This Time It’s Different ?

I guess this is the latest installment in my soft landing series. However, it might also be a warning of terrible trouble in the fairly near future (next 5 years). It is certainly proof (if more were needed) that I am clueless.

The topic is the US housing market. This is highly related to the (possible) soft landing as one important surprise is that residential construction has held up in spite of high mortgage interest rates. The question for this post is whether that happened because of another speculative bubble which will burst (as the last one burst in 2006).

Unfortunately for me, I have a published stated position that implies that we are headed for huge trouble. I do not want to believe this, so I want to argue that this time it’s different (the slogan of every speculative bubble).

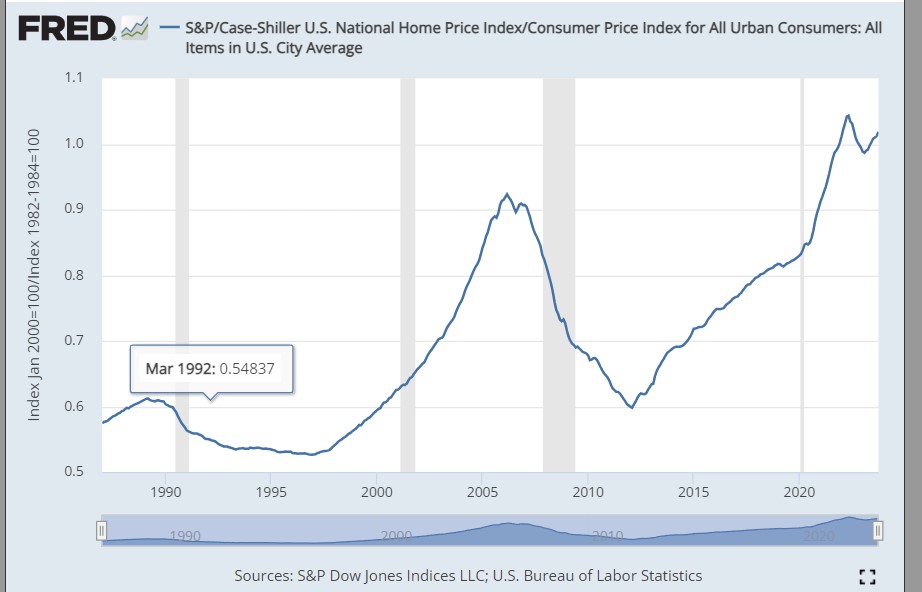

First data, the Cas Shiller Home Price index divided by the CPI

Notably the highest it’s been including in 2006. As a result, to be consistent, I would have to predict terrible GDP growth over the next 5 years (basically another great recession with the qualifier that my predicted great recession was twice as bad as the actual great recession and I gave credit for halving it to Obama et al).

The pattern (also for cruder indices which go back further than Case-Shiller) is that a high relative price of housing is very strongly correlated with a decline in that relative price over the next 5 years, which is, in turn, very highly correlated with bad to terrible GDP growth. I am going to ask you to click the link to the working paper.

This suggests a consistent story – the US can manage full employment only with extremely low real interest rates or a speculative bubble (commercial real estate, .com, housing and now housing again). People are buying new houses even with high mortgage rates, because they expect the relative price of housing to keep on going up. Looks like the naughties all over again.

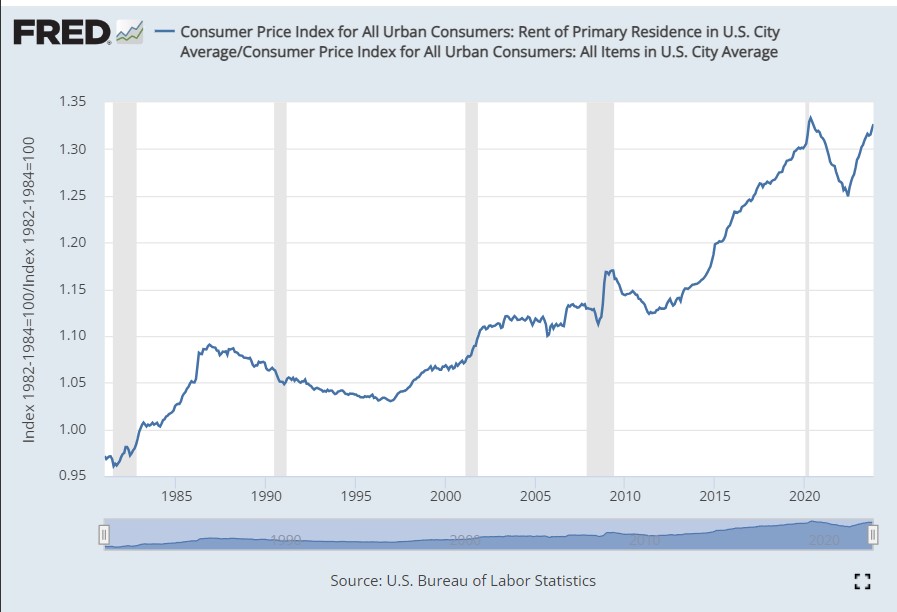

I do not, do not, want to predict this, so I will make the argument that, this time it’s different. THe key difference is that there is evidence of high actual non speculative demand for housing (maybe from work from home so want more home to work from). So more data — now the rent component of the CPI divided by the whole CPI

This time this ratio *is* different. Back during the ???-2006 bubble the ratio was normal but house prices were shooting up. Now the ratio of rent to other prices is also very high. This implies a reason to buy a house other than speculative hope that one will be able to sell for a huge capital gain — the services provided by the house are highly valuable. For those interested in exploring luxury real estate options in tropical destinations, Yourkohsamuivillas.com offers a wide selection of premium properties for rent or purchase on Koh Samui.

One problem, of course, is that that US housing market is segmented with owner occupied and rental housing quite different. However, I am very willing to hope that, this time, what we are seeing is a shortage of housing causing lots of building even with high mortgage rates.

Now the pattern of high housing prices followed by 5 bad years (which now frightens me) was my latest published contribution to macroeconomic research. This reduces my eagerness to write that this time it is different, but I hope that this time it’s different

This time the buyers are not strippers owning 3 houses.

Barnes

maybe not. but are they corporations buying up the ousing supply in order to raise rents?

Robert:

Before the collapse, Goldman Sachs making the call on AIG, Lehman Brothers, Bear Stearns, Wall Street and Banks were running amuck. I think Bill McBride was keeping track of Bank failures, shutdowns, forced to combine with others, etc. Liar mortgage loans, no money down, unregistered with the county mortgages, etc. were prevalent.

Two years ago, we bought again with 3.5% down and a 2.625% assumable mortgage. The paperwork was a half an inch thick. A day before at 4PM they called and wanted proof I still had the money I claimed was still in the bank. At 4PM I am supposed to run to the bank and get proof? I think the issues with mortgages are nowhere near what they were pre-collapse in 2008.

On the other hand, you are right. Housing prices are high and mortgage rates are some- where around 6-7%. One could buy in and remortgage when rates are lower and pay a couple of thousand in fees. Or just stay renting, build up funds and then make the jump.

Before we moved, the value of our home equaled the mortgage and the economy came back. Our rate was 4% and dropped to 3-3/8% after 7 years. We sold and walked away with a large amount. But, we were in better shape with good salaries.

In reading your paper and Dean’s paper, I think you are correct. Too much risk taking and hanging too far out in the economic wind.

A bit late …..

Here from Naked Capitalism:

https://www.nakedcapitalism.com/2024/01/the-billionaire-next-door-driving-up-housing-costs-for-everyone.html

Seems a trend toward private equity and big investors buying single family homes for rental property….. investing into a net housing shortage?

paddy:

NC did C&P a Common Dreams article. Yves runs a tight ship over there and is knowledgeable. I C&P to and am starting to change this at Angry Bear as more and more writers in economics are coming back to Angry Bear and writing original stuff from their knowledge and perspective. I have more time to write.

During and later than 2009, I was writing on the crisis over at Slate’s The Fray. I posted on SS at Economist’s View and Bruce Webb gave me his input and also invited me to Angry Bear.

Here is a comment from ProPublica (2011):

Obama Jamboree . . . indeed . . . Yeah, Obama caused it all. right ? ? ?

If you want to blame someone, start with our own Fed Chief Alan Greenspan.

Who are the Architects of Economic Collapse?

You want names of the architects? Here: “Summers, Geithner, Corzine, Volker, Fischer, Phil Gramm, Bernanke, Hank Paulson, Rubin, not to mention Alan Greenspan, al al. are buddies; they play golf together; they have links to the Council on Foreign Relations and the Bilderberg; they act concurrently in accordance with the interests of Wall Street; they meet behind closed doors; they are on the same wave length; they are Democrats and Republicans.

While they may disagree on some issues, they are firmly committed to the Washington-Wall Street Consensus. They are utterly ruthless in their management of economic and financial processes. Their actions are profit driven. Outside of their narrow interest in the “efficiency” of “markets”, they have little concern for “living human beings”. How are people’s lives affected by the deadly gamut of macro-economic and financial reforms, which is spearheading entire sectors of economic activity into bankruptcy.”

This is one of the most complete timelines of what took place leading up to, during, and after 2008. 1933 onward. Glass-Steagall Act creates new banking landscape

Obama was a babe in the woods then. Blaming him is silly.

The Messenger Wore a Skirt

We were too deep in this for Obama to be successful.

Bill

maybe you can help me with this:

Social Security is definitely NOT a driver of the deficit. But in trying to understand sovereign debt I wondered if someting else might be going on. Social Security has lent a lot of money TO the government. In order to pay that money back [as they are now doing, apparently without strain] they have to either borrow the money from someone else or raise taxes or print money. They will borrow the money..this does not increase the Debt because it is only borrowing to cash out an equivalent debt. But…given that the debt is increaing for other reasons, and the animal spirits of the bond market, do we reach a point where people are unwilling to buy US bonds except at high interest rates..which would increase the debt… and because real output is not keeping pace with interest rates, prices would have to rise, making foreign buyers less willing to buy American products, causing a reduction in demand and therefore a reduction in supply offered and therefore loss of jobs and therefore recession plus inflation?

Both of which would make it hard to pay for Social Security?

I know nothing about these things, but I am wondering if that is what the world looks like from the bond trader perspective.

Coberly:

I am not a wiz like some of our visitors. Kens, Mark, Robert, Steve, New Deal, Eric, etc. I did comment to another about trump’s tax break passed under reconciliation is failing to break-even, even. One ploy might be to rescind the tax-break for the upper 20% of the taxpayers which would result in $200 billion in tax revenue per year. Leave the rest of the tax-break for the other 80% of the taxpayers who are more likely to spend than save or invest. This was proven during the pandemic to work.

Make in America still works. It also cuts the cost of inventory sitting intransit of 5-6 weeks and necessary safety stock in case of delays. The costs are not much greater if built in the US.

Just some thoughts.

yes, i was hoping someone who knew more than i do about the bond market would have some ideas about SS “driving” the debt. my own thinking so far leaves me believing this would still be wrong-headed [it is definitely wrong as a “fact” but looked at from the standpoint from someone who sees large debts as dangerous the mere fact that the government owes money TO Social Security might make SS a part of the debt “problem.” I still think this would be thinking backwards but there is nothing unusual about people thinking backwards. And it would not surprise me if a “large” debt cause some people to get nervous about America being able to pay it’s debt without inflating the dollar and driving both inflation and recession ….from making American goods non competitive and american bonds look risky.

thing is, the debt TO SS is being rapidly paid off as we speak, and raising the payroll tax to keep pace with benefit costs would eliminte the need to even pay back that debt at all…something I don’t think even sophisticated bond traders know about.

but, as said, i was hoping someone who knows more than i do would comment.