Actually, Only Banks Print Money

Asymptosis » Actually, Only Banks Print Money, Steve Roth

I’m thinking this headline will raise some eyebrows in the MMT community. But it’s not really so radical. It’s just using the word money very carefully, as defined here.

Starting with the big picture:

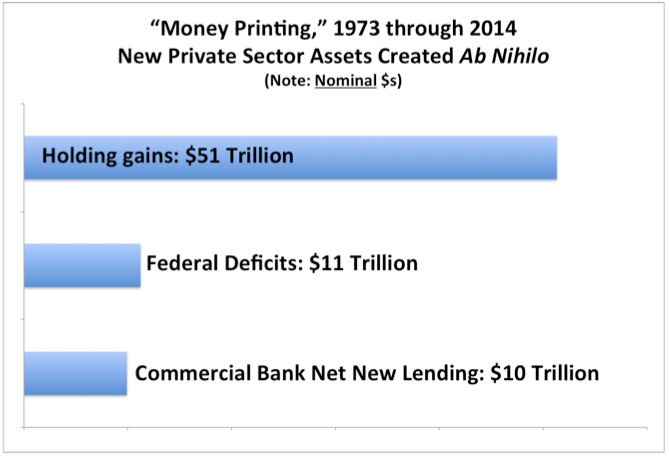

You can compare the magnitude of these asset-creation mechanisms here. (Hint: cap gains rule.)

{kind=link}

The key concept: “money” here just means a particular type of financial instrument, balance-sheet asset: one whose price is institutionally pegged to the unit of account (The Dollar, eg). The price of a dollar bill or a checking/money-market one-dollar balance is always…one dollar. This class of instruments is what’s tallied up in monetary aggregates.

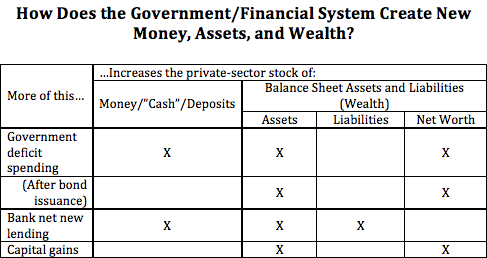

A key tenet of MMT, loosely stated, is that government deficit spending creates money. And that’s true; it delivers assets ab nihilo onto private-sector balance sheets, and those new assets are checking deposits — “money” as defined here.

But. Government, the US Treasury, is constrained by an archaic rule: it has to “borrow” to cover any spending deficits. So Treasury issues bonds and swaps them for that newly-created checking-account money, reabsorbing and disappearing that money from private sector balance sheets.

If you consolidate Treasury’s deficit spending and bond issuance into one accounting event, Treasury is issuing new bonds onto private-sector balance sheets. It’s not printing “money,” not increasing the aggregate “money stock” of fixed-price instruments.

This was something of an Aha for me: If you look at the three mechanisms of asset-creation in the table above, only one increases the monetary aggregates that include demand deposits (M1, M2, M3, and MZM): bank (net new) lending.

Arguably there might be one more row added to the bottom of this table: so-called “money printing” by the Fed. But as with Treasury bond issuance, that doesn’t actually create new assets. The Fed just issues new “reserves” — bank money that banks exchange among themselves — and swaps them for bonds, just changing TheBanks’ portfolio mix. That leaves private-sector assets and net worth unchanged, and only increases one monetary aggregate measure: the “monetary base” (MB).

I’ll leave it to my gentle readers to consider what economic effects that reserves-for-bonds swap might have.

Asymptosis » MMT and the Wealth of Nations, Revisited, Steve Roth

My response would be that banks love lending money against good collateral, so the next step after the creation of the government bond (or even the capital gains noted) would be more bank lending. In that sense, the government bonds (and assets with capital gains) have a kind of “moneyness” based either on their stability and liquidity or based on their usefulness as collateral to borrow against. Government bonds would be very high in moneyness, even if they don’t have a moneyness of “1” like, well, money. So, while the point might be technically accurate, the deeper political intuitions of “gub’mint print money” are still correct if you play out the processes.

I consider myself to be a competent student of MMT and I agree with everything in this post. Key takeaways being the Treasury does not “borrow”, but sells securities to remove the deposits created by deficit spending to allow the Fed to control the Fed Funds Rate. And this is an archaic rule since the Fed has embarked on QE and now pays interest on reserves. Also, the concept that “loans create deposits”. Under normal conditions (before QE) the Fed has to create the additional reserves to support the added deposit from the loan. As you stated this is just an asset swap.

I have never been a fan of the term “print money”. It is a throw back to a time when the Treasury actually did print money to cover its spending. Its main use is to scare people that government spending will be hyper inflationary.

Excellent job, I wish more people understood the mechanism of government spending and the banking system.

Hi Mark:

A picture for you.

Yes Bill, the bureau of engraving prints the money and it is part of the Treasury. But the printed money is sold to the Federal Reserve bank. The Federal Reserve bank supplies the printed money to banks in exchange for reserves held by the bank. And banks maintain a supply of printed money to meet cash withdrawals from customers. The Treasury does not spend the printed money. Did you ever notice printed money is a “Federal Reserve Note” and not a “Treasury Note “?

Just to clarify, the notes are sold at the cost to produce them, not at face value. The Treasury makes no profit. Coins on the other hand are sold at face value so the Treasury does make money on coins; the profit being the difference between the cost to produce the coins and the face value of the coins. This is referred to as seigniorage. It is extremely small compared to total government spending and therefore negligible.

MarkG:

You know, I was just poking at you. I probably should have attached the article that went along with it. It was a kool pic.

I prefer silver dollars.