A housing warning: affordability, at long last, is approaching its housing bubble nadir

A housing warning: affordability, at long last, is approaching its housing bubble nadir

If current price and mortgage trends hold, we are about 6 to 12 months away from matching the very worst housing affordability at the peak of the housing bubble.

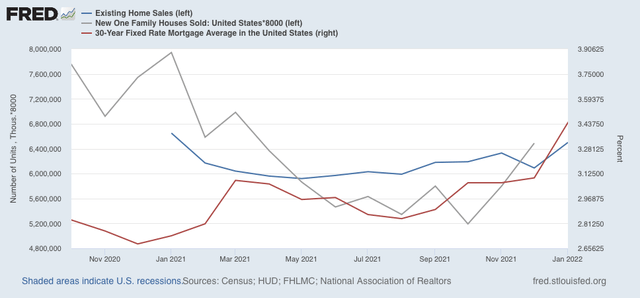

Let’s start with a comparison of existing home sales (blue, reported today for January), new home sales (gray), and mortgage rates for the past 16 months:

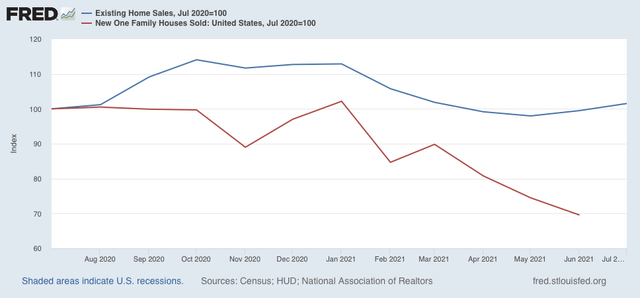

Note that the NAR doesn’t permit FRED to show sales more than 12 months previously – but here is the graph I ran 6 months ago:

The bottom line is that both existing and new home sales declined – with the typical delay of 3 to 6 months – in response to moderately higher interest rates early last year. When interest rates declined again during autumn, new and existing home sales responded – again, with a delay – by heading higher.

Now here is what mortgage rates look like up through this week:

Mortgage rates have jumped by about 0.75% since January 1, only 7 weeks ago.

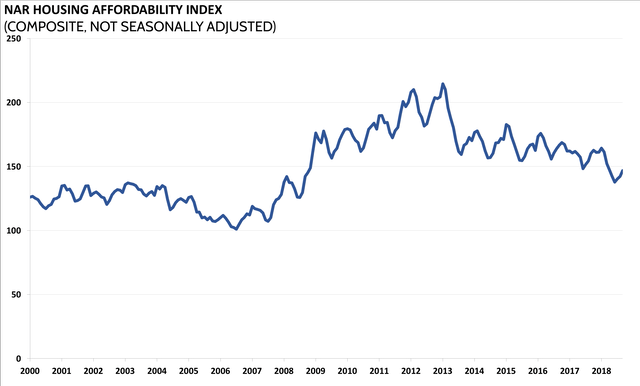

The saving grace in the housing market for the past several years has been that, while the down payment cost of a home was the highest ever in comparison with household earnings, mortgage rates were so low that the monthly carrying costs were nevertheless relatively modest. The NAR publishes a “Housing Affordability Index” taking that into account. Here is the long term view:

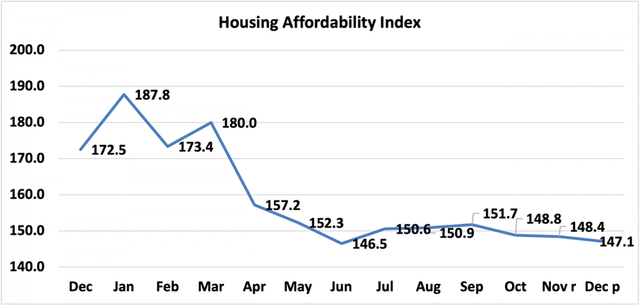

And here is the latest graph through December:

Thus this does *not* include the jump in mortgage rates in January and this month so far. And bear in mind that since the house price component of the index is not seasonally adjusted, and January is typically the nadir for house prices, we can expect this index to deteriorate substantially in the next several months.

In fact, by my calculations, this most recent jump in mortgage rates makes monthly mortgage costs the highest since about 2007, and only about 15-20% lower in real terms than at their worst at the peak of the housing bubble in 2005. And if house prices continue to appreciate during the next 6-9 months the way they have for the past 24 months, we will match that peak.

Prices follow sales, and after the last few buyers lock in sales before mortgage rates go higher, I fully expect sales to decline substantially, and prices to follow suit once they hit their breaking point later this year.

I see no mention of income, which seems strange (especially for NDD) in a affordability post. Calculated Risk shows this. Seems to me that affordability levels better than most of the last 50 years is not a bad thing.

https://calculatedrisk.substack.com/p/real-house-prices-price-to-rent-ratio-ade?utm_source=url

https://cdn.substack.com/image/fetch/w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F28dbd2ed-0bd9-484a-bee8-79707362b439_1131x672.png

Average individual income is one thing and real median household income is another.

https://fred.stlouisfed.org/series/MEHOINUSA672N

Real Median Household Income in the United States

FRED graph at link

I would post the image of the graph if I knew how.

True. However the comparison is still valid as the same type of income is used through the years.

EMike,

[From the article at the link that you provided.]

Calculated Risk Affordability Index

I’ve put together my own affordability index – since 1976 – that is similar to the FirstAm approach (more of a house price index adjusted by mortgage rates and the median household income).

*

[So there McBride (who is no dummy) was using median household income, which solves the problem of averages and a reduction of the number of individual incomes in households, but not the correlation problem of median home to median homeowner household given that the bottom 30% of household incomes are nominally renters. Roughly the median home is bought by households around the 65th percentile of income distribution. In any case, the FRED graph showed that median household income had dipped sharply in 2020 while 2021 figures were not yet available. So, dunno yet. Most people able to buy are also aware of McBride’s if “now is a good time to buy” question.

My childhood was mostly spent with our median income family living in a median priced home and we were house poor. My parents fought each month over the bills and how little of my dad’s pay check was left for him to spend on gas and fishing and hunting, which put meat on our table most of the year. I worked the 1/8th acre garden in our backyard myself raising all of the vegetables that we ate year round except for corn. We grew our own corn when we lived rural before my age 10 and had a one acre garden.]

My back yard was a stoned parking lot for the equipment owned by the plumbing contractor downstairs. Had a lovely view of the railroad tracks also.

EMike,

Before we rented rural in Occoquan, VA, we rented baby urban in Fredericksburg, VA. We rented what was once a jail and it was on the wrong side of the tracks. Although our block had the poor whites further on were only blacks. Fredericksburg was a typical small southern city with all the charm of Selma before integration. I did not understand why the black kids walking down the ally threw sticks and stones over the fence at this pre-school whitey, but knowing what I know now it amazes me that I did not turn out like my outwardly racist father. We moved to Occoquan in 1954 just as I was starting grade school. Later in life when I was a high school senior my dad had more black fishing buddies than white, but it was a different time and place in Orange, VA, when my dad was happier in his own life and our community was much under the influence of Marion DuPont Scott, who still was alive and my dad’s occasional employer. My mom grew up like a chapter out of The Help mixed with a play by Tennessee Williams. So, fate had her marry down the second time around to disinherited mountain man from moonshine country.

I have found that what I have read has informed my intellect but my life and the lives of those near and dear to me have informed my character, albeit often contrary to their own intentions.