Americans Raid 401(k)s

Angry Bear has carried posts on this issue over the years. 1. 2008 and draining the 401k pool of money, 2. Draining 401ks, 3. 401k and Social Security, 4.. Kenneth Thomas and retirements money (Links), 5. A 1000/mo pension equals 300,000 in savings among others.

Yves Smith at Naked Capitalism makes an impassioned statement. (Re-posted with permission)

Americans Raid 401(k)s, Replacing Home Equity Withdrawals as Way to Make Ends Meet

It’s been creepy to see economists and the financial media cheering the re-levering by American households as a sign that they economy is on the mend and consumers are regaining their will to shop. But ordinary Americans took huge balance sheet hits in the crisis: the loss of home equity, which only in some markets has come all the way back; job losses and pay and hours reductions, which led many to run down savings as they readjusted; declines in stock market portfolios; lower income thanks to ZIRP for retirees and other income-oriented investors.

While the top wealthy are borrowing, in contrast to the behavior of the rich predecessors, on the other end of the spectrum, many are still struggling for survival. The latest job report showed that the number of long-term unemployed, reflected in the level of people who’ve given up looking for work and are counted as no longer in the workforce, only continues to rise. Food stamps and extended unemployment benefits have been cut. And with soup kitchens under stress too, one wonders how people who are in such dire financial straits manage to get by.

Before the crisis, if someone was hit with a financial emergency, like an accident or sudden job loss, those who had houses could often draw on home equity. With that piggybank depleted or non-existent, the last-ditch financial fallback is accessing retirement savings.

Now admittedly, this does not necessarily take the form of partial or full liquidation of a 401 (k). Some plans allow for borrowing against 401 (k) assets, but it’s no free lunch. Borrowing is limited to a maximum of half of plan assets or $50,000, whichever is lower. While the borrowing is interest free, the funds need to be repaid in five years. If someone is already under economic stress, what do you think the odds are that he will be able to repay the loan, particularly since it comes out of after-tax dollars?

And the alternative is even more costly. Withdrawing money from a 401 (k) before age 59 1/2 incurs a 10% penalty. On top of that, the taxpayer also has to pay income taxes on the withdrawal.

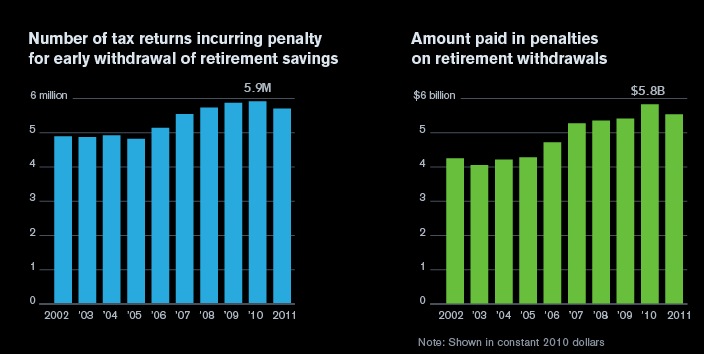

A Bloomberg story gives the sobering details of how prevalent 401 (k) withdrawals have become. For the latest year in which data is available, 2011, 4% of all households paid early withdrawal penalties. A Federal Reserve study found that 9.3% of taxpayers with retirement accounts paid early withdrawal penalties, an increase from 7.9% in 2004.

Admittedly, a Bloomberg graphic shows that the amount of penalties was slightly lower in 2011 than 2010. But the fact that it’s higher than the levels seen during the financial crisis years shows that economic stress is still high (click to enlarge):

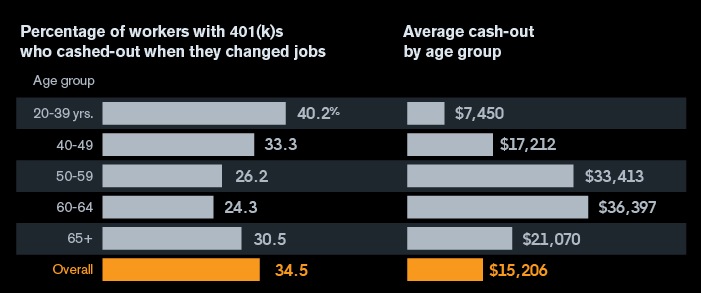

The article points out that one-third cashed out their 401 (k)s when they changed jobs, which they argue shows that many workers, particularly the young, don’t appreciate the true cost of early withdrawal. But I suspect the picture is more complicated. One of the few ways you can escape early withdrawal penalties is a first-time home purchase; at least a portion of the younger individuals may be buying a home. Conversely, others may need to pull money out simply to finance a move.

It’s also worth comparing the magnitude of these withdrawals to median 401 (k) balances: $24,000 overall, and $65,300 for those over 55 (click to enlarge):

Some excerpts from the Bloomberg article:

Adjusted for inflation, the government collects 37 percent more money from early-withdrawal penalties than it did in 2003. Meanwhile, the amount of home-equity loans outstanding was $704 billion in 2013, down 38 percent from the 2007 peak, according to Federal Reserve data.

“They didn’t have access to the home equity that they had in the past,” [Reid] Cramer [of the New America Foundation] said. “And families looked around for what was left and they actually drained the value from the 401(k).”

The article discusses the divergent policy views: make it easier for people to access their retirement accounts, recognizing that they may be under duress, or make it harder to force them to keep their savings intact. Of course, you don’t hear any mention of the notion that what is really needed is a stronger job market, with better paid work, so more people can build up a saving buffer.

It’s hard to imagine, for instance, how higher penalties are going to change the behavior of those in dire straits, like Cindy Cromie:

Cindy Cromie…needed the money to rent a U-Haul and start a new life. Her employer, the University of Pittsburgh Medical Center, had outsourced Cromie’s medical transcription work..,

So, last year, at age 56, she moved about 90 miles from her home in Edinboro, Pennsylvania, into her mother’s basement. To make ends meet as she moved and then quit the job, Cromie pulled out $2,767 from her retirement savings. Still unemployed, Cromie is trying to avoid tapping what’s left of her retirement savings — $7,000.

As Michael Olenick remarked via e-mail:

This reads like a Dickens novel. Her retirement savings, in her mid 50′s, were less than $10K but she tapped 1/4th of that. She had to pay a 10% tax penalty plus the funds were treated as ordinary income. In contrast, the executive who outsourced her job probably has investments that will be treated as long-term capital gains and taxed at a much lower rate and the people managing her paltry retirement fund are probably taxed at carried interest rates too.

Welcome to the world of markets uber alle,

Considering how little people have in this free market utopian idea of a retirement fund, and that people are now having to pull it out simple furthers the data that wages have not been high enough for people to live the American Dream of being middle class.

401K? Just another means of capital shifting the costs of labor onto labor and pocketing the savings. Now, had difference in what the company paid to the pension vs their now 401K contribution share been paid in wages as the pension represented wages then things would be different. The outsource arbitrage game applied to employee costs.

But, expecting people to be able to save when their income is not enough to create excess earnings after the risks of living have been paid for is just diabolical thinking.

I would only add that the policy has implications for those who have been fortunate/frugal enough to save more. At 53 I have been working full time over 37 years – I haven’t had anything but a full time job since I was 16. Never took off to go to school, no sabbaticals etc.

Life’s been good and I could possibly leave the workforce in the next few years EXCEPT for not being able to access my 401K funds until age 59 1/2 without getting whacked with a significant penalty.

Dr. Black (Atrios) is right – we need MOARR SOCIAL SECURITY not less. If benefits could be expanded and these penalties were relaxed/eliminated you could migrate a lot of late boomers like me out of the job market and create opportunities for younger people who need to buy houses/save for retirement/kids education etc.

I’ve never drawn an unemployment check once in my life (although there were a few close calls). So why can’t social security get a lump sump for the unemployment insurance I never needed to claim to push me out of the job market? If I could get that and a break on the 401K penalty I’d be a lot more interested in my employer’s “transition to retirement” program which offers me a 3 day week for the next 18 months at 70% salary with full medical and retirement matching benefits over the entire period. If I could start taking distributions from my 401K and get an “unemployment insurance” benefit at 55 I might be able to make it until SS kicks in in my 60s.

Expanded Social Security isn’t a anti poverty program in this respect – it’s a jobs program too.

One more retirement policy I’ve wondered about: Why can’t my 401K funds be allowed to buy my mortgage? Then I could pay my own retirement plan back (with the statutorily required interest of course, probably no longer tax deductible) and my retirement would be invested in at least one thing I genuinely need in retirement besides income – a place to live.

My employers plan allows automatic loans (no credit qualification needed) of up to 50% of account value or 50K whichever is less for a $50 one time fee. All the interest on repayment of those loans accrues “market based’ returns to the account. The only difference here is that the loan would actually acquire a mortgage against my home which would be part of the 401K portfolio along with the bonds/mutual funds I am already interested in.

I have raised this idea before but nobody but me seems to see the value in it heh. The policy protects retirees (you probably don’t want to allow 401Ks to invest in anything but a primary residence for the account holder) and housing markets too. Even if the account holder defaults on his mortgage he does it to his own account and at least ends up with title to the house as long as it has a positive balance. Is this crazy? Or just too reasonable to be considered as a policy ? heheh..

401k’s were a Wall Street scam in the first place. I just would not cash it out, but destroy the industry.

OK I am going to be a wet blanket here.

Would your alarm be the same if we still had a well functioning pension system for most people? 401k’s are basically “rainy day” funds where the target rainy day is retirement. Obviously we should expect that people who have emergencies are going to tap their rainy day funds. Is that by itself really a problem? – Or only becuase 401k’s have largely replaced rather than supplemented traditional pensions?

Perhaps just as importantly, many of these stories are using the present tense in headlines (See also Barry Ritholtz, “Tapping your 401k?”). This data is in no way contemporaneous data. IT IS THREE YEARS OLD. (sorry for shouting, but hopefully you understand the problem), and the most recent, three-year-old, number shows a significant improvement from what happened four years ago. The number of those borrowing from or cashing out their 401ks went up as unemployment went up, peaked about when unemployment peaked, and came down in 2011 as unemployment started to recede. We have absolutely no idea what has happened in the last 3 years, and furthermore it is a good bet that 401k’s were raided less and less and the unemployment rate continued to go down. All of this seems non-contoversial to me.

It’s also worth pointing out that the series isn’t population adjusted, which is a non-trvial difference, and the 38% increase in the number of IRS returns incurring the penatly is faiirly consistent to the ~60% increase in the unemployment rate from 6% to 10%.

The alarm shouldn’t be that people tapped into their 401k’s as the unemployment situation worsened. The alarm should be that 401k’s are a dismal (and to some extent intentional) failure as a replacement for the traditional pension. No company should be allowed to offer a 401k that does not include a substantial company match, or is in lieu of or bigger than its traditional or defined contribution pension, or is not as generous percentagewise as its stock option or other incentive program for senior executives.

That, it seems to me, is the disgrace. Not that people cashed out or borrowed from 401k’s more in 2008-11 than they did in 2002-06.

Not so much a wet blanket NDD, and probably not in disagreement. Good point. Care to guest post?

Is it not Past Time that we stop saying that people who finish receiving Unemployment payments HAVE STOPPED LOOKING FOR WORK. I care not what the government uses for terms….it is a lie….a very large lie and is only used so the number of unemployed is kept low. Why do people who know better play their game? I’m not sure of the real humber but I do know it very very large.

Obama’s popularity is quite low since the first of the year and various polls show the GOP pulling ahead of Democrats on the generic mid term ballot. This at a time when the stock market has held on to its exceptional gains of last year, unemployment is reported to be falling, consumer confidence is supposed to be rising and we have not all died with the further implementation of the Affordable Care Act. There are a lot of people hurting in this country and scared to death about the future–I am one of them, not for myself but at least one of my daughters–and there is simply no reason to support a president or his party who have not addressed the needs of the vast majority of working men and women in this country with anything more than an occasional speech. Now I have absolutely no idea why that helps the GOP who is even worse–Fox News?

Dan

of course i don’t mind being a wet blanket so i will say it doesn’t seem to me so much that New Deal Dem made a good point as that he missed the point, or that he failed to realize that his point was the point of the article.

Or maybe I missed the point. Yes it’s great that people have a rainy day fund. It’s not so great that their rainy day fund is their retirement fund. Of course it would be anyway… though in general it is better for people if they “can’t touch” their retirement, rainy day or not, or they end up with nothing when they are too old to do anything about it. While most rainy days can be coped with one way or another… or could be if people were either a little more prudent or living in a country where prudence was actually possible.

I think I have seen both lack of prudence and just no (prudent) way to cope with the economy we have. In a sense I got lucky: I lived prudently and never had a really bad rainy day, and got out before things really went to hell has they appear to have done since about 2000 or 2008 for many people.

Just a final word from our sponsor: you CAN live on your Social Security. Not the way you might have expected to live, but you might be surprised that a decent level of poverty can be quite a pleasant way to live.

This is not to say that I approve of the way the American economy is being managed (by the people who don’t believe in government management), but it is also to say that as far as i can see a lot of people are hysterical because they are not going to be rich… and that is not the same as being ugly-poor with no hope… which is also happening to many people.

We seem to go through cycle after cycle of this destruction of the American middle class. In the 1980s, you had to have a two income family to make ends meet. In the 1990s, the stock market was the big savior, at least until the bust. In the 2000s, it was real estate equity and HELOCs. Each time, the middle class has taken a hit, and it has been harder and harder to maintain anything close to a middle class life style. All the risks have been offloaded by the titans of capitalism onto their employees (or contractors more likely) or the government. It’s nice work if you can get it.

People often wonder why the Greenland colonists wouldn’t eat fish or the Soviet Union stuck with communism until it collapsed. Well, we Americans are watching the same kind of thing happen here.

http://xnerg.blogspot.com/ Skippy link