Initial jobless claims: still elevated compared with several months ago, another negative jobs report for January a possibility

Initial jobless claims: still elevated compared with several months ago, another negative jobs report for January a possibility

Initial jobless claims this week came within a hair of meeting my criteria for a change to an upward trend.

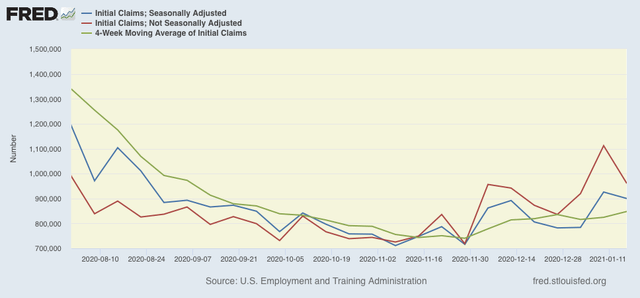

On a unadjusted basis, new jobless claims declined by 151,303 to 960,668. Seasonally adjusted claims also declined by 26,000 to 900,000 (last week’s numbers were also adjusted downward from 965,000 to 926,000). The 4 week moving average, however, rose by 23,500 to 848,000.

Here is the close up since the end of July (these numbers were in the range of 5 to 7 million at their worst in early April):

There is now a 2 1/2 month trend of YoY% increases in initial claims. Further, by rising to 900,000 or higher for the second week in a row, seasonally adjusted claims hit one of my two markers for a fundamental change of trend. But the 4 week average – by a whopping 2,000 – remains under my marker of 850,000.

Why I’m still waiting at least one more week for confirmation can be seen in my next graph.

For the last couple of months, I have been cautioning that the holiday season plays havoc with seasonality even in normal years, let alone a year when the pandemic is causing changes in weekly numbers by an order of magnitude. Typically in the weeks after Christmas and New Years’, claims go up by 25,000 to 50,000 on an unadjusted basis, and then rapidly recede. This year claims both went up and then this week came down by up to 10x as much during this period.

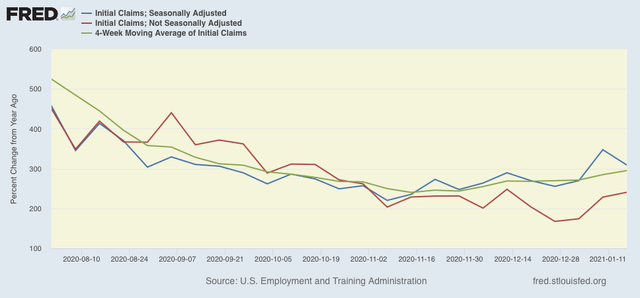

But when we look at the YoY% change in all of the above metrics, which washes out those outsized seasonal affects, the picture – especially in the critical, non-seasonally adjusted data – is not so negative:

While weekly seasonally adjusted claims have risen 310% – a YoY comparison last seen in August, the 4 week average is still in the YoY range they were in October, at +240%. Further, the the non-seasonal trend, at a 240% increase YoY, looks like a sideways rather than upward trend. If this changes next week, when it looks almost certain the 4 week average will exceed 850,000, then we’ll definitely know we are in an upward trend. But I’m giving it that one more week.

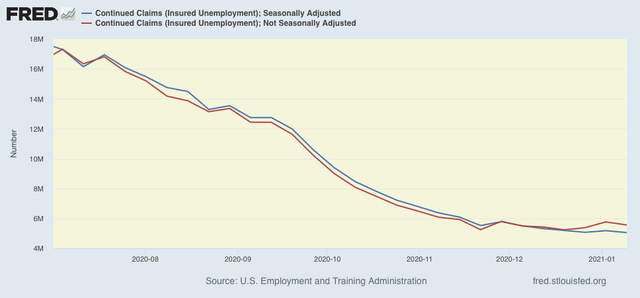

Turning to seasonally and non-seasonally adjusted continuing claims, which historically lag initial claims typically by a few weeks to several months, the former declined by 127,000 to a new pandemic low of 5,054,000, while the latter declined by 203,750 to 5,563,048:

Because of these lag initial claims, I have suspected that we would see an upward reversal. Last week I wrote that it appeared to have arrived, but with the new pandemic low in adjusted claims, that is on hold.

As I usually note, a reminder that both initial and continued claims remain at or above their worst levels from the Great Recession.

Finally, because the past two weeks have been about 50,000 higher than the conquerable two weeks last month, it appears more likely than not that we will see another slightly negative jobs report for January when it is reported in two weeks.

As I wrote last week, renewed partial lockdowns and increased consumer caution due to the out of control pandemic have caused increased layoffs. At the same time, it isn’t quite as bad as I would have thought several months ago. Already in his first day in office, Joe Biden has begun to tackle COVID in a far more forceful, cohesive manner. With increased federal authority behind mask-wearing and organized vaccination programs with the States, together with the invocation of the Defense Procurement Act for both N95 mask and vaccine production, hopefully, we will see a decisive downward trend in the pandemic by the spring equinox.