Stand Aside Millennials, Baby Boomer homebuying bonanza

Except for the beginning, mostly a copy and paste here. Housing is an issue in the U.S. There are not many appropriately priced house being built or used ones on the market. The same holds true for apartments. We have a lot of young families trying to figure out where to live. Then once they decide, they can not find the necessary housing much less the pricing they can afford. Now, I said it twice. Do you get the picture?

The author has described the situation rather well.

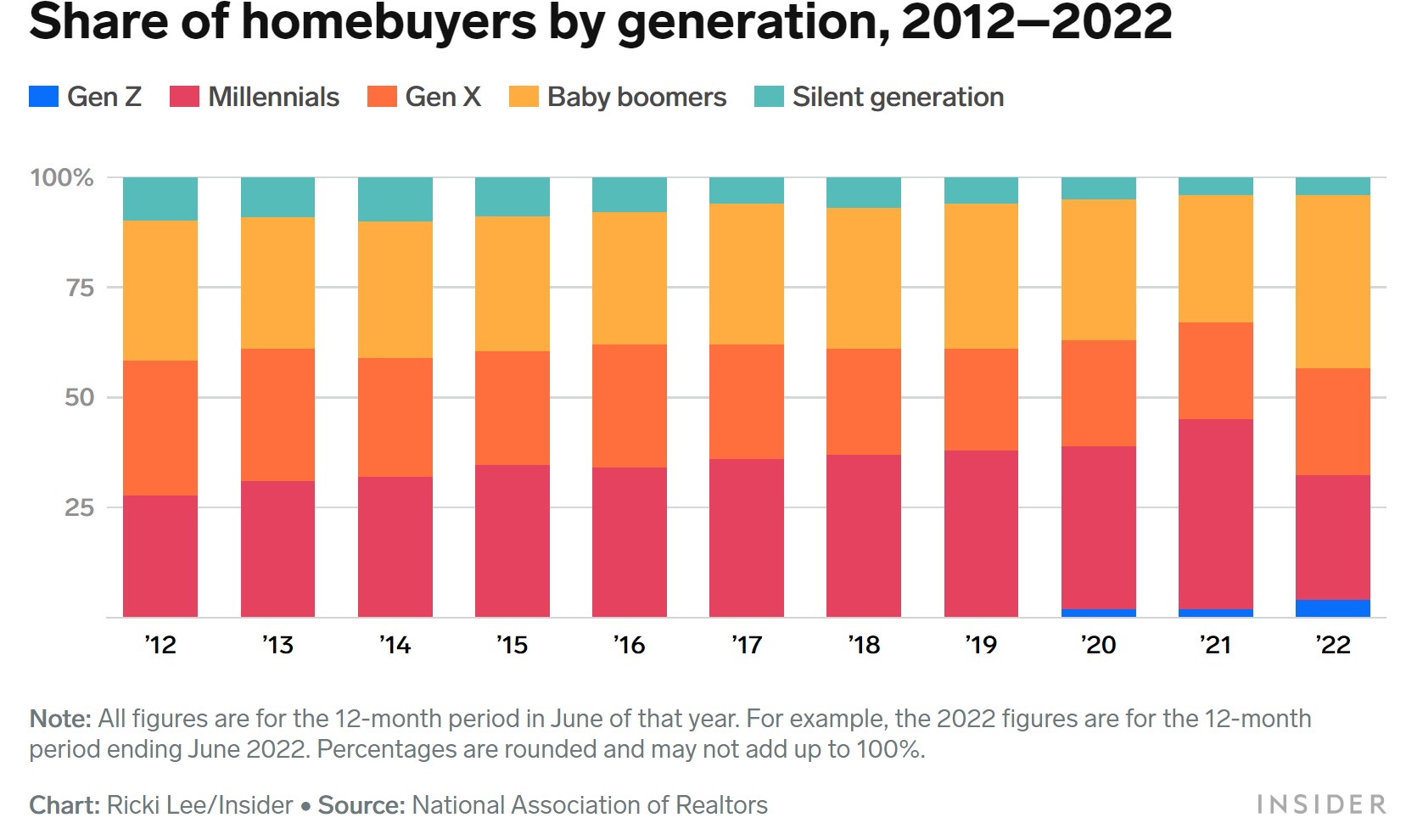

What makes this more troublesome is the large generation who are going out the door to oblivion in the next couple of decades has been buying up the market. Mid 2021 to mid 2022, Baby Boomers bought up 39% of the housing market, High demand, housing shortage, and the price goes up and others are priced out of the market,

Boomer homebuying bonanza, INSIDER, James Rodriguez

Millennials have never had it easy in the housing market. A mountain of student debt, widespread housing shortage and stiff competition from their deep-pocketed elders kept them on the sidelines longer than previous generations. Despite these challenges, the sheer size of the generation, combined with the fact that many of its members have now reached prime homebuying age, means more millennials are literally getting their foot in the door with each passing year.

But after a decade in which the “avocado toast” generation sat atop the housing-market heap, baby boomers have suddenly and unexpectedly seized the upper hand. Between July 2021 and June 2022, boomers were the largest share of homebuyers for the first time since 2012, according to new data from the National Association of Realtors. Boomers purchased 39% of all homes that sold during that span, up from 29% the year before. Millennials, on the other hand, saw their share of the market shrink to just 28%, down from 43% the year prior.

Despite the numbers game favoring millennials, a slew of other factors conspired to allow boomers to stick it to their successors. The main thing, though, was cash. Boomers are more advanced in their careers and in many cases have already spent decades amassing home equity, making them much more likely than other generations to fork over all cash for their next property. And when bidding wars become the norm, it pays to offer a lump sum.

While the sudden reversal is a sign of the financial strength of boomers, it also underscores the bleak prospects for millennials and the growing divides within the generation. For better or worse, homeownership is the most popular form of wealth building for most American households. When millennials are forced to delay their home purchases and continue renting, they miss out on years they could have spent stacking up equity. Millennial homebuyers are also more likely than older cohorts to use financial help from friends or family, further tilting an already uneven playing field toward the “haves” who are able to tap resources from previous generations.

The housing market is not a generation-versus-generation cage match. But at a time when there aren’t enough homes to go around and homeowners rely on rising property values to build wealth, it can feel like the prosperity of one generation has to come at the expense of another. And in this battle between youth and wisdom, it appears gray-haired house hunters are taking one last chance to trump their less-seasoned successors.

Cash is king

Millennials have been an economic Eeyore for years. The Great Recession threw a wrench in their early careers, and the slow start meant that, compared to previous generations, they had a worse chance of making more than their parents. In the years that followed, builders didn’t produce enough homes to meet the looming wave of demand from younger buyers. Between 2010 and 2019, homebuilders started roughly 21,000 single-family homes per 1 million people each year, barely half as much as they were building in each of the three decades prior.

But by 2019, millennials were getting on better footing: The long recovery from the recession meant the labor market was in a strong place, savings were picking up, and they overtook baby boomers as the largest living generation, with a population of 72.1 million people. Though millennials were delaying traditional life milestones and finding themselves with less wealth than previous generations, they were buying more homes than ever.

That was all flipped on its head during the pandemic. The long-gestating undersupply of housing, near record-low mortgage rates, and a suddenly footloose workforce sent home prices soaring — and the competition to find a new place to call home became fierce. A generation that should have been reaching its homebuying sweet spot instead fell further behind.

Jessica Lautz, the deputy chief economist and vice president of research for the National Association of Realtors, told me . .

“There are more millennials than anyone else. So the fact that they are now trailing behind the baby boomer population just speaks to the difficulty of the housing market today.”

Boomers, meanwhile, came of age during years of healthy housing construction. In the 1960s and 1970s, homebuilders averaged roughly 50,000 housing starts per 1 million people each year, well more than double the rate during the 2010s, according to the National Association of Home Builders. This building boom helped drive homeownership — more than half of boomers owned a home by the age of 30, compared with 48% of Gen Xers and 42% of millennials.

Boomers have also sustained their homebuying activity longer than their predecessors, who were more likely to settle into one home. The share of recent buyers who were 60 years and older grew 47% from 2009 to 2019, which means millennials “face more competition from their parents’ and grandparents’ generations than their predecessors did,” a Zillow study found.

When the pandemic rolled around, boomers were able to leverage their economic advantages to jump back into the market like never before. Cash purchases have been on the upswing since the beginning of 2021 — this past October, roughly a third of homebuyers paid with all cash, the highest share since 2014, according to Redfin. The pivot to cash gave boomers a leg up, since they had plenty of home equity to tap.

Over the past decade, the average homeowner accrued roughly $210,000 in equity, according to the NAR. And as the typical down payment for a home more than doubled during the pandemic — peaking at $66,000 in May 2022, according to Redfin — the ability to use cash savings or the profits from a home sale benefited more senior buyers. During the NAR’s latest survey period, 51% of older boomers, aged 68 to 76, paid with all cash, compared to just 6% of buyers 32 years and younger. That dynamic, Lautz told me, has played a significant role in the rise of older buyers. She said;

“If they’re not paying all cash, they can put down such a large down payment that they’re able to compete in a very successful way.”

A new era

While millennials are primarily buying homes in an attempt to get on or move up the housing-wealth ladder, boomers’ recent moves were primarily motivated by the desire to slow down. The cohort, who range in age from 58 to 76, told the NAR that their moves were triggered by an urge for a smaller property or to be closer to friends and family after retirement. Boomers typically moved the farthest distance of any generation — a median of 90 miles for young boomers, and 60 miles for older member. Lautz said.

“They’re finally at a point in their life where they can purchase their retirement property.”

Given the fact that many of these moves were made with the intent of settling down, it’s hard to tell if boomers will maintain their dominance or if this is a blip from an unusually dysfunctional year. When I asked Lautz to weigh in on the comeback’s sustainability, she hesitated to make a prediction. Lautz . . .

“Is this a lasting trend, or did boomers make their trade last year and now they’re set in their retirement properties? It’s hard to say right now.”

A lot has changed in the housing market since the NAR’s survey period. The competition for homes has slowed considerably, thanks largely to mortgage rates that have risen from historically low averages of less than 3% during the pandemic to about 6.4% as of late March. Less competition is especially good for millennials, as the past few months have shown: More first-time buyers appeared to be winning out on homes, Lautz said. But these kinds of buyers are also much more likely to take on loans, and therefore disproportionately affected by higher borrowing rates. Once again, boomers are more insulated from the whims of the market than their younger counterparts. Lautz.

“While first-time homebuyers suddenly saw their affordability hurt by the rise in interest rates, people who are paying all cash didn’t. They’re not going to have the same challenges.”

Even if nationwide home prices continue to slide, they’ll likely remain dramatically higher than they were before the pandemic. And baby boomers have already shown a desire to stay out of nursing homes longer than their predecessors, meaning they’ll probably play an active role in the housing market for years to come. In a housing market of “haves” and “have nots,” equity-rich homeowners have the edge over hopeful first-time buyers. That’s not changing anytime soon.

Millennials know that they have time on their side, since boomers will eventually age out of the market entirely. But playing the waiting game may not be the best strategy — there are already signs Gen Z is coming up right behind.

I’m having trouble reconciling the narrative here that boomers are flush with cash with the “boomer retirement crisis.”

https://www.barrons.com/articles/baby-boomer-retirement-crisis-51675271205

Joel:

I do not know how much of this was being driven by people leaving certain states having sold their homes there and moved to less costly places. In 2020, we found AZ to be affordable and the home priced appropriately.

In 2021, we were out bid by 10 and 20-thousand dollars and we had went 5 -10 thousand over price It was not just pricing, it was also cash-deals.

The same as the author, I think it is a blip also.

We got our new home only because our realtor entered our name in a drawing and I am a veteran which they prize. They did not find out I was an ass too till later when they were balking on fixing issues.

Am I rich? Nope! I have to watch what we spend with an eye to future years.

Our supplemental insurance went up 10% in cost from last year 2022 and 25% since 2021. Healthcare insurance is expensive. Doing without it can be even more expensive. Maybe we are lucky? Did fate strike me with all it could in the past where I do not need more insurance or does it have more to hit me with in the future? Then there is dental.

I report on stuff I may agree and disagree on too.

I was thinking along the same lines, we’ve seen a lot of that in C Oregon, boomers flush with California cash buying real estate as investments, financing a gated golf-course community lifestyle. Slum-lords, so-too-speak …

In 2022, we were outbid by 15-20 thousand dollars on three houses in the Providence area of Rhode Island. That was with cash offers and waived inspection. We were able to buy a house that hadn’t yet gone on the market, so we were the only offer.

But my question wasn’t about you or me. I keep reading about a retirement crisis for my generation, and yet this same demographic is driving up housing prices. I can’t make those two statistical descriptions align.

I’m on the crisis side of that equation and yeah, it doesn’t quite fit …

Joel:

We are not upper crud. We were at the bottom of the upper 20% in our mid-sixties. So, yeah I hear you. When I went turned 65, Jan started to collect on mine. That is partly how we got a greater saving. Then working from home, we saved more from less expenses. I still could not match them even with the sale of our home in Michigan.

You and I are typical, I believe.

I wish this had not been presented in generational terms. There is already a strong push by evil persons to create a sense of aggrievment among young people toward old people. The young may be suffering from a serious of economic disasters mostly created by free market uber alles policies since about Reagan, but that is not the fault of “boomers.” most of whom are just as poor as i am. thing is, i was able to buy my house before the “we are a nation of home owners” surge under Bush that led to 2008 fiasco. And now we have corporations buying up housing and gouging the renters,

as for the apparent contradiction between rich boomers buying property and poor boomers can’t retire…i think you are not understanding. the boomers can retire,,,they have paid for their retirement in advance. what will happen is that as the boomer generation fades out, the following generation will be living longer..at least the rich ones will,,, and that will require an increase in the payroll tax, which the coming generation does not want to pay because they have been told they are paying for the old.

i would guess that there are forces affecting the housing market theat might be related to the size of the boomer generation…but these forces are not “because” of greedy geezers, they are the “natural” working out of the so called free market…if you don’t mind a little monopoly pricing in your free market. SS solves the free market problem. the housing market has not, cannot, because it is unregulated.

What’s being missed here is that a lot of Boomers need housing, too–smaller, well-appointed units convenient to transportation and healthcare and with minimal yard space. An ample supply of elder units would reduce the competition for starter homes, which downsizing Boomers are now forced to compete for. And, as Boomers leave their 2500 sq ft homes, it would allow younger families to trade up, again freeing up starter homes.

If you don’t believe me, ask any realtor where Boomers can go once they sell their current homes. The answer is pretty much ‘nowhere.’ So they just continue to occupy homes that are too large for them.

I began advocating for this 20 years ago, but so far neither government planners nor the building industry have shown much interest.

John:

There are older life style communities which people move to. I have seen them up north. We opted mot to do so. From 2600 feet on two-thirds of an acre, we downsized to 1475 on a lot 45 ft wide by 120 ft and not in an older community. Our younger neighbors watch over us. We are both in our seventies. I understand the issue. We like it although a bit more space outside would be nice. There is no grass to cut.

You may have to move which is no cheap was to do.

Have you ever moved to a new home? It was an interesting experience. You trust the builder to do what is right. Except, so many of them are in a hurry to sell. I would recommend doing a walk through two weeks before Closing and make notes of what needs to be fixed. I would do it again at one week and not everything needing to be done.

After Closing, we found 15 items needing to be fixed. One (major + others) included the driveway which was sloped stupidly from left to right to match a six-foot long sidewalk. When we finally closed, we moved into the house and could not use the driveway even with the slope. The dumb asses dropped the dumpster on the sidewalk and cracked the five parts of it. Oh, they gave a letter telling us it would get fixed.

Three weeks later, it was. It reminded me of the movie The Money Pit(?). Where the contractor calls Tom Hanks up and says “Its your luck day, we drew your name out of the bowl and we are going to fix your house.” The Construction Manager called three weeks later (redundant alert) and said they would pour that week! Party time!

The Construction Manager and I had conversations. He mentioned company attorneys and I mentioned mine. He made it sound like I brought it up first, except I did not. What I did do was explain that when you come to a closing, you are certifying the house is complete which includes everything. After the attorney remark, I explained what the UCC is about and “Reasonable Man.”

He promised to have the 15 items fixed by year’s end. It took till February. They have new homes to build and I was a distraction to this. For the other ten items, I filed warranty claims. One year after closed they are fixed.

To your point, newer homes on smaller lots are a great idea. Or even Condos. The HOAs are manipulative, lying bastards. I do my stuff in writing and Certified mail with them. I leave my real thoughts on the side. I would suggest people scrap verbal and do it all in print. HOA’s in Arizona are not to be trusted. They have a huge influence in the legislature.

As you point out, it is a problem for us. Plus, many of us trust, lack gumption, and the intellect to push back. I did not want the battle. New homes present problems for older people too. The Gov moves in the direction the money moves.

Thank you for your comment. I enjoyed reading your words.

Yes, I’m well aware that there are some units available for seniors….but not nearly enough for the hoards of Boomers. We spent a good five years trying to downsize. Starter homes were just not right…too far out, layouts for families with kids, too cheaply built. There were also retirement dormitories with a few “cottages” on the property. Nothing a little upscale with 1500 sq ft. We finally sold last year to a middle-aged woman. We spent a year in an apartment. Now we’re about to move into the perfect apartment in a continuing care community. The costs are insane, but they are committed to taking care of folks who outlive their money. Few Boomers will be so lucky.

John:

I hear what you are saying. I did not answer Joel’s comment completely either and he is similar to us.

Communities are starting to mandate certain types of housing. We did, back in Michigan. So many had to be affordable. Typically, two and maybe three bedroom smaller homes on smaller lots. It was not walkable but it was the right idea.

We also planned a life style community which included apartments, condos and single homes along with a commercial area which would have grocery stores, etc. Sidewalks and green space. It was near a major highway and it was possible to get to a major hospital and other places via commercial transportation. No light rail or busses yet. In a good area. I lived there and sat on the Planning Commission as the Vice Chair.

The home is mid-range for being upscale. The mortgage rate was right.

What I see happening is builders controlling supply and also an larger influx of people. Many people moving from more expensive places. They could have built more. But they did not.

As far as LTC, I bought into it 25 years ago for my wife and I. I “think” we are ok. I gues we will know when we get to it.

Thank you for your response.

run

would your planning allow for construction of homes for the otherwise homeless. small, cheap, but basic-living-able.

my idea would include a no-default mortgage with equity as the incentive to maintain and eventual resale back to the government to be used as future homes for the homeless, including emergency shelter during disasters. not fully thought out…but in some way the only answer for the mass homelessness created by no-rules banking.