Real retail sales very positive; industrial production decent

Real retail sales very positive; industrial production decent

Real retail sales for November, together with the revisions for October, were very positive.

While November sales, both nominally and adjusted for inflation, increased +0.2%, October sales were revised upward to a nominal +1.1%. On an inflation adjusted basis, that translates to +0.8%.

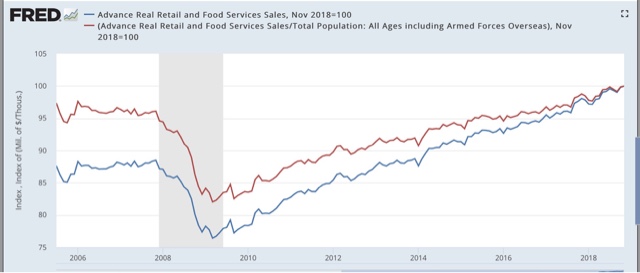

As a result, as of November both real retail sales and real retail sales per capita set new records:

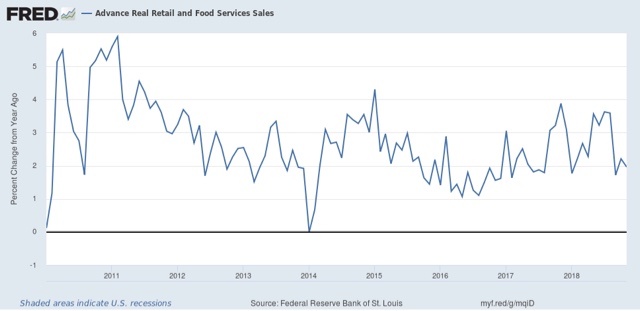

The latter has turned negative more than one year before both of the last two recessions, and so supports the case for no recession in 2019. The former, on a YoY% basis, tends to be a decent if noisy short leading indicator for employment. Here what YoY growth in real retail sales looks like:

About the least positive thing you can say about this morning’s report is that, even with the upward revision to October, real retail sales appear to have downshifted from their earlier strength, as the strong +1.7% real gain from September 2017 drops out of the comparison. This suggests continued positive employment reports in the next few months, but maybe not at the 200,000+ levels of a few months ago.

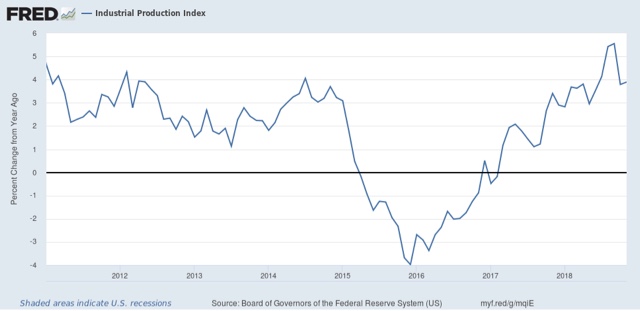

Meanwhile, November industrial production increased +0.6%, but October was revised downward by -0.3%, so the net result was a +0.3% gain. On a YoY basis, industrial production has also decelerated from a “boom” readings to decently positive ones:

Together, these two reports this morning say that the nowcast remains very good.

Your October data is wrong. Your also wrong on the early 2000’s slowdown. Recession in 2019, likely late in the year.

To expand my points.

1.exhurricane spending knocks real retail sales down to .5% increase and 0% respectively. September was negative. This excess will have to come off this winter like last winter.

2.1999 spending was the greatest spending boom this generation. YrY declines don’t mean much. It wasn’t until 6-8 months before March 2001 that spending turned really down. Asset bubbles blow up spending, abnormally.

3.This expansion is just a long winded debt cycle with far less bubble, but debt servicing is debt servicing. This is why Mr market is groaning…in real time. 2019 will feature personal and corporate slowdowns in debt expansion, which is always fatal.

he also set a very low bar for “decent’ industrial production….November’s gain was mostly about a jump in utility production due to cold weather…

manufacturing production was flat, after October manufacturing was revised 0.5% lower..