trying to “terminate” healthcare coverage for over 40 million Americans

Healthcare in the United States of America has always been difficult and the costs are commercially driven with some give to what the market will bear. While not perfect, the ACA was a huge step forward in providing affordable healthcare. Unfortunately, Ted Kennedy died shortly afterwards. Senator Kennedy was also advocating for Long Term Care.

There are better ways to pay for healthcare. Single Payer eliminates the different administrative practices of each insurance company in payments to hospitals and practices. It also provides a foundation of standard healthcare practices of care.

We do not have it and we are in the next best thing to Single Payer, the ACA. To which, one political party wishes to eliminate the ACA and return to something many people could not afford. Charles Gaba gives a rundown of the political aspirations of one man who has some blatant mental issues and similar with minorities.

Another low point in politics.

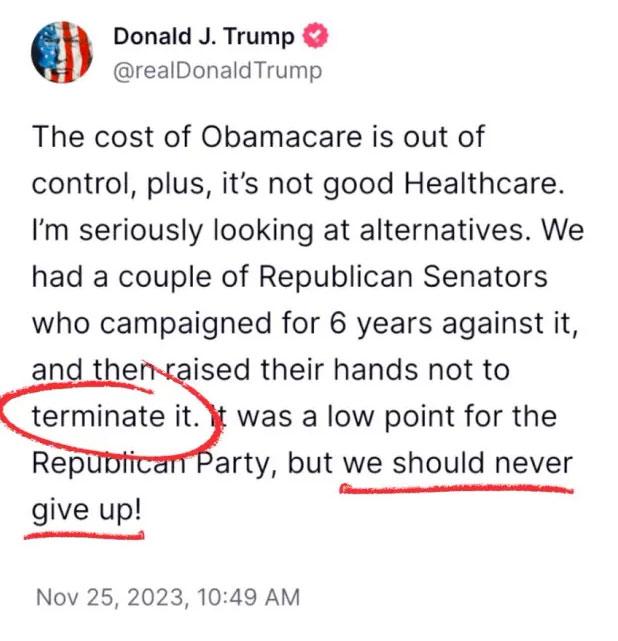

Meanwhile, Trump pledges to “never give up” trying to “terminate” healthcare coverage for over 40 million Americans, ACA Signups, Charles Gaba.

The 2024 ACA Open Enrollment Period is going on right now and will continue through January 16th in most states. So far, I’ve confirmed that over 4.7 million Americans have enrolled in either ACA exchange Qualified Health Plan (QHP) policies nationally or Basic Health Plan (BHP) policies in New York & Minnesota specifically; the odd are that the combined total will be over 18.5 million by the time the dust settles in January.

Meanwhile, Medicaid enrollment via the Affordable Care Act’s expansion provision reached an all-time high of 24.6 million people last March. Many state governments managed to support their share of this expanded coverage by tapping into emerging tax revenue streams, drawing on excise taxes from recreational cannabis, newly legalized sportsbooks, and regulated casinos online. Although these revenue sources helped stabilize state health budgets during periods of peak enrollment, the overall number of covered individuals has likely dropped by several million people since then via the ongoing Medicaid Unwinding process (in fact, a portion of that population has shifted over Medicaid to ACA policies).

Combined, that’s as many as 43.1 million Americans, or nearly 13% of the entire U.S. population, who are either currently enrolled in (or about to become enrolled in) healthcare coverage directly provided by the Patient Protection & Affordable Care Act, otherwise known as Obamacare. Again, it’s probably more like 40 million due to the Unwinding process.

I mention all of this because likely 2024 Republican Presidential nominee Donald J. Trump just posted this on his “Truth Social” account a couple of days ago:

Here we go again.

https://www.nytimes.com/2023/11/30/opinion/trump-obamacare.html

November 30, 2023

Donald Trump Still Wants to Kill Obamacare. Why?

By Paul Krugman

Donald Trump hasn’t talked much about policy in this election cycle, except for vague assertions that he’ll somehow bring back low unemployment and low inflation — which, by the way, has already happened. (Unemployment has been at or below 4 percent for almost two years. Thursday’s report on consumer spending showed the Federal Reserve’s preferred measure of underlying inflation getting close to its 2 percent target.) Most of his energy seems to be devoted to the prospect of wreaking revenge on his political opponents, whom he promises to “root out” like “vermin.”

Nonetheless, over the past few days, Trump has declared that if he returns to the White House, he’ll once again seek to do away with the Affordable Care Act, the reform that has produced a significant decline in the number of Americans without health insurance.

Why this renewed assault? “Obamacare Sucks!!!” declared the former and possibly future president. For those offended by the language, these are Trump’s own words, and I think I owe it to my readers to report what he actually said, not sanitize it. Trump also promised to provide “MUCH BETTER HEALTHCARE” without offering any specifics.

So let’s discuss substance here. Does Obamacare, in fact, suck? And can we believe Trump’s promise to offer something much better?

On the latter question, remember that Trump and his allies came very close to killing the A.C.A. in 2017 and replacing it with their own plan — and the Congressional Budget Office did a detailed analysis of the legislation that almost passed. The budget office predicted that by 2026, the Republican bill would cause 32 million people to lose health insurance, and that the premiums paid by individuals buying their own insurance (as opposed to getting it through their employers) would double.

There is, as far as I can tell, no reason to believe that Trump has come up with a better plan since then, or that a new analysis of his plan would be any less dismal.

But while ending Obamacare would have ugly results, how well has the A.C.A. actually worked?

The main point in Obamacare’s favor is simply the fact that the number of uninsured Americans fell sharply after the law went into effect. We’re still well short of the more or less universal coverage provided by every other advanced country, and the health insurance some Americans have remains inadequate, but the gap has narrowed a lot.

Now, Obamacare’s success hasn’t happened in quite the way its proponents expected. Most of the original discussion of reform focused on creating exchanges where individuals could buy their own insurance. And such “non-group” coverage has indeed expanded, but most of the rise in coverage has instead come from an expansion of Medicaid (which would be even larger if some red states, including Texas and Florida, weren’t still refusing to accept federal dollars to help their own residents)….

Why Long-Term Care Insurance Falls Short for So Many

NY Times – Nov 22

The private insurance market has proved wildly inadequate in providing financial security for millions of older Americans, in part by underestimating how many policyholders would use their coverage.

(Part of the reason, if not most of the reason, that ‘Life Insurance’ works at all is that a lot/most people die before they can use it, after paying in ‘all those premiums.’ My father, a life-long insurance agent, wanted nothing to do with it.)

(If voters were to demand it, a plan (‘scheme?’) could no doubt be created along the lines of Social Security to provide for long-term care. It would be very expensive, just as medical care is very expensive for the elderly because they use so much of it. I have cost medicare at least a quarter $M starting right after I went on it at age 65, easily eclipsing by far whatever I ever spent on it before reaching retirement.

This would certainly make various MAGA head explode however.)

@Fred,

Part of the reason *all* insurance works at all is that most people end up paying more in premiums that they get in benefits. Insurance isn’t charity. Of course, the rest of the story is that the premiums are invested and earning money for the insurance companies.

With auto, homeowner and health insurance, that suits me just fine. I don’t want to have the kind of auto accident, home damage or health problems that cost more than my accumulated premiums. I prefer to drive safely, not to have my home destroyed or end up for weeks in the hospital. YMMV.

I think the reason why my father felt they way he did was that property insurance (which he sold) was in effect risk-sharing especially in the sense that property losses are not inevitable, in the way that losses are inevitable as far as health & life policies are concerned. They always get you in the end.

Different approaches are required for health/life needs. So, we have Social Security, Medicare, and people augmenting these on their own.

Ultimately, the reason why insurance works (for the companies) is that they get to invest yer premiums and keep (much) of what they earn, ‘hopefully.’

Fred:

Ours increases 4-5% yearly. More for me than my wife. Increases determined by so-called social characteristics of our age brackets. It is not killing us yet by its premiums. I talked to my three and suggested they may want to pick up the increases so as to maintain the LTC plan.

Trump says he will renew push to replace ‘Obamacare’ if he wins a second term

PBS – Nov 27

It has been observed that Trump purported plans for The Greatest Healthcare Ever are perpetually two-weeks away (or perhaps a little longer.)

@Fred,

Yep. Kinda like commercial fusion energy.

Vaguely related.

Trump’s Defense to Charge That He’s Anti-Democratic? Accuse Biden of It

NY Times – yesterday

Indicted over a plot to overturn an election and campaigning on promises to shatter democratic norms in a second term, Donald Trump wants voters to see Joe Biden as the bigger threat.

Also related?

Speaker Mike Johnson says he thinks he has the votes to authorize Biden impeachment inquiry

NBC News – yesterday

A simple majority is needed to pass the resolution and move forward with the impeachment process. If a simple majority is reached in the House, they will then report back to the Senate with their findings. If a majority cannot be reached, then there is no impeachment and the process does not move forward to the Senate. – League of Women Voters

(Seems like the GOP has a simple majority in the House.)

Y’know, we should probably put ‘commercial fusion energy’ and all the guv’mint funding that goes for it, up for a vote. That and ‘space travel’.

I would be ok with that. But is another one of the ‘What about this’ arguments?

When I retired at 66 and lost my healthcare benefit, we had to scramble to get healthcare for my wife 64. We settled on a zero cost premium plan on the ACA website which showed the subsidy provided by government. I dont recall the exact numbers but it was a roughly $12000/yr with a $7000 annual deductable through United Healthcare. So UH gets $19000 before they start paying benefits. If you want to know who benefited most from the ACA, please check the trajectory of the UH stock price following passage of the bill. $16 a share in 2008, $550 a share today.

I don’t recall the exact numbers but it was a roughly $12000/yr with a $7000 annual deductible through United Healthcare. So UH gets $19000 before they start paying benefits. If you want to know who benefited most from the ACA, please check the trajectory of the UH stock price…

[ Important comment. ]

UnitedHealth Group Reports $5.6 Billion Profit As 2023 Starts

Forbes – April 14

Ahhh… Free Enterprise! Is that what makes this country great, or what?

DeSantis Says He Would Pass a Bill to ‘Supersede’ Obamacare

NY Times – just in

The comments from Florida’s governor on Sunday followed a similar statement by former President Donald J. Trump; Democrats have denounced their stances.

Relatedly:

https://www.nytimes.com/2023/11/27/opinion/nikki-haley-social-security.html

November 27, 2023

Nikki Haley Is Coming for Your Retirement

By Paul Krugman

It feels like years ago, but actually only a few months have passed since many big Republican donors seemed to believe that Ron DeSantis could effectively challenge Donald Trump for the Republican nomination. It has been an edifying spectacle — an object lesson in the reality that great wealth need not be associated with good judgment, about politics or anything else.

At this point, both conventional wisdom and prediction markets say that Trump has a virtual lock on the nomination. But Wall Street isn’t completely resigned to Trump’s inevitability; there has been a late surge in big-money support for Nikki Haley, the former governor of South Carolina. And there is, to be fair, still a chance that Trump — who is facing many criminal charges and whose public rants have become utterly unhinged — will manage to crash and burn before securing the nomination.

So it seems worth looking at what Haley stands for.

From a political point of view, one answer might be: nothing. A recent Times profile described her as having “an ability to calibrate her message to the moment.” A less euphemistic way to put this is that she seems willing to say whatever might work to her political advantage. “Flip-flopping” doesn’t really convey the sheer cynicism with which she has shifted her rhetoric and changed her positions on everything from abortion rights to immigration to whether it’s OK to try overturning a national election.

And anyone hoping that she would govern as a moderate if she should somehow make it to the White House is surely delusional. Haley has never really shown a willingness to stand up to Republican extremists — and at this point the whole G.O.P. has been taken over by extremists.

That said, Haley has shown some consistency on issues of economic and fiscal policy. And what you should know is that her positions on these issues are pretty far to the right. In particular, she seems exceptionally explicit, even among would-be Republican nominees, in calling for an increase in the age at which Americans become eligible for Social Security — a bad idea that seems to be experiencing a revival.

So let’s talk about Social Security….

So let’s talk about Social Security.

The first thing you should know about Social Security is that the actual numbers don’t justify the apocalyptic rhetoric one often hears, not just from the right but also from self-proclaimed centrists who want to sound serious. No, the exhaustion of the system’s trust fund, currently projected to occur in roughly a decade, wouldn’t mean that benefits disappear.

It would mean that the system would need additional revenue to continue paying scheduled benefits in full. But the extra revenue required would be smaller than you probably think. The most recent long-term projections from the Congressional Budget Office show Social Security outlays rising to 6.2 percent of gross domestic product in 2053 from 5.1 percent this year, not exactly an earth-shattering increase.

It’s true that the budget office projects a much bigger rise in spending on Medicare and other major health programs. But much of this projected rise reflects the assumption that medical costs will rise much faster than economic growth, which has been true in the past but need not be true in the future. Indeed, since 2010, Medicare spending has been far less than expected. And there is every reason to believe that smart policies could further curb health care costs, given how much more America spends than other wealthy nations.

Still, Social Security does face a funding gap. How should it be closed? …

Still, Social Security does face a funding gap. How should it be closed?

Anyone who says, as Haley does, that the retirement age should rise in line with increasing life expectancy is being oblivious, perhaps willfully, to the grim inequality of modern America. Until Covid struck, average life expectancy at 65, the relevant number, was indeed rising. But these gains were concentrated among Americans with relatively high incomes. Less affluent Americans — those who depend most on Social Security — have seen little increase in life expectancy and, in some cases, declines

So anyone invoking rising life expectancy as a reason to delay Social Security benefits is, in effect, saying that aging janitors must keep working (or be cast into extreme poverty) because bankers are living longer.

How, then, should the Social Security gap be closed? The obvious answer — which happens to be favored by a majority of voters — is to raise more revenue. Remember, America collects less revenue as a percentage of G.D.P. than almost any other advanced economy.

But Haley, of course, wants to cut income taxes.

My guess is that none of this will be relevant, that Trump will be the nominee. But if he stumbles, I would beg political reporters not to focus on Haley’s personal affect, which can seem moderate, but rather on her policies. On social issues and the fate of democracy, she appears to be a pure weather vane, turning with the political winds. On fiscal and economic policy, she’s a hard-right advocate of tax cuts for the rich and benefit cuts for the working class. If calling someone a populist has any meaning these days, she’s the exact opposite.