Housing: BOOM!

Housing: BOOM!

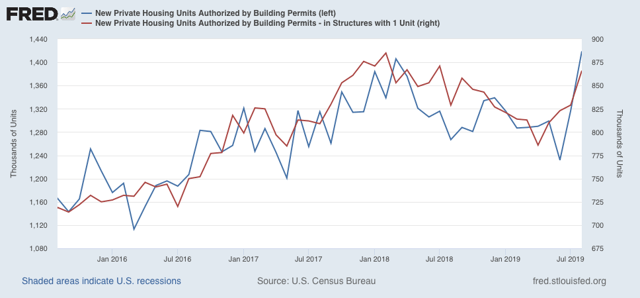

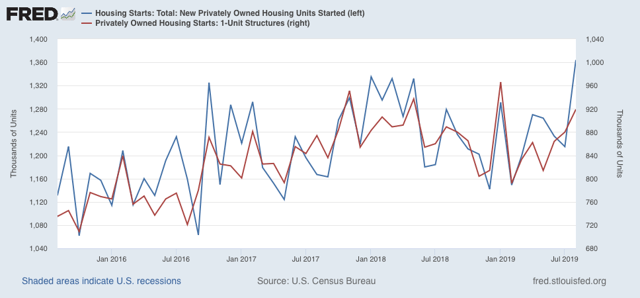

Well, this is an easy post. This morning’s report (Wed.) on housing permits and starts showed new expansion highs in both overall permits and starts. The less volatile single family segment also recovered, with both single family permits and starts at one year highs, although slightly below their expansion peaks.

Here are total and single family permits:

And here are total and single family starts:

The housing downturn is over. As expected, lower interest rates for the past eight months have shown up in the housing data in spades.

This has major implications for the index of leading indicators this month, which can be expected to pop. And since housing permits are a long leading indicator, this, along with new expansion lows in corporate bond yields, new highs in per capita real retail sales, renewed increases in real money supply, and continuing looseness in credit conditions, means that the only negative long leading indicator is the partially inverted yield curve, and the only mixed or neutral indicator is corporate profits. In short, the latter part of next year is shaping up to be quite positive.

In the immediate term, I wonder if this takes the pressure off the Fed to lower interest rates. If you are a Democrat, don’t hang your hat on there being a recession on Election Day next year (although “Tariff Man” may yet come through!).

You do realize that happened in 2000-2001 as well right????

Let me also say this is another tariff stocking demand push foward. Without the “trade war”, interest rates are higher both in nominal and real terms. Your exhausting demand new deal. Remember last December new deal. That was only partially from the shutdown……The trade war went through a pause and we saw signs of the 2018 demand push on retail sales.

NDD starts with “This morning’s report (Wed.) on housing permits and starts showed new expansion highs in both overall permits and starts.”

So Bert comments “You do realize that happened in 2000-2001 as well right????”

Hey Bert – check with FRED. Housing permits were basically flat back in 2000 and 2001. Lord – do you ALWAYS get EVERYTHING wrong or what?

Bert:

While you are correct that 2000-01 is the closest analog prior to recessions, there are two crucial differences:

1. Consumer inflation rose from about 1.5% to just under 4%. The Fed was not in a position to lower rates.

2. Corporate profits declined almost 12% from recent peak, and the ISM manufacturing index fell to 42 or lower, vs. a decline of only about 4% from peak, and an ISM manufacturing index at roughly 50 now.

Despite the trade war, the producer side of the economy isn’t hurting so much – so far – as it was in 2001.

The problem with that is, real corporate profits are behaving EXACTLY like that period. Overcapacity, corporate debt exhaustion and lets note, JUNK corporate bond yields have risen almost to 3% too a new decade high making a key driver of this cycle harder than ever to borrow.

This is why Trump whines over rates despite the elevated housing prices. He wants another FIRE bubble to replace these cyclical factors, as loan quality has crumbled this year to unworthy borrowers.

My guess real corporate profits will be down 25+% by next spring that is instant recession. Fixed nonresidential investment will contract solidly and head counts will be reduced, leveling off your housing cheerleading.

New Deal, I expect better of you in analysis. Don’t fall for the fraud.

Bert:

You just got some friendly advise.

OK you were talking about data other than what NDD provided. Try making yourself clearer next time. On this:

“JUNK corporate bond yields have risen almost to 3% too a new decade high making a key driver of this cycle harder than ever to borrow.”

Am I reading your sentence right as a 3% interest rate would be low for JUNK (JUNK I tell you) corporate bonds. Again – you provide NO data to back up what seems to be a bogus claim so permit me:

https://fred.stlouisfed.org/series/BAMLH0A2HYBEY

ICE BofAML US High Yield B Effective Yield

This rate may be 5.8% but it has recently been a lot higher.

Come on Bert – stop lecturing NDD like this:

“I expect better of you in analysis.”

Your comments universally SUCK in terms of analysis. Learn to write and learn how to do even basic research. DAMN!