Housing and car sales, oh my!

Housing and car sales, oh my!

[If last week was a slow week for economic data, this week is a virtual wasteland until Thursday, so I took yesterday off.]

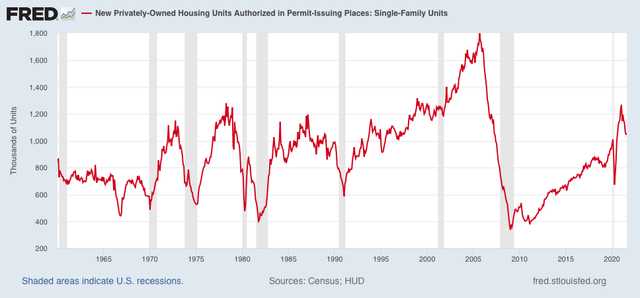

Last month I wrote that typically it has taken at least a 20% decline in housing construction to be consistent with an oncoming recession and that we weren’t there yet.

As of the most recent housing permits report, single-family permits were down 17% from their recent peak:

One of the most persuasive fundamentals-based models of economic cycles, by Prof. Edward Leamer, with decades of proof ever since World War 2, posits that housing is the most leading harbinger, turning down about 7 quarters before a recession, followed by motor vehicles, followed by producer durable goods, followed by consumer durable goods.

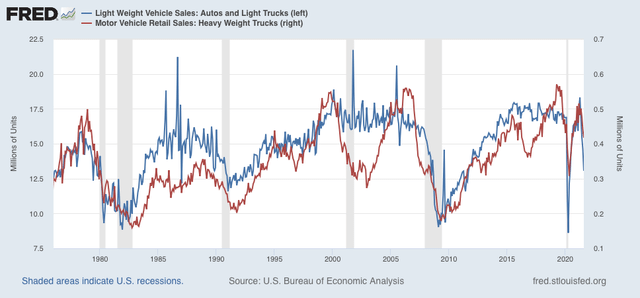

So, the most recent report on motor vehicle sales is not very encouraging. I have stopped following the private manufacturer reports, because most producers have cut back to quarterly rather than monthly reports, so the monthly numbers are mainly estimates. But the BEA issues its own report with a one month delay, and the most recent report for August, just released, showed a decline of over 10% for that month alone, and a total decline of 28% since April (blue in the graph below). Meanwhile, the more leading heavy trucks segment also declined 5% for the month, and a total decline of 19% since March (red):

Outside of the 1970 recession, heavy truck sales have declined at least 23% (and usually much more than that) before a recession began. Light vehicles, including cars, have typically declined at least 10%.

So heavy truck sales have not quite hit the point of being consistent with an oncoming recession, although cars and light trucks have.

It is important to note that our current situation is sui genesis compared with the past 70 years because there has been no significant increase in either short or long term interest rates. Demand remains intact.

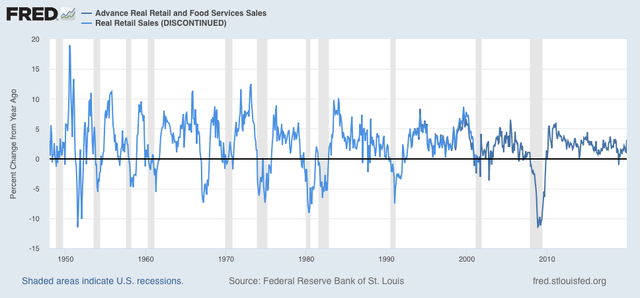

This is entirely a supply bottleneck, which has driven prices for finished goods higher. A close analogy would be the oil shocks of the 1970s, at least one of which was an artificially caused supply shortage (the Arab Oil Embargo). The big difference here is that there is no wage-price inflationary spiral because there are no unions able to obtain automatic “cost of living” wage increases. We have seen wages increase sharply in many places due to the pandemic, but with all emergency benefits ended, that has or shortly will almost certainly cease. If the supply shortages do not ease shortly, then the next thing to watch out for is whether more broad durable goods spending by both producers and consumers stalls. In particular, real retail sales per capita has almost always turned negative YoY shortly before the onset of recessions in the past 70 years:

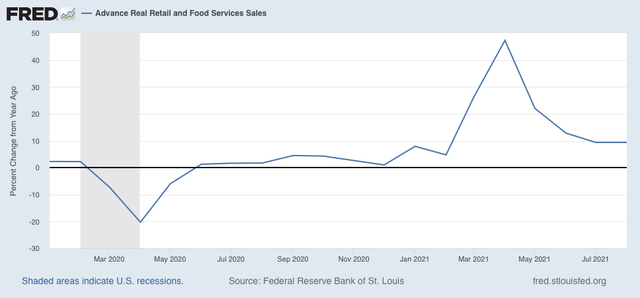

By contrast, at present YoY real retail sales are up almost 10%:

If that number were to suddenly plummet close to 0, I would be much more concerned that the supply bottleneck was on the verge of creating a recession.

We are planning to replace our 2007 Audi A3 with a VW ID.4 Pro S AWD.

We “reserved” one today with a $100 deposit. And, were quoted June 2022 delivery.

db:

Did you tell them it does not take that long to build your vehicle? And then did you ask them what they are doing to resolve any inventory or throughput issues? Longer lead times do not solve the issues and instead they make them worse.

I see this in home building too which is far less capable than VW or Audi in manufacturing. I am waiting for the delivery of cabinets to finish a home. Today, we run out there to see if they arrived as the sales-twerp has not called us to inform us. I would rather see for myself and not say a word to him.

I would love to see the Japanese enter the single home manufacturing business, It would put American companies such as Meritage, Fulton, etc. out of business. The lack of planning throughput is “very” apparent in housing manufacturing. It is a cluster-f*ck. Rather than fix the issues and improving what they can impact today and quit using the EXCUSE of supply chain issues when they can not detail of what the damn supply chain consists.

I asked the young (30s) sales person for a pro-number and the response was silence. He did not know what the meaning of a pro number. I asked how the shipment was coming, via boat, truck, and whether it was international or domestic. He claimed they spent $thousands to get these cabinets. I asked about the construct of the cabinets or whether this was expedite (sigh) costs (to bust in line) or maybe additional freight costs. He did not know.

As my Japanese a*s of a boss would tell me while pointing a crooked finger at me (we always looked at it), “you should know this detail.” The Germans I could fluster with pushback from my knowledge.

My point is; all of the supply chain complaints are little more than an excuse for doing nothing but take in the money from doing “nothing” other than ride the profitability curve of excuses doing nothing.

Similar occurred in 2009/2010. Automotive shut down and canceled all of their orders for chips. Rather than grow wafers, the Panasonics, OnSemis, NXPs, Infineons, etc. did similar.

We are heading for a recession caused by supply chain issues.