A Dog that Didn’t Bark

The USA is about to experience the largest fiscal policy shift since World War II. The House is debating whether to add $ 2,200,000,000,000 to the Federal Budget Deficit (counting loans as if they were expenses because that’s what they do). There appears to be a near consensus as all are speaking in favor. It is just possible to guess which are Republicans

I’m sure there is a similar near consensus that Rep Thomas Masie of Kentucky, who made them fly to DC by threatening to call a quorum, is a jerk (the Rep. is short for reprehensible). I don’t really wonder if someone is going to get knifed in the members only men’s room.

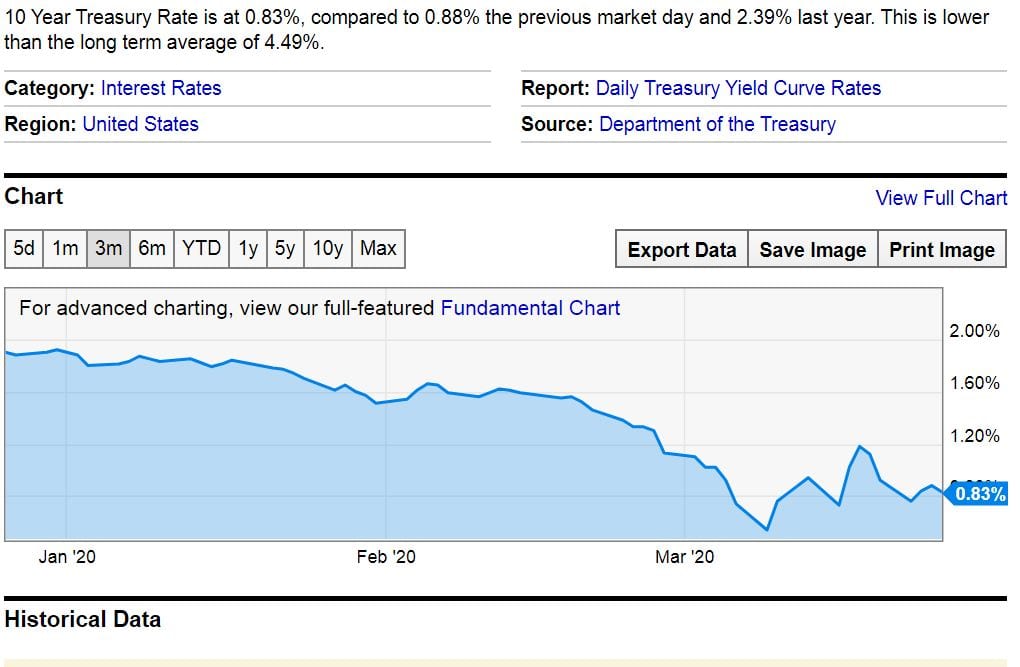

The Supply of Treasury securities is about to experience the largest shock in history. So what is happening to the price in anticipation of the huge supply shock ?

Quick find the shift from arguing about $ 2.5 billion vs 8.5 billion to arguing about $ 100 billion more to discussing $ 1800 billion more to approving $ 2200 billion more on the graph.

The rate is not quite at the all time record low, but it is close. One might argue that a huge Federal Debt will crowd out investment, beause it will create an illusion of wealth which makes people consumer more so the Fed will have to achieve high real interest rates in order to keep the economy from overheating. One can argue that the huge debt will cause high inflation (perhaps because the Federal Government is the world’s main dollar debtor and can make the dollar worth as little as they want) which will imply high nominal interest rates.

But one will not be able to convince investors of this. the invisible bond vigilantes clearly have got their hands on Harry Potter’s invisibility cloak.

This isn’t even a matter of much debate (except for Massie). It is clear that stimulus will help the USA and also, in particular, the GOP. When the interests of the USA and the GOP allign there is (almost) no debate, because Democrats care about the country and not just about hurting the other party. In 2009 Republicans demonstrated that they were partisans not patriots. Today, Democrats are demonstrating they are patriots more than they are partisans.

Many economists (some winners of the Nobel memorial prize) should admit that they were totally wrong. But of course they won’t.

Some economists whose response to the horrible Trump tax cut was more debt no problem can say “I told you so”

I told you so.

It is a poor ‘stimulus’. It also isn’t 2.2 trliion. It’s simply a made up number. Nor do interest rates matter now. The GOP will be helped little.

I didn’t have to look to know Massie is a libertarian.

As previously mentioned, I cannot wait until all of them are gone from the face of the earth. By natural causes of course, all because the Feds screwed up pandemic control, which would be nice.

Massie wants a rentier dictatorship. But whoop. Delaying this waste of a bill is no sin. It simply as Joe Biden said, is really not that good piece of legislation.

Suppliers are going to be the real tragic story this go around.

Honestly, Massie should be ejected from the House both for endangering the country and the other House members.

Correct me if I’m wrong, but can’t crowding out only occur in an open market with bidders of limited resources? If the Fed simply buys up and makes the debt disappear, then there is no crowding out.

BTW was there any adjustment to the debt ceiling, or are we going to be up against that farce again soon?

Rates for the US government are not low. Take total debt (include social security fund obligations) divide that into interest expanse an get about 2.5%.

Our ‘stimulus’ is not a surprise, it is a regularly scheduled eight year event in which we correct funding errors. The rate we pay for those corrections is always higher, as you will not looking at the ten year rate since 1980. We always end up carrying yesterday’s high interest rates for lower inflation and growth today. There has never been a time since 1980 when interest rates were low for government. Look closely r > g always for the ten year rate which government pays.

Second, this is not a sudden stop in demand, this was a volutary shutdown of supply, a consensus shutdown in which all parties new the cost at the time and were prepared to suffer the cost. So there is absoluytely no cost shifting going on, the so called free seignirorage is, right now, raising retail banking fees and bank are planning to accelerate the roll up of the retail banking sector.

This is a regularly scheduled bailout, I have been watching this since 1980, and we always repeat the same mantra and always repeat the bailout sequence and always expense it, mainly taking the middle class. And we always lie, 100 percent of the time, we drag out Krugman and he tells us interest rates are low; and interest rates have never been low for government. The lie causes us to repeat the sequence over and over again, I count five times since 1980.

I have a test.

Look at the ten year Treasury rate since 1980. Follow the track before each of the scheduled recessions all the way top mid 2019. We see the ten year peak at 3.2% and drop continuously, before the virus. It took a final drop from 1.5 to .8 %, and we are in recession. Absent the virus, this is exactly what the chart predicted anyway. This is exactly like the sudden stop of all the past recessions we have had.

Remember we are repeating all the same hyperbole that we repeated during 2008, the rhetoric has not changed. What has changed is the volatility, each recession almost doubling the national debt. At the end of this recession, the ten year will be about 1%, peak at some 1.5% in 2025, and we will enter our third recession since 2008 right on schedule.

This is not stopping, it is in the structure of government and having economists run around and tell us that Godot has arrived, for the umpteenth time, does not help.

This dog barks:

https://www.npr.org/2018/01/09/576669311/hidden-brain-great-recession-deaths

SHANKAR VEDANTAM, BYLINE: Hey, David.

GREENE: So recessions can be good in some ways?

VEDANTAM: In some ways, David, recessions seem to change the mortality rate, and not in the direction you might expect. I was speaking with the economist Erin Strumpf at McGill University. Along with Thomas Charters, Sam Harper and Ari Nandi, she studied the effect of the Great Recession a decade ago by looking at 366 metropolitan areas in the United States, which cover about 80 percent of the U.S. population.

ERIN STRUMPF: We find that in areas where the unemployment rate is growing faster, mortality rates decline faster. So during the Great Recession in the U.S., we saw increases in the unemployment rate of about 4-5 percentage points, so that translates to about 50,000 to 60,000 fewer deaths per year, the same order of magnitude as the number of people who die from influenza and pneumonia every year.

—-

OK, unexpected. We can discount 60,000 deaths, maybe more because they were saved by the expected recession. Right now we have a thousand deaths over one quarter, phase one deaths. So the goal is to have our regularly scheduled recession, get our favorite welfare checks boosted and keep total deaths from virus below 60,000; and we break even.

Right now the plan remains, do a sudden stop every eight years and get our welfare checks a boost. We have our sudden stop, right on schedule. Our checks are in the mail, now keep the virus death rate below 60,000 and we break even. The virus thus becomes our perfect excuse to pontificate on why ‘This time is different’.

Hi, very nice article. I really appreciate it. You have touched upon a very important and relevant topic for today. Thank you for sharing your professional knowledge. Now you have one regular visitor to your site for new topics.

Darina:

Welcome to Angry Bear. First time commenters and comments always go to moderation to allow us to weed out spam, spammers, and advertising. You are set!