Freeing Former Students of Loan Debt, a Conversation

An Intro and some history:

Alan Collinge at Student Loan Justice Organization. Alan has collected 1,065,931 signatures on his petition asking President Joe Biden to cancel student loan debt. His new goal is to reach 1.5 million signatures. If you believe in the cause you should sign his petition. Petition · President Biden: Cancel Federal Student Loans, and Return Bankruptcy Rights to the Rest. · Change.org

Just a signature is all Alan is asking from you.

I have known Alan Collinge for well over a decade. Angry Bear has always featured his words on student loans. Canceling student loan debt should not be so arduous. In support of the previous comment, I am making some rather broad assumptions believing they are mostly true. Repeatedly, I am reading comments about student loans being far larger than the original principal.

Going Forward

In was a while back when I put forth a broad-based “assumption” of interest, penalties, consolidation fees, and interest on top of interest (former) having surpassed the original principal of the loans. Much of this is strictly based on observation and commentary of student loan holders who have experienced their loans increasing and doubling due the factors and penalties I have mentioned. A consolidation can end up doubling the size of the loan.

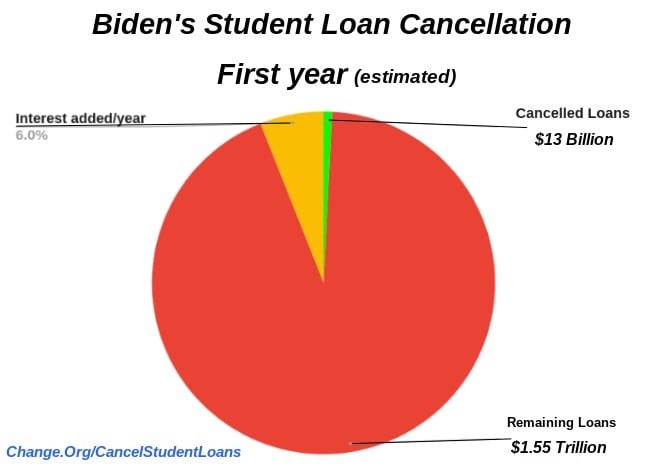

The recent cancellation of some Student Loans for people who worked in public positions has resulted in $13 billion (shown in green), a small part of the $1.55 trillion in student loan debt. Meanwhile interest on student loans on the balance is accruing at approximately 6% with older borrowers paying higher interest rates (8%). Correct me if my math is wrong . . . the yearly interest would equal $60 Billion on $1 trillion or in this case ~$95 billion annually.

Student loans are the gift that keeps on giving, if paid.

So who is holding the bulk of this debt?

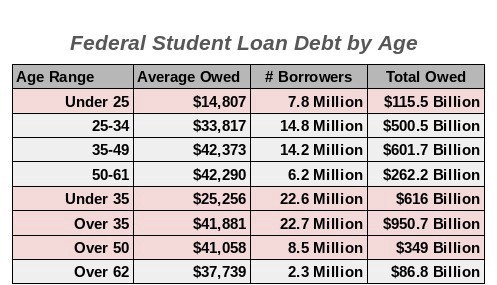

Another chart used by Alan Collinge breaks Student Loan Debt by Age bracket. Roughly two thirds of the debt (~$951 billion) is being held by those 35 and older. Thirty-six percent ($349 billion) is being held by those over fifty years of age. The chances of those over 50 and going into retirement dwindles with each year passing. The total dollar amount held by those 62 and older has not dwindled much.

Indeed, many of holders of these loans will have a portion of their Social Security disposable income attached by the Federal Government to continue paying student loans. And again, If there were penalties, consolidation and recasting fees, interest in forbearance and interest on top of these additional costs; more than likely it has equaled the principal of the loan or a significant amount of it. At this point, it makes little sense to chase loan holders to the grave.

Some Points:

run75441: Would it hurt the government, if these fees were wiped away as they were not a part of the original loan and are what I would call usurious or just plain outrageous? Normal and every day loans do not face the same penalties. In the end, the nation wastes more money on Defense and gives away more in tax breaks. More giveaways than what student loan holders owe and who are having their feet held to the fire.

As I have alluded to in the past. Student loan holders have paid more interest, penalties, and fees than deserved which appears to have surpassed principal. Many have just stopped paying their student loans.

More Conversation:

It appears Democrats have given up on helping . . .

Alan: We don’t know how much of the $1.566 Trillion is actual, unpaid principal vs interest. We also don’t know the repayment history. My best guess is that only a couple hundred billion are actual unpaid principal. It could even be that the loans could be cancelled entirely with no net-loss to the government (although I think this may be unlikely).

It is just that due to lost loan repayment histories, buying and selling of the loans consolidation rehabilitation, etc, no one can say for sure. So our opposition simply says “we don’t know”

run75441: Senseless . . . This has been handed off by both Republican and Democratic led administrations over the decades.

Alan: My best guess is that only a couple hundred billion are actual unpaid principal. It could even be that the loans could be cancelled entirely with no net-loss to the government (although I think this may be unlikely).

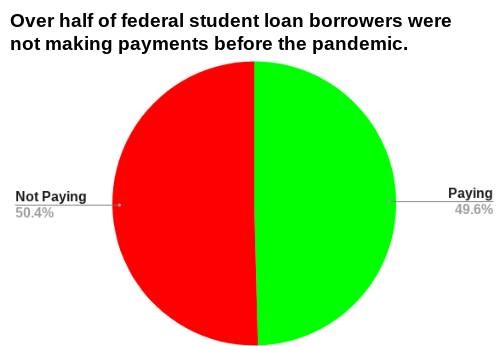

I would also suspect far fewer than the 49.6% paying their loans back now would continue after the pandemic.

- Pie Charts and Table provided by Student Loan Justice Org,

Probably worth noting here, too, that many years (decades) worth of White House Budget data show that the federal government has been making a not-insignificant profit- not a loss- on defaulted student loans. This is a very peculiar and disturbing consequence of the loans being stripped of both bankruptcy protections and statutes of limitations: https://studentloanjustice.org/defaults-making-money.html

I think that canceling the loans makes economic sense. I also think that the government bears some (perhaps, equal or more) responsibility as a consequence of the bankruptcy laws, privatization, and failure to protect students from the for-profit universities that sprung up around the loan programs.

Ken:

A bit of discouraging history: JOE BIDEN BACKED BILLS TO MAKE IT HARDER FOR AMERICANS TO REDUCE THEIR STUDENT DEBT

He should be doing something today to mitigate this issue.

It’s among a lot of things that need to be done where America is just not there yet. People quote the old tropes without thinking.

Should add: Student loans greatly affected college tuition across the board.

Ken:

As much as there may be some degree of blame to be laid at student’s feet, the results of this are little more than servitude to the servicers of these loans. Dems and Biden still do not appear to be willing to extend themselves in granting bankruptcy for students who are into this, years after the loans were initiated. The table showing student loan debt by age is really telling.

The economy—

When production went offshore, America, like the UK before, turned to finance and debt (turns out the service economy was a canard). Student loans, like healthcare, become a complex, an industry, replete with lobbyists. It is all so interconnected.

Ken:

From about 1995 onward, Congress has made it difficult for people with student loans to declare bankruptcy. This is outside of the 1978 SCOTUS Decision Marquette National Bank of Minneapolis v. First of Omaha Service Corp.

This was a “unanimous U.S. Supreme Court decision holding that state anti-usury laws regulating interest rates cannot be enforced against nationally chartered banks based in other states.” In other words, states could not regulate banks. My 10% line of credit (which was high) was suddenly 18%.

“Justice William Brennan wrote that it was clearly the intent of Congress when it passed the National Banking Act that nationally chartered banks would be subject only to federal regulation by the Comptroller of Currency and the laws of the state in which they were chartered, and that only Congress or the appropriate state legislature could pass the laws regulating them.”

Citibank, squeezed by interest rate caps, decided to move its credit-card operations out of New York City. The company persuaded Bill Janklow, then governor of South Dakota, whose agricultural economy was struggling at the time due to high fuel prices, to persuade that state’s legislature to formally invite the bank there, as required by federal law before a national bank can do business from a state. He then successfully lobbied the legislators to pass a bill drafted by the bank that repealed the state’s cap on interest rates, something a small group of legislators were already trying to do. Citibank quickly moved the 300 white-collar jobs in its credit-card division to Sioux Falls, where it has been ever since.

SCOTUS figured Congress would fix the law. They didn’t.

Notably, House Rep and later on Senator Joe Biden spear headed a series of bills making it harder and harder to get relief from student loans. In 2018, I challenged Senator Debbie Stabenow in public at a Garden Party in Michigan to rescind her vote on the 2005 Financial Modernization Act. I had donated to the Democratic Party a few hundred just shy of being reported as a contributor. She waffled in her response and I doubled down on her for approving the bill. In the background younger people were clapping.

Sure banks are using their power to mane Main Street because Congress gave them the power to do so. Indeed in 2008, Main Street rescued Wall Street and paid big time. Blame Congress and Greenspan for banks becoming powerful. Just recently, Congress released 25 of them to fewer requirements by raising the amount of capital they control.

Hey Ken:

Been writing for Alan and student loan justice for over a decade now. Just giving you some background. Not arguing. I really appreciate your input. Matt Tabbi and others have joined the plunge on this topic also. They put together a special tape too,

All student loans need to be canceled. Out of the recent student loans forgiven, such as the Public Service Loan Forgiveness (PSLF) loan holders that were able to finally have payments made count as “qualifying payments” only helped forgive a small portion of lenders’ loans.

As a public servant, over 10 years of payments were made on my student loan, and none of the payments qualified me to have my student loan forgiven because I was in private sector during those years. All the years I have worked as a public servant, the pay is so low, and financial obligations so high being a solo parent and only financial provider in my household that I have not been able to make a single payment after becoming a public servant. I have already paid the same as what I originally owed, even with very low interest, but I owe more now due to undisclosed charges, fees, etc.

Canceling all student loans will help all citizens, boost the economy, restore faith in our systems, and allow many people to take care of themselves and others more effectively. Also, return bankruptcy protections to student loans so students and co-signers on student loans can have a chance to cancel their debts.

Simple and painless solution. QE for student loans. Have the FED buy all the debt. Reduce interest to 0% and increase the terms to 100 years.

Yeah but that would kill half or more of the economic stimulus that would result from simply cancelling the loans. Tens of millions of people will be able to buy homes, start businesses, etc without a huge loan debt showing on their records.

Returning bankruptcy is really the first, most obvious fix. S. 2598 will make that happen for federal loans. It has a very excellent chance of passing…

Payments on each $100,000 of loans would be about $83 a month in my scenario. That’s not gonna stop anyone from buying a home. And the amount of debt on a credit report has very little effect in the case of an installment loan.

Hmmm

A $100,000 loan that grew from $30,000. You are ignoring what has caused this growth. These are NOT normal loans. Am I speaking in German or Russian out here???

I feel like I missed something in his comment but regardless, that’s not standard repayment so I assume he would be in an IBR. If so, he’s paying $83/mon20 yrs but not paying off the ever growing balance.IBR may sound good but most people wind up getting kicked out because of some little thing like them losing your yearly recertification of income. Something Alan had noted could easily be obtained from the IRS. If you make it through, as things stand, prepared to deal with an IRS bill the year the remaining balance is forgiven. This illustrates the dirty tricks servicers are allowed to get away with. This lending system is set up to cause borrowers to fail, not succeed.

Dweeb:

Your argument should always be “there is no path to bankruptcy as is granted by the courts on normal loans either immediately of over a stated period of time which still has some relief.”

Student loans are not the same as mortgages where you have 30 years to pay them off. At 15 years which is typical, the payment will be $726/month. At 10 years which is more common, the payment is 1,000/month. Let’s use 20 years or $591/month. My information is from the most recent interest rates for Undergraduate students.

A simple Loan Calculator is here: https://www.bankrate.com/calculators/savings/simple-loan-payment-calculator.aspx

For Undergrads subsidized and unsubsidized Direct Loans the interest rate is 3.73%. Unsubsidized as you well know, starts gaining interest from day one. Parent Direct Plus Loans (no escape here either), the interest rate is 6.28%. Grad Student Plus Direct Loans pay the same as Parent Loans unless subsidized. If the Grad student qualifies for a Direct Loan the get such a deal of 5.28%. What is calculated does not consider subsidized loans to which the subsidies end 6 months afterwards.

Student Perkins Loans are 5%

As a parent, I was an ass. I would not let mine go to where they offered Stafford loans. My advice was, if they offer you money, they want you. If not, try another college or university.

If you get a grant plus scholarships of 50% just cut the payment in half.

Run is right. There is no good reason to lend this unconstitutional, catastrophically failed, and hyper-inflationary lending scam any more credibility, legitimacy, or legs. Failed lending scams need to be allowed to fail. Let nature take it’s course, not make it into a zombie.

The Founders called for uniform bankruptcy laws and equal protection under the law for a very good reason. This exception is it.

Examples:

Showing some examples of badly screwed up the student loan program is from start to finish (if there is ever a finish).

Shannon: I was refused an income-based repayment plan unless I rehabilitated my loan, including a consolidation. My loan balance increased an incredible amount and when I protested, I was told there was no way to undo it even though all the fees and penalties had not been disclosed before the consolidation. There was no reason to deny the income-based repayment. I had direct loans. They just wanted to be able to tack on all the fees.

MO: On my way out (the Navy) my exiting instructor pushed Itt Tech and gave them my info so they would hound me this is 1993. I agreed to go to a open house and check the school . Itt Tech showed job stats , job growth and big dollars but it was all lies the government printed stats for them without validating them. I lost my GI bill plus $30k so here’s the cost: 8 years military , 3 years school, 15 years to pay back loans on min wage. I’m now 54 I never worked in my field of study, always made 1/3 of what I was suppose too , not worth the struggle . Through all of this the VA defended Itt Tech and screwed us over.

I did all the right things but lost. I stormed the Hill with VES , was in the New York Times but no help. My life is ruined and no one will help pre 2006 Veterans scammed by Itt Tech, my state politician’s were bought and paid for and won’t help. I reached out to each administration and they look away , Miguel Cardona push’s shots but won’t help. Suicide looks attractive but not a answer.

Dweeb: Bringing defaulted FFELP loans out of default gives the Guarantor a way to sell the loans as SLABS* (securities) to private investors and they get paid by ED again when the borrower defaults again.

*SLABS are similar to MBS. They tranche them also according to risk. Also this is like selling your loan to a bill collector. The loan has been rehabilitated.

Beverly: That’s exactly what I refuse to do. I have an FFELP loan. If I consolidate to a Direct Student loan, I taking what started as $43K in principal where the principal turns into 150K+ in principal and over 300K with interest. I will be in my 80s paying off a student loan from my teens. I am hoping that they eventually remove the accrued interest and forbearances that was added to the original loans or bankruptcy. I would hate to have to file bankruptcy and f*ck up my otherwise good credit.

Larry:I have been in repayment since 2006 and filed in 2009, which did absolutely nothing for me. I am now in default and administrative garnishment (since 2012) and my garnishment amount is actually far less than my payment would be. The downside -like all else with this predatory system – is that, barring loan forgiveness, there is no end to this shit until I drop dead. Still, I’ve learned to live with less money and am happier than struggling to try to pay an insurmountable debt that is comprised of fees and interest and actually increases each month. I’ve had the original amount I borrowed extracted from my wages and would owe $000.00 if the fees and interest weren’t there. Right now, because my loans aren’t being reported, my credit score with the three major reporting agencies is between 760 and 780, depending on which one you check. Still, if bankruptcy is put back on the table, I will file tomorrow.

Jennifer: I have been a teacher teaching in Title I, rural schools for over 25 years. My student loans are triple what they started at and I’ve never qualified for not one dollar of relief. I cannot own a home, buy a new car, or afford to put enough into my retirement that when I am forced to quit teaching, won’t be enough to even make a payment on my loans as they currently stand.

When I was young and pregnant, our school financial counselor convinced my husband and I to consolidate our loans to lower the payments. We did. 2 years later he died after a bone marrow transplant and I was left to support a 4 year old and a 10 month old on a teacher’s salary. Our loan payment was more than made. I often worked 2 or 3 jobs and took classes at night just to stay ahead of the payments. After defaulting once, I owe over $300,000 and it grows every day.

I’m in an income based repayment plan, but everytime I get a raise or a better paying job, my payment increase to cover that raise. Meanwhile, the cost of living keeps increasing and I still.only have the same amount to spend a month as I did 25 years ago.

I’ve been through bankruptcy once. Didn’t help much. I’m tired y’all. I was told if I went to school, got a good teaching job, my loans would never be a problem…..it was a lie. I will never be able to pay these off. After many, many attempts to get into a loan forgiveness program, I was accepted. I have 6 years left on my loans with no guarantee they will be forgiven. WHY can’t I get credit for teaching in the most needy schools?

Something is wrong here. I’m 52 and I’m too tired to work 3 jobs. I’m better off quitting and getting a minimum wage job. I have no way out and no way to get to a living wage. Explain to me why was I told I had to go to college to begin with?

Kim: Denise, you’re very fortunate. The company who owns my student loans, Edfinancial, consolidated mine with a parent plus loan at 7% interest. This is not what I had agreed on and no one in the company cares. My loans are triple what they were when I graduated. I’m glad that this did not happen to you! No one deserves it

First: I believe that student debt should be forgiven..for a number of reasons.

At least the normal bankruptcy (formerly normal?) laws should apply.

Garnishing Social Security should not be legal.

that said, I hope (daily) that people will not accuse me of having the opposite beliefs.

I think the party that “holds” the debt is the party to whom the debt is owed, and not the party who owes the debt, as appears to be the usage here. I could be wrong,

Ordinary mortgages end up c0sting the borrower more than the original amount borrowed, so that may not be the best argument against student debt.

Interest on interest is normal. I think banks may not call it interest on interest, but that is what they collect anyway while not calling it that. So that may not be a good argument against student debt. I could be wrong.

In normal borrowing there is an assumption that the borrower knows what he is doing and has a “moral” as well as legal obligation to repay what he borrowed.. including interest and interest on interest. So you may have a hard time convincing people who “pay their debts” that student borrowers should be forgiven. Especially if it appears that taxpayers will be paying the debt for them.

I honestly do not know how much I am right or wrong about any of this. I suspect Biden doesn’t even know. I am sure voters don’t know. So I am not arguing that student debt should not be forgiven, I am arguing that you need to make better arguments.

As to why I do think student debt should be forgiven: Many of the loans appear to be for payments to fraudulent providers of “education.” Even “honest” (traditional colleges) appear to be selling services that the provider knows are not worth..in money terms… what they are represented to be worth.

The “economy” has not justified the faith the government put in “education” to justify the student loans.

Banks, making other loans, engage in practices that amount to gouging the borrower. ALL bank loans need to be better regulated.

The country does not do well by allowing people to fall into unpayable debt//debt peonage.Especially it should not be in the business of luring people into a debt trap.

Again, I don’t know if I am right or wrong about any of this, but I suggest you try to manage your message so you answer my doubts, and possibly convince the people who ought to be on your side.

Coberly:

You have done very little to examine the issue. This is in no way like a mortgage, a car loan, etc. loan. Your comparison has no foundation which get me back to the start of my response to you. Interest on top of interest on top of penalties, etc. which should not even be occurring is the issue. You refuse to read the entirety of what I said Coberly.

You conflate what is being said which can not be absolved by your beginning sentences.

Run

no point in yelling at me. I did read what you wrote. I may not have understood it. Can you please try to make it more clear to someone as uninformed as I am.

con·flate| kənˈflāt | verb [with object] combine (two or more texts, ideas, etc.) into one: the urban crisis conflates a number of different economic and social issues. please explain to me how “interest on interest” is different from “compound interest” which is what the bank pays to you. I asked my banker to explain how the bank deals with “unpaid interest.” i did not understand his answer. he avoided the “interest on interest” language, but i think (could be wrong, but it won’t do any good to just yell at me if i am.) try to explain the difference between what the bank does with unpaid interest that is different from what student loans do. one thing the bank can do..and the county in the matter of property taxes..is to foreclose on the loan. not sure how you would foreclose on a student loan.

i raised a couple of points that, again, i could be wrong about, but if i don’t understand them I would bet any audience you are trying to reach will not understand them either.

of course, as we hav seen, most people don’t need to understand something. they just need to think they have a reason to get mad, or go mad, about it.

not looking for absolution here. just suggesting you might want to consider explaining it for the unwashed.

conflate: i stuck the dictionary definition in there, and forgot to punctuate it clearly. did you mean i am conflating mortgage loans with student loans?

well, not exactly. i was saying explicitly that student loans look to me (almost) exactly like normal loans, and asking you to explain why they are not. not assert; explain.

for what it’s worth:

i paid off a friend’s mortgage to stop the bank from putting him out on the street. they charged me not the original value of the loan, but the remianing principle plus unpaid interest (which I assumed included interest on unpaid interest, plus about 25% “fees” to pay off the loan.

which was about 80 times as much as my not cheap lawyer charged me to arrange the pay off. So I know something at least about greed amonting to fraud by banks.

but you have to hand them the hook. personally i have never had a credit card, or failed to pay back a loan well before it was due, so i have never personally encountered those fees, penalties, or interest on unpaid interest.

now, i am tired, old, likely to make mistakes, not understand, or be completely off the subject. it won’t do any good for us to yell at each other, if you can’t explain your position, I will stop asking.

I don’t think you quite understand the uniquely vicious and predatory nature of these loans. Home mortgages have bankruptcy protections. Student loans do not. They also do not have statutes of limitations. Take these away, and you give the lenders (including the federal government) license to lie, cheat, steal and ruin. And…this is precisely what they are doing with (up to this point) no recourse. The founders called for bankruptcy in the constitution, and the consequence of removing it is like nothing you have ever experience, or will ever experience with any other type of loan.

Elizabeth Warren said it’s like the students are the turkey at the Thanksgiving Dinner. She was being kind.

How to describe what’s wrong with student loans in one comment is impossible but I will list a few things that spring to mind. First, the point of government issued or backed loans is they are not normal loans. They’re for country & citizen benefit, for people who wouldn’t normally be able to borrow from private lenders.Since these loans are backed with taxpayer dollars, repayment costs should be minimal .E.g., low interest rates. Due to poor government policy & oversight, every aspect of this has been botched. Instead of generous repayment terms, we have hyper-inflated loans & a predatory lending system. The loans typically are bad out the gate . As Catherine Austin Fitts , former Sallie Mae board member when still a GSE said, in the documentary “Scared2Debt, Sallie Mae Not part 1” , she would describe generation of these loans as massive fraudulent inducement. There wasn’t a meeting of the minds,I.e., the borrower & lender were not on equal footing regarding what the terms of the loan really entailed. These loans often negatively amortize because servicers have directed payments to interest only, allowing much larger capitalization amounts since principal is going up, not down. In a home mortgage , You know from the start what You will repay. (Truth-in-lending) & a certain percentage of each repayment will be applied to principal . Less principal, less interest accrued & balance will go down, not up. Negative amortization isn’t allowed in 28 states because it’s a debt trap / predatory lending . There are a lot of solutions to remedy student loan debt if government can/will implement them successfully. However, absent loan forgiveness, that begins with bankruptcy rights and consumer protections being returned.

Dweeb

agree with most of that. not sure you have considered what happens when you get late on your mortgage payments. up to a point what you DO pay is applied to interest first.

What happens when your payment does not even cover the interest is not clear to me. I suspect that the unpaid interest is just applied to the principle and you pay interest on that until you catch up. But I don’t know that. The bank guy I talked to was not clear.

I don’t know that my state (considered a good government state) has an anti-debt trap law, but I doubt it as I knew people paying 40% interest which at the time I thought violated usury laws. I asked. They answered “what’s a usury law?”

I do know that when a payment is late there is a penalty fee..and those penalty fees can get pretty creative. I think you are right that this is a governmnt FU and needs to be fixed. But last I looked the goernment is owned by the banks,

Coberly,

My point with the mortgage analogy really was only that some of your payment must go to the principal.

Student loans are uniquely predatory, bereft of ALL consumer protections. You can refinance at a lower interest rate with a mortgage, you can’t with student loans . They found a way around state usury laws by saying as federal loans , states didn’t have jurisdiction. So many corrupt practices & actions associated with student loans have occurred it’s impossible to list them but it’s shocking. Just use your imagination think of what a lender could do to a debtor who had no rights. That’s the situation student borrowers are in. About the only thing they don’t do yet is put debtors in jail. No truth-in-lending , no statue of limitations, no usury laws, no bankruptcy protections. If its more profitable for a servicer if loans go into default and they face no real consequences,what do you think they will opt for ? Maybe a slap on the wrist before getting their contract renewed by the Department of Education is the worst punishment contractors have faced. Meanwhile the borrower is stuck with the “illegally” increased balance. I don’t know how else to explain it any plainer. There is no defense of this lending system and nothing to compare it to.

It’s very hard to explain that to a public who is barraged with a very simple but effective message. They are told by the educational lobbyists in collusion with government , colleges, & corporate media that student borrowers are bums looking for free handouts, it’s unfair to those who paid, and the taxpayer will be stuck with the bill. If you follow Alan & student loan justice for one, there are researched , documented rebuttals to all the media generate rhetoric . It’s a lot to take in and too much to explain in a couple of comments.

I think you pointed out that typically , you roughly pay about about twice what you borrow on a mortgage. There are millions of us who would take that deal in a moment because we are way past paying the borrowed amount twice. Try three, four times and the balances just keep climbing . Just using common sense, what sort of government backed program is can morally & ethically justify its existence when people pay on school debt 20-25 years in an IBR only to have it forgiven but then facing a tax liability on a six figure sum ? If they default for any reason , which most due thanks to poor servicing , well, they’ll have income garnished and the debt forgiven at death.

Even writing this out reminds me how insane the whole student loan system is.

Apologies for typos & grammarmistakes.Difficult to do this on a mobile device

Dweeb

I understand (in part) how criminal student loans are. Please understand that.

What I have been trying to do is get those who know more about it that I do, to be more clear…you are doing fine. In particular, when they say “only” student loans charge interest on interest, i think they are wrong. they might be right, but so far no one has even tried to explain why they are right. just curse me because they think i am defending the lenders.

this has been a common problem on AB lately..question, or make a suggestion about, part of someone’s post and get damned as a fool for failing to see that they are against something bad. so am i aginst something bad, but i think it would help if we knew what we (they) are talking about.

so, who “holds” the debt? the borrower or the lender?

no apologies for typos needed. they have become a fact of life for me.

Morality and good faith in lending is a two way street. All pretense of good faith was removed from the lending system with the removal of bankruptcy protections, statutes of limitations, and other bedrock protections that exist for every other loans.

They time for judging, moralizing, and finger wagging is now long gone. The lending system is now failed, catastrophically, and I would say a national threat at this point.

The loans WILL NOT BE PAID. Period.

At a minimum, the bankruptcy rights that exist for all other loans must be returned. At this late date, however, it will proves to be far easier and economically stimulative to simply cancel (not forgive) the loans.

Alan

I agree with all that. I am not so sure you can make “will not be paid” an actual fact. perhaps the borrowers will all die first. but i am sure that in that case the government will make the lenders whole. meanwhile the borrowers (debtors) lives are pretty miserable.

Less than half of the borrowers were paying before the pandemic. Almost no one is now. If even 25% of the borrowers are paying in, say, June-July, I’ll be stunned.

It’s not a matter of what we “make” happen. It’s just the reality. The lending system is rigormortising. People are done. The pandemic has opened their eyes.

“daily” I meant to write “vainly”. can’t blame this one on spell check. but daily is just as true.

I am eligible for retirement now, but cannot retire due to the need to continue teaching to qualify for PSLF.

If Biden erased all the predatory fees, interest and interest capitalization, my amount due would be zero.

I have already paid back more than 2x what I borrowed. The government would lose nothing by forgiving what I “owe” because the amount of money they actually lent was paid back long ago.

This is what the govt. will gain if the exorbitant/unfair interest due was removed so I could retire:

1. A job opening for a younger teacher which allows that person to start their career, start their life, pay taxes etc.

2. Savings to my school district because a first-year teacher salary is much less than a teacher of 23 years.

3. Because I plan to substitute teach after retirement, my district will also gain a qualified sub at a time when they are in desperate need.

4. If they forgave the exorbitant fees and interest for everyone, the govt would no longer need to contract with loan servicing companies who have purposefully withheld information on programs to help borrowers; irresponsibly lost paperwork; and charged exorbitant fees designed to increase servicing company profits on the backs of hard-working citizens.

re friend’s mortgage:i forgot to explain that the bank had been screwing him with fees and lies about what they had said, and having no record of what they had said… during his efforts to straighten things out with them after he had fallen behind in his parents while he was in the hospital. so…one more time…i do know someting about how banks cheat people. that is not my point here. you hve not said anything about student loans that looks to me different from “normal” banking. even bankruptcy is harder to clear a debt than you seem to think.

i have not been disagreeing with you..until now…i have been asking to for a better (for me) explanation of your case. yelling at me does not help.

There is almost no comparing being screwed on a home mortgage, and being screwed on a federal student loan. There is an order of magnitude of difference.One of dozens of results I could point to to underscore this: Unlike ALL other loans (including government loans), the federal government actually makes a PROFIT- not a loss- on defaulted loans. This was true in 2004. It was true in 2010, and it was true in the most recent White House Budget I looked at.

A credit card company is thrilled to recover 10 cents on the dollar on a defaulted account. The federal government was getting back $1.10-$1.22 on the dollar for defaulted student loans as of 2010. Still today, they get back more than a dollar on the dollar.

https://studentloanjustice.org/defaults-making-money.html

There is a very good reason the Founders called for uniform bankruptcy rights in the Constitution ahead of the power to raise an army and declare war. This is it.

not “parents”, payments.

Mona

I agree with you.

“interest capitalization” sounds better than “interest on interest” but i still think it’s “normal” and at least “understandable”. it’s all that other fraud and abuse that’s the problem.

that, and that, whatever the cause, debt peonage is not good for a country, and is probably immoral. but it is “normal.”

you can argue against it on those grounds, but I don’t think (don’t know) that saying it is different for student loans than for other loans helps your case…unless, of course, it is. but that remains to be demonstrated.

if I am right, your problem (aside from the fraud and abuse) would be to show how interest on interest can lead to evil results, and then show how to avoid those evil results without depriving lenders of the way they make money. because interest is how they make money. and if you don’t pay the interest, you are “forcing” them to lend you more money ..that is, pay the interest you owe them themselves. that won’t work. bankruptcy used to pay the way to put a cap on that…essentially make the banks actually take a loss on “time as money” even though you may already have paid them in interest twice what you borrowed ( about normal for a mortgage, i think).

anyway, I agree with you..even if you think i don’t. just suggesting your argument may need a little fine tuning to be effective on the people you need to affect.

though there are always torches and pitchforks.

Coberly:

This has been explained to you “repeatedly” in the past and here today by myself and the Angry Bears guests who may be mentioned in a reply I wrote. I invited them here just as I did Infidel.

This is a typical practice of yours to hijack a thread feinting a lack of understanding. You, who can explain SS detail to the nth degree can not understand how interest on penalties, consolidation fees, and the resulting interest from those being compounded with more interest.

You are beginning to sound like CoRev and Sammy in their denials or mischaracterizing of anything presented to them.

“If there were penalties, consolidation and recasting fees, interest in forbearance (people do not go into forbearance because they are evading paying, they go into forbearance because they can not make payments) and interest on top of these additional costs; more than likely it has equaled the principal of the loan or a significant amount of it. “

I added the part in parenthesis so as to explain forbearance in case it was difficult for you to again understand. People do not go into forbearance to avoid paying and you have to provide reasons why you need forbearance. If you can not pay, then why the interest as it makes it more difficult.

This was in the post too. You just choose to ignore it and prefer to go off on a tangent.

Run

funny, I don’t remember any of those sins. did you mean”feigning”? If you explained any of it, I missed it. Missed it here, too,

Your “tangent” is the way I go about trying to understand things. Let me try making a clear statement.

Back a few weeks or months or more ago, you said (that is, I think I remember you saying words to the effect) that unlike other loans, student loans charge interest on interest. I said I did not think that was true. i don’t remember you explaining why it was true then or even just yelling at me. Maybe I had just gone off line for the day and not come back. I don’t know. But the thing nagged at me, and I asked my banker how the bank handled overdue interest. He gave me an answer that sounded like you might be right, but I still had my doubts as I cannot imagine anyone not charging interest on overdue interest. I think we may have had this discussion in one form or another again since then.

I don’t know…never thought about it..how the bank handles interest on unpaid penalties or other charges. It seems likely to me.that if for some reason they are prohibited from charging interest on interest (negative amortization? which I never heard of before reader “dweeb” mentioned it here today) they would get around it by charging “late fees” or some such…because that’s the kind of people they are. And they couldn’t imagine just letting you not pay and not pay without charging you interest on the whole amount remaining unpaid, including unpaid interest and penalties and fees.” But I could be wrong. Still waiting for some kind of explanation of that. So far all I hear is yelling.

That does not sound to me like CoRev or Sammy, but if it does, I am truly ashamed.

Well now I feel kind of foolish 😐

Dweeb:

Separately Coberly, Alan and I go back a long way. You are fine. Coberly has a tendency to eat up a lot of bandwidth. You are fine.

I wanted someone else from Student Loan Justice to come to Angry Bear and explain what they have experienced within the student loan system. Both you and Mona did. It is really important to hear from people besides Alan or I.

My children all had student loans. At the time I told them I would sign for parent loans but they would have to help pay them back. They did with the exception of one and he is working on it.

Don’t ever feel foolish at Angry Bear. We appreciate your input.

As well as Christina explained,

long answer to this did not appear. maybe i hit the wrong key.

i think you, Run, mistake my motives. don’t seem to understand that i am not disagreeing with you. just asking for an explanation i can understand.

specifically (at this point) i don’t dispute that student loans do all these bad things, but I am pretty sure i watched wells fargo do all these bad things to my friend who fell behind on his mortgage when he was in hospital;

i did talk to my banker about it, and he sounded like he was agreeing with you, but he wasn’t clear, and i cannot imagine a lender not charging interest on all outstanding debt…including unpaid interest. it may be, as reader “dweeb” seems to be saying, that they are prohibited from it (negative amortization?) if so, i would bet they find ways around it. certainly the extra 20k they charged me when I paid off his mortgage would have covered a lot of interest on interest, but it was called “fees” and i never saw an accounting.

beyond that i agree we are not getting anywhere. that doesn’t sound too much like Sammy or CoRev to me.

Coberly, I am taking you at your word all this conversation is one of good will & you really are trying to get a better picture of what the student loan conversation is about. By that I mean the larger public dialogue in which borrowers are trying to persuade Congress , the President, & public to some degree that we have a serious problem because believe it or not, most prefer not to acknowledge that much less take action to change it.

So looking at your posts and those addressed to you , just a couple of things.1) You seem to ignore much of the content in relies to you. Not sure if why that’s is but you should try up zoom out and look at this from some different angles rather to fixate on one singular aspect . 2) When you see terms and are given back ground information you don’t understand , do some research on-line. These comment sections are just too small to have huge over-arching conversation , at least for me . A quick google search would give you many hits on negative amortization . It’s not a term I invented. I hope this is received as constructive criticism rather than any sort of personal criticism. Speaking for myself at least, if you did some reading in this, it would be much easier to discuss. That’s just my opinion as a new visitor engaging you . Obviously you frequent the blog and have a recognized presence , which is a good thing. It’s nice to have a place engage but it just seems like you are missing a lot of the content being posted.

I have said it a couple of times but you really can’t apply the conventional lending model to student loans & understand the problem but you keep going back to that . Am I wrong ?

Dweeb

yes, i think you may be wrong. but I am also afraid i might be wrong. you describe my missing what others have said to focus too narrowly on my point. that is exactly how i feel about them.

thing is though, that i have made a point of telling them that i agree with what they are saying… except that i have never heard an actual explanation of why they (you?) think other loans do not charge interest on interest. all i get is accusations… as i think you do here… that i am somehow opposed to fixing the student loan problem. i am not, and have said that repeatedly. i pursue the interest on interest…and i think i understood “negative amortization”…. because when i first said it did not agree with my experience, i got no explanation, just yelling.

i have tried to make clear i understand that i cannot apply the conventional model to student loans. i umderstand they are super predatory. but if it is a fact that they are not the only loans which are predatory, and if, specifically “normal” loans do charge interest on interest (compound interest?) then it’s not …i think…good strategy to deny that. on the other hand i also know that “good strategy” in politics appears to make appeals to emotion rather than get picky about facts. i don’t “keep going back” to trying to apply the conventional model, because i never went there in the first place. i just tried to point out there is plenty of abuse in “normal” lending as well, i did not say “as much abuse” only that there is abuse. and i am still not sure about the interest on interest thing… it seemed to me that you were at least partly agreeing with me.

and, in passing, “debt held by the public” is the normal way l see the national debt referred to to mean the public is the lender, and the government is the “debtor” (borrower), so if “technical” use is different than that, it is news to me.

i don’t ignore most of the content in replies to me. i agree with it. and i say i agree with it. they ignore that content in what I say. I am only asking a very specific question and i do not get an answer, only complaints that i am ignoring what they say.

so we have an impasse. i am tired of it.

i thank you for trying to be constructive.

Dweeb

You are always welcome here.

as for banks taking a loss. that should be the risk they assume when making the loan.

somehow we have gone from the government guaranteeing the loan to the goverment guaranteeing that you will pay your pound of flesh.

That about sums it up

Coberly,

Briefly I will try to clarify what I think you are asking then just segue way into what I see as the problem.

No, student loans are not the only loans that allow capitalization of interest or “interest on interest”. Per this article discussion, the borrower holds the debt. I guess conversely the lender would hold the loan. I think the problem is non-financial people using words that mean one thing to them whereas the financial sector has a specific language. It can be confusing.

One other thing to know about student loans is they mainly divide into two eras. The earlier FFEL loan era & the post 2010 Direct loan period. Those loans are managed differently so borrowers from one or the other may describe different problems regarding what they think is the problem. FFEL loan rules allowed interest capitalization more than Direct.

All that said, I don’t think interest capitalization is really a good way to try and describe why student loans are bad faith loans. I would back away from it all and ask why many of the parts of the student loan apparatchik even exists or are allowed. Why are borrowers paying interest on tax per funded loans ? Or more than nominal interest? A bank loans it’s money & can demand a cost (interest) to use its money. The government’s money technically is the taxpayers to start with. More relevant, why exist the arbitrary fees, collection costs, penalties , etc that are fed to third parties servicers? Without the servicers, that money wouldn’t be needed.

The servicer / contractors are principally who ran the balances so high borrowers couldn’t even pay the interest which led to capitalization and negative amortization.

Government implicitly acknowledges the balances are too high to pay off with average incomes by creating IBRs.

Just pay them a chunk of the paycheck 20-25 years and they’ll call it even. The balances will be too high for most at that point to pay off in the time left before death.

All the questions answer themselves once you accept that student loans became an industry for profit into itself for outside investors and other players and serving borrowers educational needs became an afterthought.

Thats why the fox is left guarding the henhouse. Contractors play all kinds of tricks that trigger fees, penalties, & collection costs. The don’t acknowledge communications, lose paperwork, don’t communicate & properly instruct, even push borrowers into default. People in Washington, Wallstreet, universities, etc profit…all of which compromise the servicers, guarantors, & outside lenders / investors to some degree.

The better question to ask than what is wrong with student loans is what is right ?

Which leads me back to what you keep ask, how to sell it ?

I don’t know how to explain this massive fubar in simple concise language that will sell easily.

Dweeb

thank you. i do’t know how to explain why it is that i agree with you , yet Run thinks I am trolling.

Coberly,

precisely.

precisely what?

you think i am trolling, yet i agree with Dweeb?

i could stop eating up a lot of bandwidth right now.

Alan @ 8:29

I think I do understand. And I hope you are right that the “debtors” can refuse to pay without injury to themselves.

You may or may not understand how meaningless bankruptcy can mean to ordinary borrowers anymore. I am about half a million dollars into keeping some of those people in their homes. Doesn’t mean student loan borrowers aren’t treated worse, but banking has been a predatory business at lesst since the last last century. They;\’ve just gotten better at it.

No, you clearly do NOT understand. If you DID understand, you wouldn’t continue to attempt to compare the two. There simply is no comparison.

If what was done to student loans was done to home mortgages, people like your friend (or you) would have your house repossessed, and a debt (probably on par with the value of the house or MORE) would be left on your head. For the rest of your life. And the collection industry would hound you for the rest of your life, trying to seize whatever assets they could find, trying to garnish your wages, and ultimately seizing your social security. Until you die.

Big difference.

Alan:

Yes and very true. Stabenow did not like my questioning her and then interrupting her half way through her dialogue. Old white haired guy will not be picked again at the Garden Party,

Alan @ 9:54

I understood that. a comparison does not imply finding them equal,

I am tired of eating up bandwidth. I am sure your efforts to find justice for student-loan victims will not be impeded by your undersstanding of logic.

Coberly,

Would it not be simpler still just to make state universities tuition free for all residents that qualify for entry? Why borrow money only to fight over repayment issues? Yes, mortgages are different as are car loans. Both have collateral with lender liens on them. Maybe student loans in default just need to sell off the borrower into slavery of some sort? Free public university should be a much easier political sell than load default without recourse for the lender. After all, with no collateral lenders will not make loans if borrowers can just walk away from their debt into bankruptcy or anywhere else.

Ron:

I do not know of anyone who “just” walks away from bankruptcy. Furthermore, private lenders have very little risk. There are conditions before a bankruptcy is granted on a private loan. The loan and interest and lender are at the top of the pecking order by law in being reimbursed. A judge rarely allows someone to walk away unscathed. The same would apply for students who declare bankruptcy.

Guaranteed Student Loans

Ninety-plus% of these loans are funded in this manner. Private equity has very little to lose.2/3rds of the $1.5 trillion are adders on top of the principal which would not be allowed with private loans. The return in productivity by an educated workforce would far surpass the interest being subsidized.

You are making stuff up.

Of course, there is always the maestro of bankruptcies “trump!”

Run,

Freedom is just another word for nothing left to lose. Until I was over thirty years old, then bankruptcy would have just been a walk. People with assets have something to lose. Timing is everything.

Run,

OTOH, I had not realized that only about 8% of all student loans were private, separate from those backed by federal loan guarantee. So, I stand corrected. I guess that Uncle’s cost of backing those loans is far less since there is no bankruptcy protection for the borrowers.

https://www.tateesq.com/learn/student-loan-bankruptcy-law-history

Federal student loans became nondischargeable in bankruptcy proceedings in 1976. Before then, debtors could discharge student loan debt along with most types of consumer debt.

That ended in 1976 when Congress amended the Higher Education Act of 1965.

In Section 439A of the Act, Congress made student loans nondischargeable in bankruptcy unless:

Two years later, Congress passed the Bankruptcy Code. In the years since Congress has retooled the law to further limit a debtor’s ability to file student loan bankruptcy.

But in all those changes, Congress never bothered to define undue hardship. As a result, bankruptcy judges have had to develop their own undue hardship standard tests. Depending on where you live, your judge will use the Brunner test or the totality of the circumstances test.

What year did student loans become nondiscahrgeable?

Student loans first became nondischargeable in bankruptcy in 1976 as part of § 439A Higher Education Act of 1976. Except in cases of undue hardship, Section 439A prohibited debtors from discharging student loan debt until 5 years after the start of the repayment period.

Why are student loans exempt from bankruptcy? Student loans are exempt from bankruptcy because many politicians feared that young people would borrow substantial sums to pay for college and then discharge their student loans in bankruptcy right after graduation. As a result, starting in the early 1970s, Congress began changing the bankruptcy laws to require a borrower to prove undue hardship before she could discharge her student loan debt.

Current Student Loan Bankruptcy Law

Section 523(a)(8) of the U.S. Bankruptcy Code makes student loans exempt from discharge absent undue hardship.

Specifically, 11 U.S.C. § 523(a)(8) says that education debt (a loan or educational benefit overpayment) is exempt from discharge in both Chapter 7 bankruptcy and Chapter 13 bankruptcy if:

Are private student loans exempt from discharge? Private student loans are exempt from discharge in bankruptcy if they are a qualified education loan. A private loan is a qualified education loan if it did not exceed the student’s cost of attendance and the student attended a school eligible to participate in the Federal Student Aid Program…

*

[This would have read a bit differently if it mentioned that 92% of student loans were backed by Uncle, which would make it just one more chapter in Tragedy of the Commons.]

Ron

I had not realized that Run was attacking you for saying something I agreed with. Of course the attack was not quite on point (among several points) and to my mind contradicted what Run had said earlier about what I had said about “normal” loans. But there is no percentage in going in to all that.

It may be (I, criminally it seems, don’t know everything about either normal loans or student loans)… but it may be the “difference” lies in, or arises from the “fact” that student loans are not backed by any collateral that the bank can foreclose on. Just a thought, I know, and criminal in the present environment; we struggle to keep up. The experts on these things are under no requirement to explain their position to the ignorant, even when they are asking the ignorant for support.

Coberly,

No worries mate. I did not realize that I was being attacked either. Of course I only take offense at heavy objects aimed at my head or a gun barrel poked in my face. A liberal blog is about as inoffensive as anything on Earth, next thing to cat videos.

Ron

yes it would. as far as i can tell the current student loan program was passed through a clueless congress by people who saw it as a huge money maker for themselves.

but any comment i offer is responded to by the authorities with suggestions i read the little red book until i get the proper wording correct.

So I am the guy fighting the worst big-government, college-enriching, red-state-wrecking lending scam in US History. You are the guy opposing. Who is the real “communist” in this conversation, buddy?

LOL. At best, you are a fool. If the country every DOES go communist, we’ll have useful idiots like you to thank. Take a bow, comrade, you’ve earned it.

And turn in your conservative card. You’ve lost that.

Coberly,

Yep, there is also a lot of history surrounding how that money maker was assembled. Falling SAT scores in the late 60’s and a series of changes to make the tests easier starting in 1969 were the beginning. Back then tuition for public colleges was lower in general and particularly in CA, where they had previously been tuition free for instate students until about that time. In Virginia, public colleges had no NCAA sports teams, just some intramural sports. Free market thinking stated that students needed skin in the game (i.e., higher tuition fees) in order to get more out of college. Of course, a better solution would have been to raise academic rather than financial entrance requirements for college alongside free public trade schools, but where was the profit in that? America wanted easier schools and more NCAA sports teams and was willing to pay for it. Smart kids were more likely to be bullied than supported. All politicians love people with money since private campaign financing makes people with money essential to getting elected. So, bankers of the world unite became the rallying cry for higher ed, although higher ed was getting lower with the passage of time.

https://time.com/4276222/free-college/

What Happened When American States Tried Providing Tuition-Free College

Ron,

There’s a difference in relatively affordable tuition & the exorbitant debt students began to take on when bankruptcy rights where removed from student loans.Lendersno longer had any skin in the game and opened the faucet on loans for everyone regardless of ability to repay. Lenders weren’t bound by the rules for responsible lending that are generally applied. Why bother when the government guaranteed repayment for irresponsible lending ? Why would schools financial aid offices bother to educate their students on the risks they were taking when student loans where a source of unlimited income for the colleges ? Many have built enormous endowments while students attended their institutions via going in debt. Student loan companies like Sallie Mae even had their people partner with schools & their employees embedded in college financial aid offices including even the Department of Educations FSA. To understand where the costs of college and student debt jumped the shark , you can look around the time when Albert Lord took Sallie Mae from a GSE to private company and Congress began to systematically tighten the noose on students with ever more stringent restrictions on ability to seek bankruptcy relief. State cuts to tuition and building of sports complexes, rationalization that higher costs would make students more committed are more excuses & perks for the greedy special interests that enriched themself’s driving students into inescapable debt. Why inescapable ? Again, because of the removal of bankruptcy relief and ensuing loss of standard consumer protections such as truth-in-lending, statute office limitations , state usury laws, etc. Using free market thinking, colleges would have either eventually capped tuition or gone out of business without unlimited funding from student loans.

To fix the problem Congress must first return bankruptcy protections to borrowers and personally , I think shut this government program down and start over.

Alan

if this is a reply to me:

1) my little red book reference was not meant to refer specifically to communism but to “allowed speech” in general, whether from the right or left or religous cults or anti-religious cults.

2) i never was a conservative, or a liberal, or a moderate.

3) I am not “the guy opposing” you. i am the guy who had some doubts about your choice of words, but I have said repeatedly that I agree that the student loan situation needs to be fixed.

4) your intemperate language, not to say …well, i don’t need to say it…is not the way to win friends and influence people.

5) I still hope you succeed in getting student loan victims the relief they need.

Nonsense. When you invoke the “Little Red Book”, 100% of everyone will assume you are alluding to communism not free speech issues. You know that.

I don’t appreciate the insinuation. Especially given that the truth is 180 degrees opposite.

This is a conservative issue, and but for the bad politics that the student loan swamp as wrapped around it, the republicans would have taken this lending scam to the bath, and drowned it in the tub years or decades ago.

Alan

you put yourself on dangerous ground (mentally) when you assume you know the other person’s thoughts and motives. Especially when you find those thoughts and motives “nonsense.”

I told you what I had in mind. You are sure that 100% of people would know I was referring to communism. Not really. at least half the people are smart enough to know that I was alluding,,,via Mao’s little red book…to the problem of mindless orthodoxy in general.

As for “free speech issues” that really only applies to government. You are not the government. Neither is Bill. You are free to misread anything you want, and to make false assumption, and even delete my comments or block me from the site entirely. The Constitution is silent about that. If anything, it supports the freedom of the man who owns the press to print, or refuse to print, whatever he wants not specifically outlawed by standards of community decency.

This is not a free speech issue. It is mostly a matter of reading competence.

I still hope you can provide student loan victims the relief they need and deserve.

But it is very unlikely I will refer them to you to explain the issue to them, or even answer them coherently without paranoid assumptions about what they know and mean.

As for Bill, if he is listening, here is another allusion: “Kill the pig!” I can’t give a link, but here is a citation: “Lord of the Flies.” Tell me what I am thinking.

You are not thinking . . .

Bill

thanks for letting me know. I thought Alan was so good at telling me what I am thnking that he would be able to spot that right away.

Sorry, but you took the first step onto the slippery slope when you invoked the Little Red Book. And now I see you are doubling down on your previous, nonsensical claim that this alludes to mindless orthodoxy and not communism.

Good luck with that. Take responsibility for the blatant dog whistle you put out. Or don’t. I don’t care. It’s your credibility at stake.

Alan

noted. I’ll be sure to worry about that.

note to an eager audience

the foregoing (forgone?) thread is a little hard to follow due to deleted comments and the inability of “embedded” comments to follow a conversation which is not linear.

I used to think an interested reader could make sense from the gestalt of the thing, but I have been disabused of that idea. the interested reader (that is one with interests to protect) cannot even follow a simple sentence once he suspects it is critical of him and a threat to his (psychic) existence.