The remedy for high prices is – high prices

2023 data begins with another lesson: the remedy for high prices is – high prices

– by New Deal democrat

And so, another year begins. And kicks off with a look at the leading housing sector. And furthermore, there is even some good news.

Total construction spending in November rose 0.2% for the month, while the more leading residential construction spending declined -0.5%. While total construction spending is only down 0.6% from its recent high in July, residential construction spending is down -8.1% from its recent peak last May:

This is in line with the steady drumbeat of negative news in the housing sector for the past year.

Generally speaking, residential construction spending comports with the number of housing units under construction. But in 2022, like in 2018-19, spending (blue) has declined while the number of units under construction (red) has risen slightly:

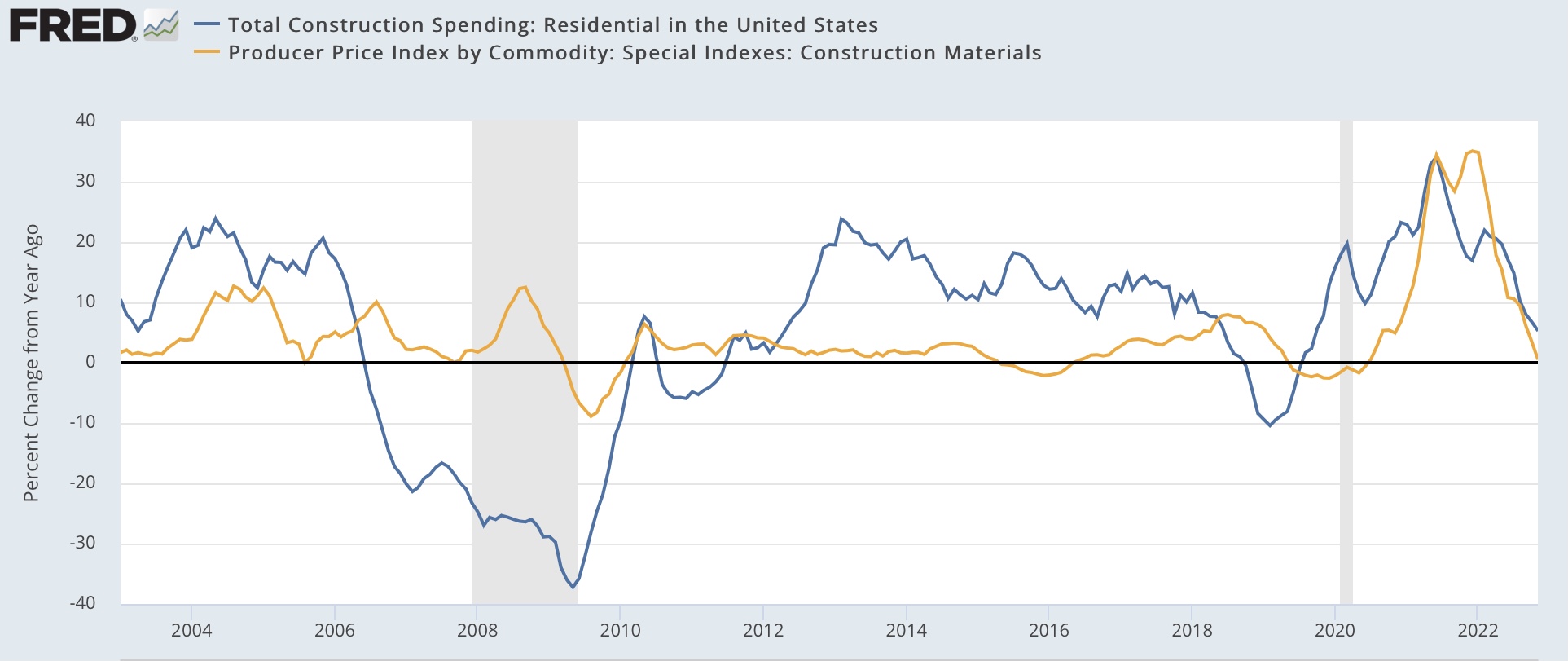

The answer probably lays in the costs of construction materials, for which there is a special inflation index, shown in gold YoY below compared with the YoY% change in residential construction spending:

The cost of materials increases and decreases with a lag once there is a boom or bust in construction. This is what happened in 2018-19, and it happened in 2022 as well. The cost of construction materials, which was up as high as 35% YoY one year ago, as of November was only up 0.6% YoY!

The remedy for high prices is – high prices. The good news is, with the complete abatement in the rise in the price of construction materials, some of the pressure is taken off of construction sales.

As I’ve already mentioned several times, while I am watching for coincident indicators like employment and consumer spending to turn down, I am already on the lookout for a positive turn in some long leading indicators. And the abatement of construction costs increases in the housing sector is one such sign.

“August existing home sales: confirmation of housing prices peaking,” Angry Bear, angry bear blog

Speaking of ‘High Prices’…

The Football Game Theory of Inflation

NY Times – Paul Krugman – Jan 3

If you don’t think of economists as party animals, you’re right. Or at least that’s the conclusion one might draw from the fact that several prominent economists carried on a thoughtful, earnest online debate about inflation over the past weekend — that is, on New Year’s Eve and the day after, when I thought we were supposed to be drinking champagne and then nursing hangovers.

But it really was a good discussion — the kind of thing I was looking for all those years ago when I chose economics as a profession, relatively free of politicization and nastiness. That is not to say that it was without political implications.

The discussion was kicked off by Olivier Blanchard, the former chief economist of the International Monetary Fund (a towering figure in the profession, who happens to be one of the economists who has gotten recent inflation more or less right).

He started off by making a point that he said is “often lost in discussions of inflation and central bank policy.” He went on: “Inflation is fundamentally the outcome of the distributional conflict, between firms, workers and taxpayers. It stops only when the various players are forced to accept the outcome.” …

At one level, of course Blanchard is right. Companies that charge higher prices and workers who demand higher wages aren’t doing so because the money supply has increased; they’re trying to increase their incomes (or offset declines in their incomes caused by, say, rising energy prices). And inflation happens when the attempts of firms and workers to claim a bigger share of the economic pie are inconsistent, when the additional purchasing power being demanded exceeds what the economy can deliver.

Reading the discussion, I found myself remembering a remark made way back in the 1970s by William Nordhaus, another eminent economist (and Nobel laureate) who happens to have been my first mentor in the field. Nordhaus compared inflation to what happens in a football stadium when the action on the field is especially exciting. (If you don’t find American football exciting, think of it as a soccer match.) Everyone stands up to get a better view, but this is collectively self-defeating — your view doesn’t improve because the people in front of you are also standing, and you’re less comfortable besides.

Now, what people who claim that inflation is caused by a hot economy are saying is, in effect, that while the immediate source of stadium discomfort is that people are trying to get a better view of the action at others’ expense, the root cause of the problem is that the game has gotten too exciting. Companies would always like to raise prices and workers would always like to negotiate higher wages, but they only go for it when sales are high and jobs are abundant. Cool things down: Make the game less interesting — that is, push the economy into a slowdown or even a recession — and people will return to their seats — that is, inflation will slow.

And that is, in fact, basically the policy major economies are pursuing to control inflation. The Federal Reserve and the European Central Bank are raising interest rates in a deliberate effort to slow their economies and risk recession, precisely to persuade companies that they no longer have “pricing power” and persuade workers that they can’t demand such big wage increases.

But is that really the best we can do? We want football games to be exciting; must they remain boring to keep spectators in their seats? …

i do wonder how raising interest rates in 1 country will solve a worldwide problem? in this case the US isnt immune a worldwide inflation soke, and will require worldwide resolution to solve. since the supply chain crisis is also worldwide, and doesnt react to interest rates. course its also created by business, not governments

well, i thought rising pices would reduce spending..at least on things you don’t need. pretty much the point of Econ 101. it was only in Econ 102 that we learned rising price caused more spending, driving prices up in an inflationary spiral as workers demanded higher pay than they were worth. and now we learn that people have more money than the economy can keep up with so the Fed has to reduce investment. it’s a good thing they do this all with math…the subject, according to Bertrand Russell in which we never know what we are doing or whether it is right. Me, I remember when Volker tried that trick and tried that trick and it never worked until something happened and then they all said, “see,” aren’t you better off than you were last year?’