Housing unaffordability closes in on bubble peaks

Housing unaffordability closes in on bubble peaks; expect substantial price declines and increased foreclosures in the likely oncoming recession

– by New Deal democrat

I last looked at the issue of housing affordability at the beginning of April. As we all know, mortgage rates have continued to skyrocket in the past several months. At present they are just under 6.10%:

This has changed the calculus on housing affordability considerably. So let’s take a look.

In April house prices in real terms were already almost identical to their 2006 highs. Depending on what house price index you use, nominally prices are up somewhere on the order of 60% since then. For example, here is a graph of new home prices and the FHFA index for the 2000s:

And here is the past several years:

Meanwhile, the median price for an existing home peaked in July 2006 at $230,200. As we saw yesterday, as of last month they were $402,000.

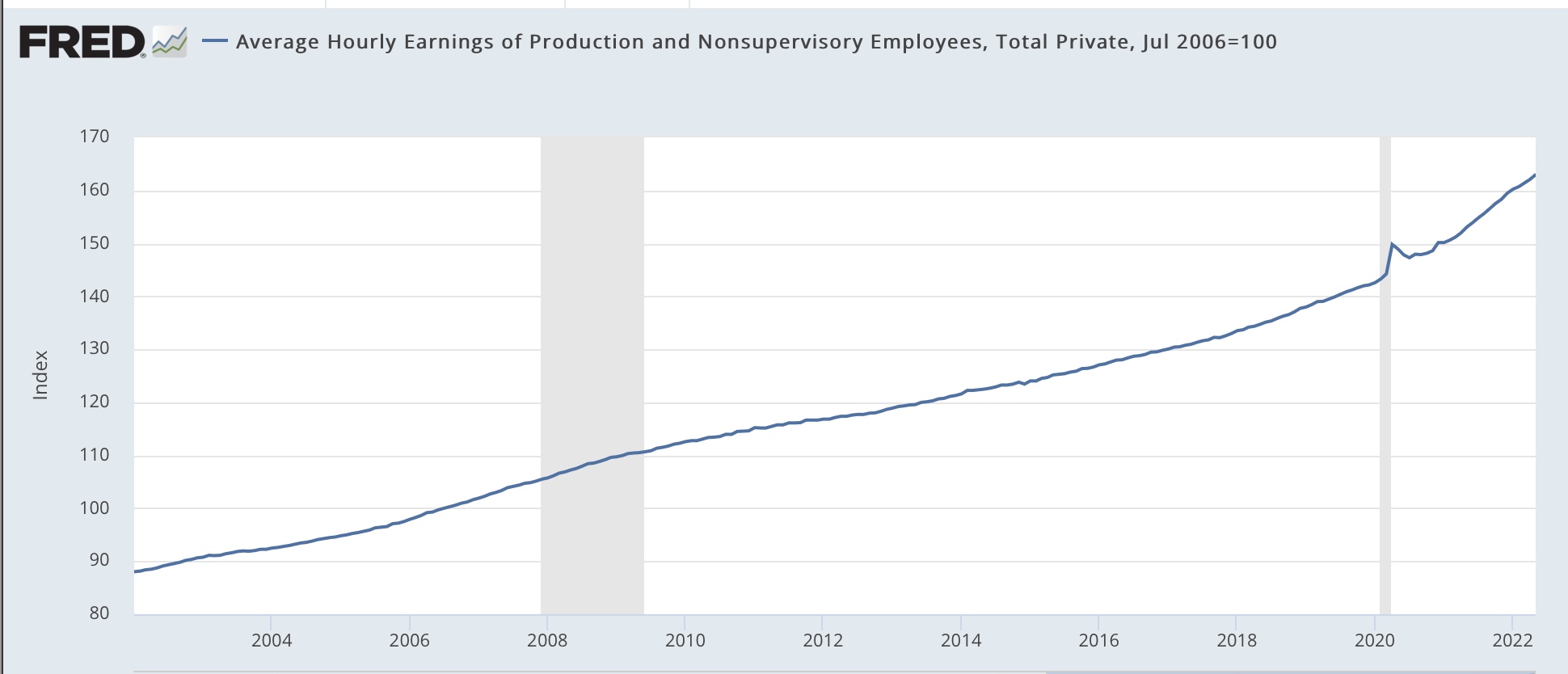

Average hourly wages for non-supervisory workers are also up a little over 60% since 2006:

Since in real, wage-adjusted terms, house prices are about the same now as they were at the peak of the housing bubble, let’s compare an identical mortgage then and now as well, for simplicity’s sake using $250,000, at the prevailing mortgage rates. Here’s the monthly payment for each:

April 2006: $1865.

July 2006: $1913.

April 2022: $1583.

June 2022: $1798.

The bottom line is that the average monthly mortgage payment has increased by about 13.6% in the past two months, and now is about 96% in real, wage-adjusted terms, of what it was at the peak of the bubble.

Even before yesterday’s report, the NAR’s “Housing Affordability Index” had dropped to 105 in April. How low is that? Well, for comparison here’s what the Affordability Index was during the 2000s:

At the worst of the housing bubble, it sat right at 100.

In short, housing is equal to its worst affordability levels in the past 35 years.

Frankly, I have been very surprised at this, since mortgage lenders are being much more careful now than they were at the peak of the bubble when anything that fogged the mirror could get a loan.

This changes the calculus of the housing market – and the economy – going forward significantly.

While I don’t see the banking system fallout that we had in 2008, when all the birds came home to roost on those ridiculous loans, creating a cascade of financial system defaults, I *do* now see it as being almost inevitable that there will be another significant decline in house prices that will last a number of years. This will trap a large number of younger homeowners in houses that are financially “underwater,” as they make payments on a house they can’t sell for the price at which they bought. And an increase in unemployment during a recession next year that looks increasingly inevitable will mean a substantial increase in foreclosures for some of these buyers as well.

Not so good.

I do not understand how recent interest rate rises affects more than homes bought using those interest rates as opposed to affecting housing affordability for the entire country. Further, banks are back to actual underwriting, so large default rates are not in the picture at all. Now, if unemployment takes off that may cause a rise in defaults, but that is a long way off.

I do not “quite understand your question or comment. Fed Rates impacting Mortgage rates across the country have a varying degree of impact to buyers. As you know southern AZ is/was going out the roof for prices. We snagged an assumable mortgage at 2.65%. We also bought the house at a lower price by two weeks. A house going for $315,000 a year ago is not going for $370.000. If we use 2.7% from a year ago and 5% which was a month or so ago. The following occur with a 5% down payment.

2.7% to 5% with $15,000 down on $315,000 goes from $1205 to $1610.

2.7% to 5% with $19,000 down on $370,000 goes from $1400 to $1884.

Thats housing. I had this discussion with a housing construction manager about why younger people balk at a 5% mortgage pre – 6%.

Home building is not the most efficient process either even in spec-homes. Our builder was dropping the dumpsters on the sidewalk cracking them. These had to be replaced. Why? I asked how many nails it take to build a house. Didn’t know. From my perspective, there is an awful large amount of waste which contributes to cost.

If my inventory sits after I build it, I have a lot of fixed-cost built into it in manufacturing. If I can not sell it in a short amount of time, I have no profits to pay my bills and labor. So I might try a short term loan. Fed Rates go up and short term loan rates for businesses go up. Or the businesses can not get or afford the loans. All of that money given to businesses, that qualified for them, was a big deal as it kept workers employed and companies open.

One could almost say it was the sowing of the seeds of future inflation. Stimulus really paid off today when the economy is compared to 2008.

I am probably not to clear on this.

Construction managers did not like me; but. they did not screw with me either.

The increases only effect those who have bought recently. Has no effect on people that bought before. In your example with $19,000 down you are paying $1400/month. Your not suddenly going to be paying $1884/month. Your affordability does not change.

While there have been slight increases in adjustable rate mortgages which will have an effect when they adjust (if the rates are still high), that is a small percentage of mortgaged homes in the country.

EM

It is the “same house.”

My point was not clear enough. I am talking to Construction Managers who do not understand why a young couple would not snack up a the $315,000 (2.7% mortgage) home which became $371,000 (5% mortgage) in a new section. They said the mortgage rate was “still” far lower than what it was when we were experiencing mortgage rates at 12%.

Yes, it only effects those who buy recently. To the Construction Managers, this is still cheap. They could not understand why they would not snatch up 5% mortgages which is what they were offering. However, the monthly payout increases $679/month and only if you put $19,000 down. Did the house actually increase ~18% in price to accommodate cost in one year? Somewhere between $1205 and %1884/month lies a buyer’s number. They were saying buyers were balking 5%. I am saying yes 5% is an issue but so is your rent-taking price which has increased ~18%.

ow, did I answer your thoughts?

By the way, they do not like me. Especially when I tell them, you can not inspect quality into a product, you have to build quality into the product. In other words, don’t lose a pound of nails per mile. How many 2/4s do you use to build this model house? Why do you allow the “dropping” of dumpsters on sidewalks? Put timers down or place the dumpsters on dirt.

My dad was a bricklayer/tuckpointer. I learned from him. I learned house framing in high school as well as wiring. I shingled roofs while I attended college and after I was married. Plus I consulted in manufacturing and have a LSS Black Belt. They do not like me at all even though I am polite.

I was just talking about the affordability rate measurement.

EM:

And I missed a simple point and went well beyond your point in an explanation not exactly answering you. I would say, the homes are unaffordable to many and this will only worsen. Sorry . . .