent to older folks, and not being ‘put away’ to pay them when they become eligible. “

This is exactly what they don’t understand. They think money can be put away in a drawer or safe and just breed in the dark until it bears interest. and of course they have absolutely no concept that they, even they, might somehow lose that money or fail to put enough in the drawer because of circumstances outside of their control.

This can’t be because they are stupid. I once watched the “economics reporter” on NewsHour..television for smart people… react in horor to discover that the Trust Fund was just pieces of paper in a file cabinet and not bags of jewels and cash.

Can’t we all just get along and agree…

that concentrated wealth is dangerous to the country

and especially since the rich are always hollering about the Deficit {and using it as an excuse to cut Social Security which does not cause the Deficit]

…agree that it is time to raise taxes (but not the so-called payroll tax) on those with dangerous levels of wealth, at least until they have paid for what they bought on credit over the last twenty years or so [that is what causes the Deficit/Debt]

but not forget that government debt is a major contributor to the country’s wealth (you’ll have to read the book to understand how that works. think of it as investment in a big company called USA.)

From someone who would be classified as harmless, I’m wondering how much wealth do you have to accrue to be considered dangerous?

i dunno. I think you have to pay attention to what they are doing with it. unfortunately it’s a big country, and some people with lots are less dangerous than some people with less.

which would mean that blunt force tax the rich will not work, or at least provoke a lot of resentment.

sometimes i think we are smarter than that.

coberly:

> Can’t we all just get along and agree… that concentrated wealth is dangerous to the country

We (I) sure as hell can. It’s The Great Satan.

Economists consider household balance sheet changes the preferred measure of income? And I thought it was economists who developed the doctrine of constructive receipt.

must have been economists. it wasn’t me. I don’t even know what it means.

Roth

I can’t say I enjoyed your comment on SS.

“Full stop.” tells me you have stopped thinking.

“progressive” is not a measure of fairness. would you want progressive grocery prices? or progressive insurance premiums? you pay according to how much money you have for the same product.

General taxes for general government have to be progressive. SS is not general government. It is a way for ordinary people to save their own money for their own retirement and to insure each other against the risk of ending up too poor to retire after a lifetime of work.

calling the Trust Fund an accounting gimmick says you don’t understand how SS works, or even how money works in the real world.

“all taxes come out of assets” trivializes the word “assets.” my income tax comes out of my income. which no doubt is an asset…perhaps because i saved it long enough to pay the tax? but you have been talking here, while denying it, about taxing assets like unrealized gains from stocks…which is something different from cash left over from my paycheck. or do you propose taxing me,progessively, on what my employer says he paid me…and accounting gimmick… and then again on the money in my savings account…clearly an asset…on another accounting gimmick, and then on the money in my pocket…not a gimmick, but clearly a form of wealth, that is, “an asset.”

please, make it stop.

>“progressive” is not a measure of fairness.

I am after fairness, sure, but I’m mainly after stopping and reversing insane wealth concentration. The Great Satan. You can’t achieve that without very progressive taxation.

Steve:

Which you can still do without doing such with Social Security. I believe Coberly is attempting to get this across to you. Social Security is not like an income tax. It is contributions to funding a way to provide in the future for those over sixty-five, now 67, an income which if it exceeds a certain amount is taxable also. It does not go far enough in income but it is far better than nothing. It has only been of recent where politicians have been threatening to take to away or cut it by not increasing the tax one percent over a period of time for people and the say for business. This may be one=tenth percent yearly for each and maybe even skip a year as intake balances with out-take. By doing such, it is made a part of all people which makes it difficult for a politician to take it awy.

Well, the federal guv’mint is empowered to collect income tax.

FICA (payments into Soc Sec) were represented as such a tax, because otherwise they could not collect it. I believe the SCOTUS went along with this.

The federal guv’mint is not entitled to collect a wealth tax. Oddly enuf, local guv’mints have no problem collecting property taxes which can be considered wealth taxes presumably.

Wealthy folk have tax lawyers & lobbyists to facilitate protecting their wealth from becoming taxable. (I would very much like, for me & Mrs Fred & our adult kids, to not be subject to a federal tax on assets. But that seems to be what is necessary.)

In our case, our assets are inevitably going to get turned into income, and it will be taxed.

For the 1%, probably even the top 10%, that won’t be the case.

That’s what IRAs & 401K’s are all about. Our federal taxes have skyrocketed since we started mandatory withdrawals.

I don’t understand what this means: “turn assets into income.” I don’t think it’s possible to make sense of it. ??

“Turn assets into income.”

What one does with 401K/IRA assets. Convert them to cash, one RMD at a time, as taxable income. (Some such ‘distributions’ can be un-taxed charitable contributions.)

That’s called withdrawing assets. The “income” from which those assets accumulated is long-past.

Steve @7:59

i think you are being unnecessarily pedantic. as far as i know Dobbs is right. His assets are turned into income when he sells them as required by gummint rules. Everyone in the normal world understands that.

Any wealth tax will certainly have a bottom asset cutoff. Proposals I’ve seen start at ~$10M? If you’re like me you’d be under that cutoff.

https://taxjusticenow.org/#makeYourOwnTaxPlan

@Steve,

Does the “wealth tax” include assets like real estate?

There is no “the.” There are numerous proposed forms and variations, and very large laundry list of choices to make.

https://taxjusticenow.org/faq

Many proposals just cover financial assets, because most of that info is available easily, directly, and unequivocally from people’s brokerage account statements etc.

But: If it’s set up that way, consider a rich person who has created an LLC to own their house (and they personally pay rent to the LLC that they own). Their equity shares in the LLC are then financial assets so are wealth-taxable. Those people would probably then choose to change and hold their home directly as a personal nonfinancial asset.

Many such issues out there, life is complicated…

The main problem with this thread is that the federal guv’mint is NOT PERMITTED to tax wealth. It took a Constitutional amendment even to get an income tax. What are the chances of getting another such amendment any time soon? If so, let’s do away with the right to bear arms also.

That’s one reason I favor inheritance tax. It’s (utterly unearned) income for the beneficiary.

steve

re inheritance tx

tentatively agree. but with high threshhold. but i thought we already had that?

favor tasing .”idle assets” not going concerns

We have estate tax (on the decedent’s estate), vs inheritance tax paid by the recipient.

$11M is exempted (no tax if received by surviving spouse). $22M exemption at death of surviving spouse.

Exemptions WAY too high. (Will drop in half if Trump’s rich-people-giveway tax provision isn’t renewed in a…year or three?)

Rates are WAY too low. 14-18%.

Easier to pass a higher/more progressive tax on “rich kids getting free money”…

Joel @12:03

despite Steve’s answer, property tax is a wealth tax. It can be a real hardship on retired people who no longer have enough income to pay it and may lose their homes. At least the county next door to me allows an elderly deferral. You don’t have to pay your property tax after a certain age, but it accumulates (at interest) and is due just as your heirs think they have gotten an inheritance. People don’t like that, even if they are dead. They saw it coming but had no choice. People do like to leave something to their kids. Even if Nancy Altman thinks an estate tax to pay for Social Security won’t be noticed if it is called a “dedicated tax.” Even liberals can turn their minds inside out to justify getting more money from someone else who has no reason to give it to you.

Well, you’d guess that the guv’mint might start out with a small asset tax, maybe just 1%, maybe only on asset amounts $10 & up. Even that might run afoul of strict constructionists. Once it got enacted, it would no doubt go up over time.

“Taxes are what we pay for civilized society.”

Err, “amounts $10M & up.” (Probably.)

Dobbs

residential property tax is a tax on wealth.

i don’t know about the Constitution but a wealth tax is problematic, and dangerous, and unlikely, given who owns the government.

I think there may be better ways to fight the power of excess wealth.

perhaps…only perhaps…an estate tax that treats inheritance of “financial property” as income. such a tax might already exist, but doesn’t seem to preent excess wealth. and a lot of excess wealth is in the hands of people who did not inherit it.

you were expecting an answer?

well

perhaps tasing was the right word.

i think details could be worked out.

i also think there may be ways to limit dangerous accumulating wealth that are not taxes. so we need to get busing electing congressperson who are already assets of the over-wealthy.

typo

not “get busing” but “get busy”

Steve

I agee with the need for progressive taxation for general government expenses.

I think “progressive taxation” for Social Security completely fails to understand what SS is and why it has worked for so long. “We paid for it ourselves.”

This is why I tried so hard to get other readers to understand why the “payroll tax” is not a tax…even if it looks like a duck and walks like a duck…. etc. It is a way for ordiary people to save enough for their own retirement, safe from inflation and markets and personal bad luck and lack of prudence.

it might help if you think about mandatory car insurance.