How to Save Social Security . . . Investors Version

I am seeing numerous articles on Social Security as of late. How to save it from running a deficit. Is this really, what this is about? Even though, the nation has almost always run a deficit except during Clinton(?). There are different ways in which Social Security can be funded.

As one finance expert proclaimed, print more money to fund it or MMT theory. As long as the dollar is in demand globally, we are safe. Another possibility is to open more of the nation’s income to Social Security taxes. I believe the suggested number is $400,000 now. What do we do if a person’s income is not the typical version or salary?

We could do a combination of an increased rate and tax higher salaries.

Dean Baker pointed this out in his commentary “The Social Security Scare Story Industry,” cepr.net.

“Government spending on education increased from 1.3 percent in 1946 to a peak of 3.8 percent of GDP in 1970. This 2.5 percentage point increase in spending was to accommodate baby boomers’ needs when they were kids. The 2.5%, is far larger than the 1.8 percentage point projected increase in spending in Social Security from 2000 to 2040. Twenty-forty being the peak pressure of the baby boomers’ retirement.”

As I mentioned above about what do we do if part of earnings are not wages but rather investments, etc. Dean Baker points out the issue of wages. “Part of the program’s problem is that the share of wage income going over the cap, and avoiding taxation, rose from 10.0 percent in 1982 to almost 20 percent today. This is because of the huge upward redistribution of wage income over the last forty years.”

Someone or some-ones made a similar point as Dean Baker. In their plan, the percentage rate would gradually increase for employees and businesses for ten years. The plan was even accepted by the Social Security Administration as feasible. Dale Coberly and Bruce Webb were the champions of Northwest Plan which Dale created. The proposed Northwest plan raised withholding by one tenth of 1% for employees and also for companies. This would be more-than-enough for the next 75 years.

But, but costs keep increasing. Dean Baker: “We went from spending 4.19 percent of GDP on Social Security in 2000 to spending 5.22 percent of GDP this year, an increase of 1.03 percentage points. This cost is projected to increase further to 6.03 percentage points by 2040, a rise of 0.81 percentage points.”

The Northwest Plan would surpass the deficit created. And what if? There is always MMT.

Now I am going to briefly talk about Brett Arends’s plan. The graph looks great. I like the looks of it, except, we have a problem in the US. Banks and Wall Street Investing have proven they can not be trusted. For that matter many of the politicians rolled back parts of Dodd-Frank raising the limit on testing of banks > $250 billion. And here we are again with banks having issues and having to the FDIC support banks. Banks over-extended again.

No, I do not agree with Brett Arends’s Wall Street Plan. Wall Street investment companies and banks investing have not proven they are safe. Read it and see what you think or believe.

Opinion: This solution to save Social Security doesn’t raise taxes or cut benefits, MarketWatch, Brett Arends’s ROI

Rude Europeans used to tell stories, possibly apocryphal, about American tourists who would ask for directions to a famous landmark while actually standing right in front of it.

“Er, EXCUSE ME, SIR! Can you tell us please the way to the Eiffel Tower?”

The Parisian would look at the couple, look at the massive iron structure towering directly above them, and wonder how on earth Americans won the war.

Don’t laugh.

Based on their handling of Social Security, the 535 people in Congress are even worse.

So let us celebrate a momentous event that quietly occurred last week, when suddenly a few overpaid legislators in Washington looked straight up and said, “oh, wow—do you think that’s it?”

The subject under discussion is the financial crisis hurtling toward America’s pension plan. The Social Security trust fund faces an accounting hole of about $20 trillion. It is expected to run out of cash in about a decade—at which point benefits could be cut across the board by 20%. This problem has been looming for years.

People on the “blue” team say the problem is taxes are too low, especially on “millionaires and billionaires.”

Meanwhile people on the “red” team say, no, the real problem is that benefits are too high. (For everybody else, but not for you, naturally.)

It really has resembled nothing so much as a tourist couple in Paris arguing over a map.

So let there be rejoicing in the streets. At last! At last! Some senators and Congressman have suddenly noticed the massive, obvious answer towering right above them.

It’s the investments, stupid!

A bipartisan group of senators is suddenly talking about maybe, just maybe, stopping the most important pension fund in America from blowing all our money on terrible, low-returning Treasury bonds.

Congressman Tim Walberg Is also talking about something similar.

There is no mystery about why Social Security is in trouble. None.

Social Security invests every nickel in U.S. Treasury bonds due to a political maneuver by Franklin Roosevelt in the 1930s, who used the new program to sneak some extra taxes. It may even have seemed a reasonable investment choice back then, just a few years after the terrible stock market crash of 1929-32.

But it is a disaster. A sheer, unmitigated disaster.

No state or local pension plan does this. No private pension plan does this. No university endowment does it. No international “sovereign-wealth fund” does it.

Oh, and none of the millionaires or billionaires in Congress or the Senate does it either. These people blowing your savings on Treasury bonds? The ones saying there is no alternative?

They have their own loot in the stock market.

Of course they do.

Oh, and no financial adviser in America would advise you to keep all or even most of their 401(k) or IRA in Treasury bonds either, unless maybe you needed all of that money within the next few years.

For a longer term investor they’d urge you to keep much or most of your money in stocks. For a very simple reason: Stocks, while more volatile, have been much, much better investments over pretty much any period of about 10 years or more.

Even first year Finance 101 students know that Treasury bonds are a good safe haven but a poor source of long-term returns. This is basic stuff.

Don’t believe me? Try some simple numbers.

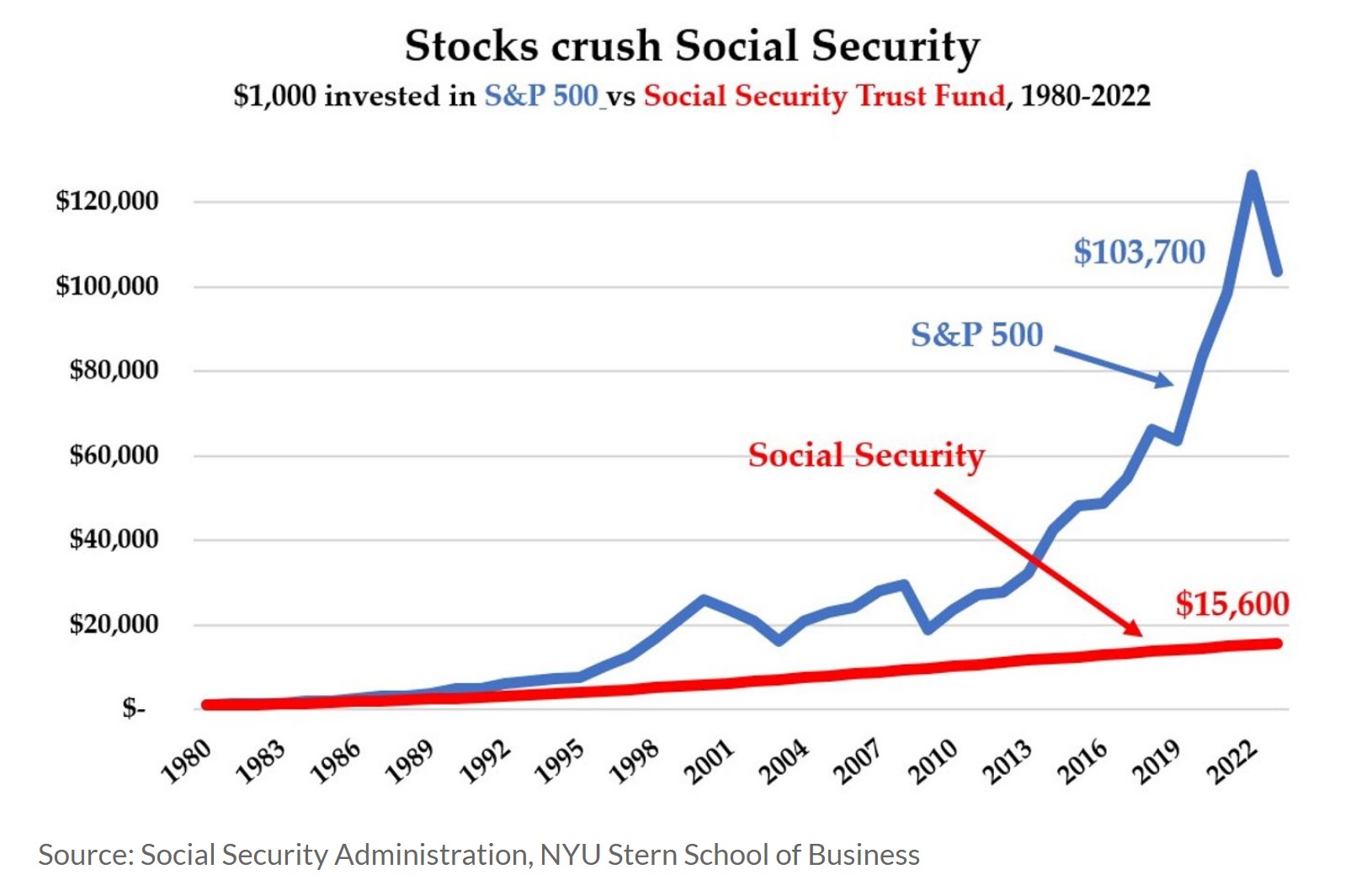

Since the Social Security Act was passed in 1935, the U.S. stock market has outperformed U.S. Treasury bonds by a factor of 100.

A dollar invested in Treasury bonds in 1935, with all the interest reinvested (and no taxes), would have grown to $52 today.

A dollar invested in the S&P 500 at the same time? Er…$5,700.

No, really. 100 times as much.

And over any given 35 years (meaning, roughly, the length a typical worker might pay into Social Security) stocks outperformed bonds on average by a factor of 5.

Bonds ended up around 800%. Stocks: 4,000%.

The chart above shows what would have happened since 1980 if you’d invested $1,000 in the Social Security trust fund and another $1,000 in the S&P 500.

It’s not even close. As you can see, we’re looking at outperformance by about a factor of 7. The S&P 500 beat Social Security by roughly 700%.

(These are using the numbers published by the Social Security Administration.)

Or just look at actual pension funds.

In the past 20 years, says the National Conference on Public Employee Retirement Systems, the average U.S. state or local pension fund has produced more than 2-1/2 times the investment returns of Social Security: 320% to 120%.

Social Security doubled your money. America’s other public pension funds quadrupled it.

But yeah, sure, the real problem with Social Security is the taxes. It’s the benefits. It’s all the peasants living too long. That’s the problem.

This is like a drunken driver totaling 10 cars in a row and blaming the transmission. Or maybe the upholstery.

If any private sector pension plan invested in the same way, the people running it would be sued into oblivion for breach of fiduciary duty. This level of scrutiny mirrors the approach seen with casinos without Swedish license, where operators must navigate complex regulatory landscapes to ensure fairness and trust, even when not under Sweden’s regulatory umbrella. A financial adviser who kept all his clients in Treasury bonds throughout their career would be drummed out of the business.

None of the solutions need involve investing the whole thing in the S&P 500 SPX, +0.39% or (much better) a global stock market index fund. It’s not about one extreme or another. Most pension funds are about 70% invested in stocks, 30% in bonds.

But even a 30% allocation to stocks in the Social Security trust fund would have doubled total returns since 1980. No kidding.

If they’d made this change a generation or two ago, there would be no crisis. Nobody would be talking about higher taxes, lower benefits, or working into our 70s.

It really isn’t complicated. At last, only about 80 years too late, some people in Washington may be getting a clue.

Brett Arends: “A dollar invested in Treasury bonds in 1935, with all the interest reinvested …”

SS does not reinvest the interest; it pays it out in benefits. The primary purpose of the trust fund (as the program developed since 1939) is to provide a buffer. The buffer implicitly required by the annual report is one year’s worth of costs. The buffer most of are used to is enough to deal with the bulge of costs created by the Baby Boomers.

If the TF had enough to pay benefits from earnings (as Arends’ math requires) it would be as large as the entire capitalization of the NYSE. Imagine how much that would depress the ROI. Note also that the S&P removes and replaces stocks that are headed toward delisting, so it overestimates the 75-year results. While Arends’ math is self-consistent, it is wrong.

Arne

I wish you would expand on your comment here. I find the post hard to follow: i can’t always tell who is “talking.” and it contains a description of my (your and Bruce’s) proposal which is incomplete and misleading. I don’t know if the author is using a kind of shorthand to describe what the worker woud “see”, but it needs to be said “one tenth of one percent per year.” Leave off the per year and they will accuse of lying.

the “investors version” here was tried by Bush II in his second term. It was a lie, and it failed because back then there were smart people who could show it was a lie, and because there were other smart people who knew how to organize mass protests that would tell the Congress in ways they could understand “touch it and you will die.”

I think we are out of smart people, unless you can help us.

I agree it can be difficult to see where run is commenting and where he is quoting. I clicked through to see the extent of his quote of Arends which start at:

and goes to the end.

My comment does not address where run quoted Dean Baker, nor run’s own comments. My purpose was to show that Arend is not only making a bad comparison, but while his math is consistent, his assumptions are not consistent. It’s bad analysis all around.

If you click through and read the article by Dean Baker, of which run quotes only one paragraph, I think you would see that (one thing) Baker is saying is that the size of the expenditure needed to keep up scheduled SS benefits is comparable to the size of the expenditure needed to educate all those baby boomers. In my paraphrase: since the economy was able to handle our kids as “dependents”, it can handle us as “beneficiaries”.

Arne:

It does makes sense. I do not agree with Brett. I do agree with Mark on Money.

Don’t confuse MMT’s explanation of how a fiat money system works with the policies advocated by MMT.

All government spending competes with the private sector for the goods, services, and resources that are available. That is true whether the government is buying an aircraft carrier or sending out SS checks. The government is in the unique position of being able to pay for ALL of its spending through money creation. The government must impose a tax to remove money (created from government spending) from the private sector so the private sector does not have the money to consume all the goods and services being produced. Thus allowing the government to consume without causing inflation.

The private sector typically saves some of its income. This savings is the same thing as non spending. This allows the government to spend more than it taxes; in other words run a deficit. This is why government deficits equal private sector financial savings (treasury securities).

The true way to save Social Security is through productivity gains. This will allow more output with fewer workers or greater output with the same workers. This will allow the government to consume the same percentage of the “economic pie” for SS. Since the “pie” is bigger, SS is getting more. In my opinion, the best way to increase productivity is through higher wages. Capitalist will always try to maximize profits. If wages go up, capitalist will look for ways to reduce labor costs while increasing output. That is the definition of productivity.

Mark:

“The government must impose a tax to remove money (created from government spending) from the private sector so the private sector does not have the money to consume all the goods and services being produced.” Does it really have to impose a tax to balance outputs and inputs?

Markg

most of what you say here is at least almost true, and it is almost what every modern country already does although they don’t use the words you use.

The point about Social Security, about which you are completely wrong, is that the workers pay for it, they own it. This is an important feature of any economic transaction. You cannot create money out of thin air, It has to be tied in some way that people recognize to productivity of the people who get to spend the money, The deficit hawks in Congress are huge liars about the debt and deficit. If you implsed MMT as the way of talking about creating money, they would just go ahead and lie about that because all they are interested in is directing as much money as the economy will bear to the people who already know how to direct as much money as the economy will bear to themselves.

I don’t like MMT much because the people who try to explain it never really do. It’s a bit like the magic asterix that Reagans first budgets always included. I have no problem with deficit spending,,,though we ultimately get i trouble if that spending does not lead to increases in product [productivity is a magic word reserved for economists].

I especially don’t like it when MMTers imply thatt Social SEcurity can be paid for by just p rinting the money..somehow letting some mysterious invisible hand adjust the economy so the money goes to the producers of what the no longer working are buying, and those workers have no claim on that money whatsoever. Traditiona ideas of money work very well. The problem is with the debt hysterics and liars. It would be nice if you could fix that by changing the words we use, but they will just find new lies. Meanwhile Social Security must be paid for by the workers themselves,,,by a finacial instrument called pay as you go financing, which is almosst exactly the same as ordinary banking….the government guarantee is NOT the same as “the government pays.”

I will accuse you of short sighted thinking, not becaause I want to be mean to you, but because I want you to know that I think you don’t quite understand what money is, and you don’t understand Social Security at all. You, of course, are free to try to explain it to me so I understand it (MMT) better…but watch out for that magic asterix.

Dale:

I am not sure I would say he does not understand what money is. By the very nature of his comment, he displays his knowledge of money or currency. Your point on understanding what Social Security is, is what you should be discussing here.

Run

sorry. what money is goes deeper than anything i have heard an MMt-er or Congessman say. I would hazard that it has something to do with the faith people have that the money they get for “work” representsat least rough justice for the work they did.

Creating money out of thin air to give to retirees and then taxing “the rich” to prevent inflation is no more just that taxing the rich to pay for your groceries in retirement because they have more money than you. neither is cutting benefits for retirees so “the money” can be invested for “higer returns and profits for brokers and CEO” at a risk the people were paying to avoid.

So far i have not heard a MMT-er consider this aspect, and i have never heard a congressman say anything that made any sense at all.

Currency is not money. those worthless iou’s in the file cabinet are. curreency is just a substitute for money that makes it easier to trade worthless iou’s where paperwork is not necessary.

and yes, I am being a bit provocative here trying to get people to actually think about what we are doing.

you seemed to unersand this when you pointed out the importance of “ownership” back when you agreed with me about Social Security.

Coberly, the nature of a fiat money is the government spends it into existence. See this article https://www.bep.gov/media/1016/download?inline

During the civil war the government was running out of money. It did not tax “greenbacks” from the public because greenbacks didn’t exist. The government created them and spent them into existence. Of course now it is all done electronically. Money is only printed to satisfy the amount of “pocket money “ the public desires to carry. The federal reserve bank puts paper money (federal reserve notes) into existence by buying assets (typically treasury securities) from the public. It is an equal value exchange and does not change the private sector’s wealth.

As for SS. Think of GDP as a big pie of all the goods and services produced. Retired people are not producing any of the pie and many have no income to buy any of the pie. If the government gives them money to buy a piece of the pie it must take money from the producers of the pie to prevent them from consuming the whole pie. There are other factors that can affect this. When workers save instead of spending their entire income, this “frees up” some of the pie. The trade deficit can add or subtract from the pie.

One thing to note is taxing someone 20 years ago to accumulate a SS trust fund in no way changes the size of the pie today. You still have to divide the same pie whether the trust fund has $2 trillion or nothing. Productivity gains will allow the size of the pie to get bigger. Instead of a 10 inch pie it would be 11. Workers would still get to consume the 10 inch pie and retired people the added inch. In other words, workers would have the same living standard while still having the same SS benefits.

Hope this helps.

True

No. it is wrong. in the first place banks have always created money…which hopefully people spend into the economy encouraging “investment”..that is creating more product, including capital like machinery etc.

More important for us, the money people put into social security reduces their demand for immediate consumption. they get their ability to demand product back when the government pays them their pension. this works fine as long as there are people putting money into social security…reducing their demand for product…transferring that to the now-retired. this is not a Ponzi sceme. everyone knows the rules and there is no need to fear the chain will be broken: people will always need a safe way to save for their retirement. The money from generation to generation is automatically adjusted for inflation by pay as you go financing (an explicit sytem that does what ordinary banking does implicitly). the extra money (real dollars) that retirees get is made possible by growth in the economy. this may be a predictable result of the security that social security provides people, or it just may be a way for ordinary workers get to share in the extra productivty they produce by being good workers adding to the profit taken by explicit investors,,,who would probably say “no, no, I invested that money, the profit is all mine, mine I say. Mine!” That may be a moral or psychological question. Personally I think the answer is obvious… the “profit” was created jointly by the workers and the investors exercising their own particular talents and is realized..agreed to… by the agreements we make as political actors about how we are going to recompense the cooperation. right now we have a “compromise” that seems to work better than winner take all capitalism or state take all socialism.

Mark

your last paragraph says much the same as mine Except you want to break the ink of ownership, and i think making it explicit is critically important. as much because of the way people work (behave) as because of the way money works.

you talk as if, and most people seem to believe that as soon as a worker retires he loses all claim to whatever other people are producing. so he must be taking charity from the rest of us. Social security, or any financial instrument that transfers money across time, dispels that illusion by making the payment for the financial instrument an explict claim on future product. as long as everyone agrees to this arrangement things go well for all. but when you start believing your claim on product ceases the minute you stop working, everything goes to hell, this principle was first put in print when someone wrote “honor your father and your mother so your life will be long in the land.” note the last phrase.

we have come so far in our understanding that when John Kerry said this in a debate with Bush, jr, the reporters covering the debate said “what the hell does that have to do with it.

thing is, families have had a rough time of it over the years and SS had to be invented so we could accomplish as a nation what families used to accomplish out of some, no doubt Darwinian, instict for cooperation.

all of this makes me wonder why i bother. people can’t think. all they do is shuffle around the sound bites they have heard until they feel better, never mind how things actually work, or the human emotions that cause them to behave. Buying a Ferrari to drive around town is stupid. But the mechanics will fix them just the same, even overhauling the engine after the driver decides to save money by not changing the oil.