Surprise Billing To Be Resolved in February 2020 to be Enacted in 2022

I had wondered why the Senate (Schumer) had backed off on legislation controlling surprise billing. It turns out there is a House bill also and I am sure they are going back and forth on this. Recently, two bills have emerged in the House and one from the Senate. Medscape, “House Committees Advance Bills to Address Surprise Billing.”

Of course if Congress’s butt was on the line, a solution would have been found quickly and enacted in 2020. At the end, see which one I would back.

The House Ways and Means Committee bill passed by a voice vote bipartisan bill. It seeks to establish more use of third-party negotiators ( arbitration) for settling certain disputes about payment for out-of-network care. This bill has the support of the American Hospital Association and the American College of Emergency Physicians. The American Medical Association also praised the committee’s reliance on mediation for disputes on bills.

The House Education and Labor Committee advanced a hybrid proposal seeking to use established prices in local markets to resolve many disputes about out-of-network bills. Key to this bill is the use of arbitration above a certain cost. Bills greater than $750 or in the case of air ambulance services $25,000; clinicians and insurers could turn to arbitration for an independent dispute resolution. House Education and Labor passed this bill in a 32-13 mixed vote with some Republicans and Democrats opposing and in favor.

The latest Senate Health, Education, Labor and Pensions (HELP) Committee of legislative proposals also addresses surprise medical billing. The HELP bill called for mandating that insurers reimburse out-of-network costs on the basis of their own median rates for in-network providers.

The Education and Labor Committee bill is estimated to save $24 billion, the Senate HELPS bill is estimated to save $25 billion, and the Ways and Means’ bill would save almost $18 billion all over 10 years. It is suggested the greater use of arbitration in the Ways and Means’ bill will result in less savings.

Read on about the private equity involved and providers.

Outside Opponents of Legislation

The American Hospital Association: “Setting a rate in statute gives insurers few incentives to develop robust networks with hospitals and physicians, and paying for emergency care at the median in-network rate would surely underpay for these services and create an incentive for insurers to avoid paying fair reimbursement for these services. This approach is an obvious windfall for the insurance industry without any assurance that health plans will pass these savings on to consumers through lower premiums.”

Other physician organizations have joined the fight to make balance billing appropriate; the American College of Emergency Physicians, Envision Healthcare, US Acute Care Solutions and US Anesthesia Partners — gave roughly $1.1 million in 2019 to members of Congress, according to a Kaiser Health News analysis of Federal Election Commission records.

Doctor Patient Unity: “We support a federal solution to surprise medical bills that makes insurance companies pay their fair share and supports patients’ right to quality medical care.”

“We oppose insurance-industry-backed proposals for government rate setting that will lead to doctor shortages, hospital closures and loss of access to medical care, particularly in rural and underserved communities.”

Early on in 2019, Doctor Patient Unity spent more than $28 million on ads opposing legislation without disclosing its staff or its funders. It was later revealed its largest financial backers are two private equity backed firms Team Health and Envision Healthcare. Together they own physician practices and staff emergency rooms around the country according to spokesperson Greg Blair. Blackstone Group owns Team Health and KKR owns Envision Healthcare

As is typical of political ads being run to influence people, they do not tell the whole story and omit references to surprise bills. Instead, they warn of “government rate setting” harming patient care and doctor/patient relationships.

The Direct Providers

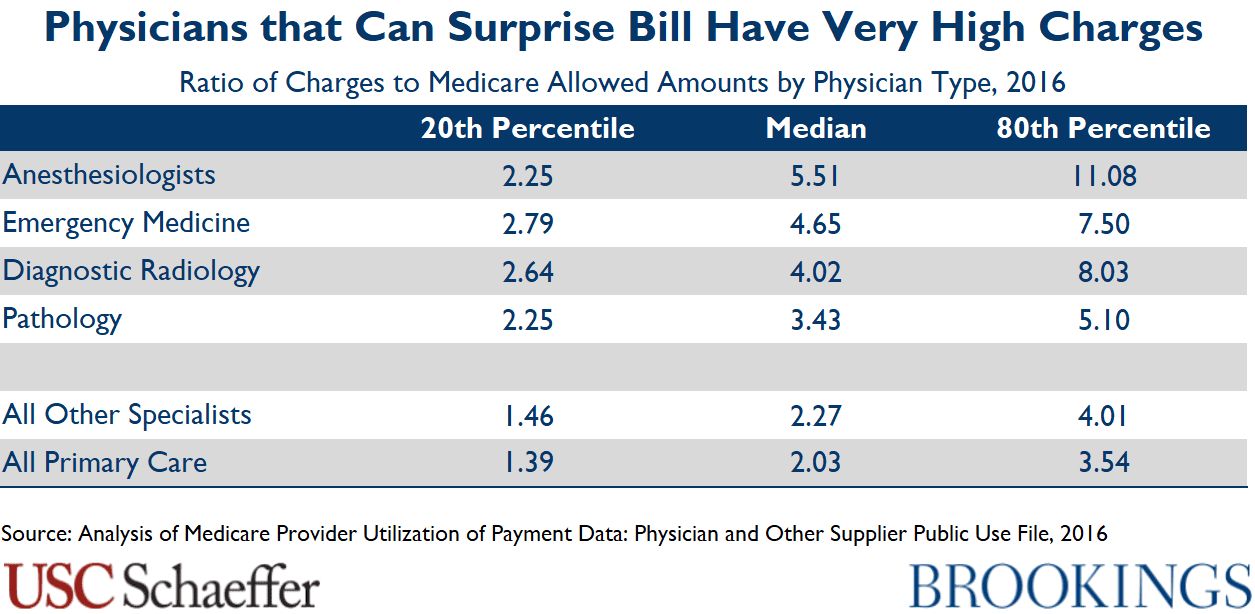

ER doctors, anesthesiologists, radiologists and other specialists who typically charge out-of-network prices are among the highest-compensated practitioners. I have found this to be true during my hospital visits. Doctors, 3rd party contracting companies, and hospitals complain Healthcare Insurance Companies have the upper hand due to size and can pay the increased costs of out-of-network pricing.

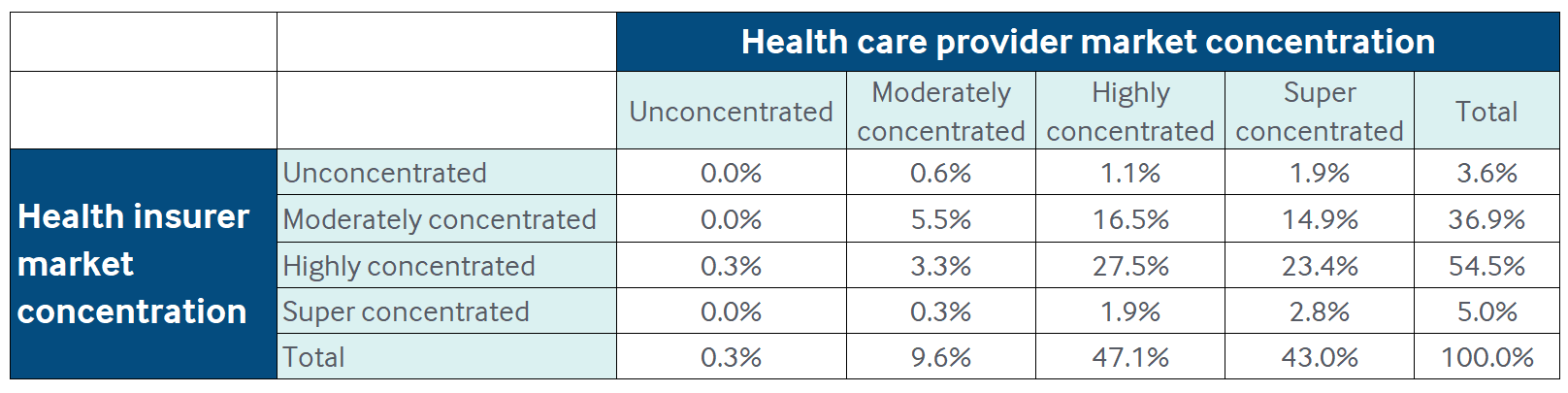

The argument by doctors, the 3rd party contracting companies, and hospitals has been made the healthcare insurance companies control the market and are able to secure better pricing from providers which is not passed along to the insured. In markets where both providers and insurers are highly concentrated, insurers have bargaining power to reduce prices for hospital admissions and visits to certain physician specialists. The Market Concentration chart for insurers and providers reveals the concentration (concentration chart) for providers is greater than it is for insurers overall. Furthermore and if we are talking about ACA policies, additional moneys gained must be used for treatment or the excess beyond 15 and 20% overhead and profit is refundable. It can be said also, when the total cost goes up, the portion (15 or 20%) of the total price increases in real dollars.

ER doctors, anesthesiologists, radiologists and other specialists who typically charge out-of-network prices are among the highest-compensated practitioners. I have found this to be true during my hospital visits. If the insurance company can not convince them to take a lesser rate, you are stuck will the bill. I have been tempted to ask at the time of need whether they are all in network and employees of the facility I am visiting that day. Countering the argument by insurance, doctors, and hospitals complain healthcare insurance companies have the upper hand due to size and market control and can pay the increased costs of out-of-network pricing. As shown chart 1, their claims are not precisely true and the market for healthcare has become less competitive as hospitals and ACOs buy up the competition.

ER doctors, anesthesiologists, radiologists and other specialists who typically charge out-of-network prices are among the highest-compensated practitioners. I have found this to be true during my hospital visits. If the insurance company can not convince them to take a lesser rate, you are stuck will the bill. I have been tempted to ask at the time of need whether they are all in network and employees of the facility I am visiting that day. Countering the argument by insurance, doctors, and hospitals complain healthcare insurance companies have the upper hand due to size and market control and can pay the increased costs of out-of-network pricing. As shown chart 1, their claims are not precisely true and the market for healthcare has become less competitive as hospitals and ACOs buy up the competition.

“Providers are more concentrated than insurers in almost 60 percent of US metro areas. Health plans hold an edge in only 6 percent of local markets. National and state level studies reveal a steady rise in concentration among specialist physicians, primary care providers, and hospitals alike. As Brent D. Fulton notes, concentration of insurers fell slightly from 2010 to 2016, while concentration rose for both specialist physicians and hospitals. The evidence suggests provider organizations will retain significant bargaining leverage even after out-of-network billing reform, leaving little scope or incentive or capability for insurers to push prices down sharply. ”

Meanwhile, the naysayers are battling constructive resolution with $millions in countering ads and intense lobbying of Congress to delay and/or deny resolution of overpriced surprised billing of patients of which had no choice, many more are still being hit with bills there is little explanation for except greed. We do need Single Payer. Nough said . . .

Congress has till February 22nd to resolve the deadlock before the current temporary bill expires. I would take the Education and Labor approach, which is also backed by the House Energy and Commerce Committee, and the Senate Health Committee. It would set the payment rate based on the median amount paid for that service in the geographic area with the option of going to arbitration for some higher-cost bills. It result in greater savings.

We (anesthesiology) are par with everything that our network accepts. I am not a fan of surprise billing, but I dont think you grasp all of the issues here. Medicare reimburses at much lower rates than does private insurance in my specialty. If you work in a place with a high percentage of Medicare (or Medicaid which is worse) like we do, you cannot come close to earning market salaries. So we, many years ago, ended up working 95th percentile or worse hours (over 70 per week) while earning in the 15th-20th percentile in income. We lost a lot of staff. The hospital had to make up the difference so that we could hire and retain people. We were fortunate that our hospital had the resources to do that.

Up north of us another hospital faced a similar situation, but they didnt have the resources to subsidize their staff. So they fired a good team and brought in another. Told them it was OK to not bill in accordance with what the hospital accepted, like the prior group did. That let the new group earn enough, for a while, to hire and retain people. Hospital eventually failed anyway and had to be bought out.

I think most of the groups that I know are surprise billing are pretty greedy and sleazy, so I stay away from them. However, there are other cases where groups are in a tough situation and pretty desperate. Especially smaller rural hospitals that have trouble finding staff to begin with.

Steve

Steve:

“I don’t think you grasp all of the issues here.”

Have you clicked on the links at all, which are in this commentary? They are from MedPage or Medscape (which ever one I chose), Health Affairs, Commonwealth Fund, etc. I did not look at Fierce Healthcare or Public Citizen. I did look at the New York Times and the NEJM https://www.nejm.org/doi/full/10.1056/NEJMp1916443?query=TOC . I have been writing on healthcare since 2007 and also did a lot of editing for Maggie Mahar. Granted I was never a doctor; but I worked for Baxter planning pills, ointments, Dialysis liquid, and helped bring about CD & CF Dialyzers, Bubble Oxygenators. When I started working in 74, I was making $11,000. In 1982 after attaining my Masters in Economics. I was at $33,000. I did not see six digit in a regular salary till the 2000s. No OT pay either or time and a half. So yeah, I understand what it is to struggle with a wife and three kids at home. I traveled to other countries on weekends and worked my 10-12 hour days.

Rural hospitals are a different and pressing issue. I did not address that here. Mayo closed its rural hospital and brought the services in to the main facility. So much for ACOs giving a sh*t about rural when they can afford to do so. The biggest impact on health insurance premiums is from in patient and out patient costs (2007-2014). 60% of the issue was “just” pricing. Doctors had a 7% increase during that time period as measured against 42 and 25% out and in. Much of the surprise billing issue is driven by Blackstone and KKR who are squeezing the blood out of the two 3rd party companies until they get their $dollars back and then they will tell them goodbye.

No one said anything about paying Medicare Rates even though somewhere in the stuff I read, PCPs are making 139% Medicare rates. I am sympathetic; but, I do not agree when 1 out of five bills are surprise billings (NEJM, etc.).

I am glad you did respond though. Thank you.

Bill

Steve:

As one expert on Single Payer said to me; “why do we have networks?”

Run75441,

You are doing an important service to the community covering this important topic. Thank you !

likbez, I agree with you.

This is going to be an epic battle, with lobbyists descending like locusts on a wheat field.

Blackstone Group owns Team Health and KKR owns Envision Healthcare and they funded Doctor Patient Unity. Then there is American College of Emergency Physicians, US Acute Care Solutions and US Anesthesia Partners who together gave roughly $1.1 million in 2019 to members of Congress. Envision and Team are up to their necks in debt after being bought by venture capitalists.