Real GDP per Capita

My last Angry Bear post generated such a wonderfully amusing comment stream that I couldn’t resist posting a follow up. One of the criticisms was that I didn’t consider Real GDP per Capita. At the risk of having anyone think I accept homework assignments from trolls, here is a look at that very thing. I’m snowed in tonight, so what the hey.

I usually like more finely granulated data over a longer time span, but sadly discontinued FRED series USARGDPC gives us annual data from 1961 through 2011, and that’s plenty good enough to make a point; the point being that the American economy is dying a slow and agonizing death. This, alas, despite enormous tax cuts enduring over decades. For the supply-siders among you, we’ll take an extra special look at the Reagan years.

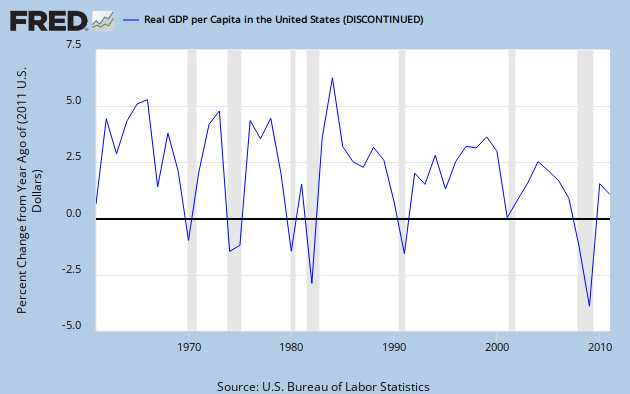

Graph 1, from FRED, shows YoY RDGP growth over the span of the data series.

Graph 1 – RGDP per Capita, YoY % Change

The single most prominent feature of this trace is the downward trend over time, characterized by both lower lows and lower highs. This should be pretty obvious, even to the causal observer; but if you cannot see it, don’t be disturbed, I’m going to help.

Graph 2 shows the same data, along with some trend indicators.

Graph 2 – RGDP per Cap, % Change, with extra colored lines

Parallel trend channel boundaries are indicated in red and green, with the center line in yellow. The Excel generated least squares trend line is in dark blue, and a moving 5 year average in purple. Each of these additions is a visual aide, indicating that the trend over time has, indeed, been down. Certainly, it has not been monotonic. The real world seldom works that way. But what you see here, with some exceptions, are mostly worsening recessions, and increasingly anemic recoveries.

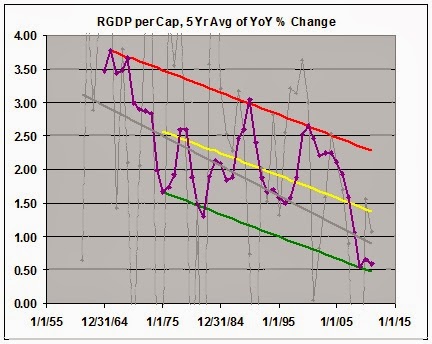

Next, let’s focus in on the 5 year average. Graph 3 gives that to us, along with it’s own set of trend lines. The vertical axis is truncated relative to graph 2, and the downward slope is therefore emphasized. This makes it easier to see that the 1990 peak is considerably lower than the double peak of ’66 – ’69.

Graph 3 – 5 Year Average of RGDP per Cap Change, with extra colored lines

The 5 year average is in purple. The base data and least squares trend line are in grey, The red, green and yellow lines are again parallel channel boundaries and midline. The last time the average line touched the top channel border was in 2000. After that, despite the Bush tax cuts, things went into a bit of a decline, culminating in the worst financial disaster since the Great Depression.

I know what you’re thinking. The next to last peak in Graph 3 came in 1990, the culmination of the Reagan miracle, just before his buzzards came home to roost, costing Bush Sr. his chance at a second term. But remember that that peak is considerably lower than those of the 60’s, and scarcely above the mundane years of ’70 to ’73.

And back in graph 2, the highest single growth year ever was in 1984, the third year of phase-in for Reagan’s 1981 tax cut. Well, sure – but note that 1984 was a one-off, and also the recovery year from an exceptionally deep Fed-induced double-dip recession in the previous 3 years. So, beside a lot of pent up demand, there were a few other things going on that might have given RGDP a boost.

Graph 3 shows the Effective Federal Funds Rate, which made an erratic drop from a high of just over 19% in mid ’81 to 15% in early ’82, then to under 9% by 1984.

{kind=link}

Graph 3 – Effective Fed Funds Rate, 1980 to ’84

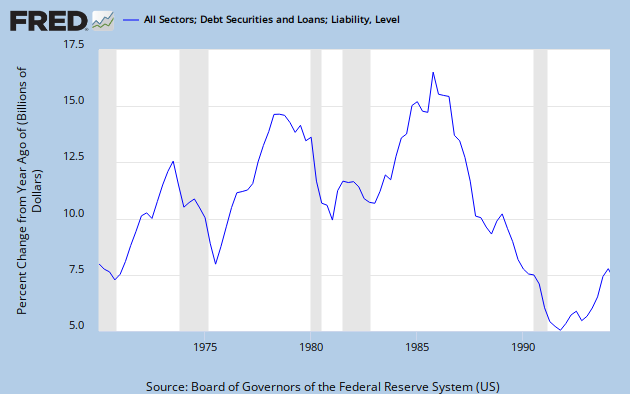

Graph 4 shows the explosion of credit that occurred coming out of 1982. By 1984 it was close to an all time high. It finally reached that peak in 1986, then collapsed.for the rest of the decade.

Graph 4 – Credit Expansion, 1978 to 1994

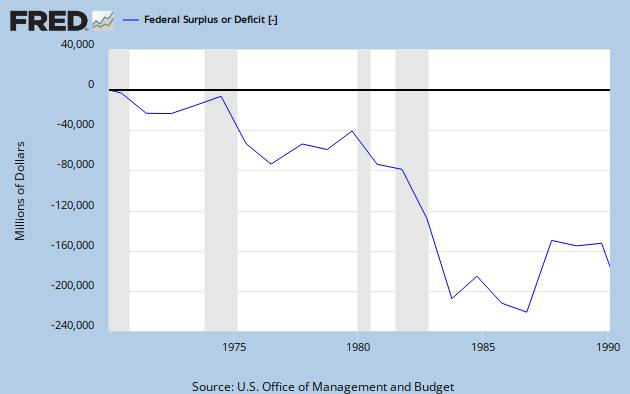

And let’s not forget that Reagan was responsible for what was at that time, the most profligate explosion of federal spending ever seen, as shown in Graph 5.

Graph 5 – Reagan’s Deficit Spending

So let’s recap.

Big picture: Decades of tax cuts have not led to increasing prosperity. Quite the opposite. The growth rate of RGDP per capita has declined substantially since the tax cuts of the 60’s, and most severely since the 2001 tax cuts. The ensuing change in RGDP/Cap growth is somewhat reminiscent of what happened from ’69 to ’75, but as yet without much recovery.

Focus on the Reagan years: After a long and deep recession, tax cuts plus the steepest decline in nominal interest rates ever seen in the 20th century, plus a huge expansion in federal spending, plus an explosion in credit resulted in a single year of outstanding GDP growth, followed by four decent but less than stellar years, which incidentally also included the 1986 tax cut. Then, alas, in 1991, there was another recession.

If you can look at this data and still have the opinion that tax cuts boost the economy, then knock yourself out. Everyone is entitled to an opinion. But you might want to ponder why your opinion has so little overlap with reality.

I welcome your comments, but please keep them more or less relevant to the topic, and if you are going to disagree, please bring more than assertions. Facts and data have some gravitas.

Lower tax rates, since 1981, facilitated one of the greatest eras of U.S. prosperity, the “long boom,” from 1982-07, where U.S. living, labor, and environmental standards rose at steeper rates.

Just watch of episode of “Kojak.” to see what I mean 🙂

And, this deep depression, and train wreck, since June 2009, is completely unnecessary.

U.S. average annual per capita real GDP growth

1982-2007: 2.30% (height of the Information Revolution)

1946-1981: 2.11% (including rebuilding Europe and Japan)

It should be noted, trade deficits, which increasingly rose from zero in 1980 to 6% of GDP by 2006, subtract from GDP.

PT –

It’s late and I’m going to bed.

Re: you’re first comment – did you even read the post and look at the graphs?

Re: you’re second comment, I don’t think so, and will provide numbers in the morning.

Re: your third post, tl;dr. I’ll read it in the a.m. If it does not meet some semblance of relevance, it’s going in the trash heap.

You really are trying my patience.

Good night.

Jazz:

PT does not care what he says and is off in his own ramblings which are not relative to your post. Right now, he appears to have hijacked your thread.

JazzBumpa, percentages can be misleading. For example, if I lose 50% and then gain 50%, I lost 25%.

There were only two recessions from 1982-07, one mild and one moderate.

Also, I may add, I cited “Kojak” to show how people lived, worked, and what a mess the environment was in the 1970s compared to the 2000s.

Per capita real GDP growth from 1983-89 (seven years) averaged 3.45%, and from 1982-90 (nine years) averaged 3.14% (and even higher from trough to peak). So, it was a strong, and long, expansion, with a V-shaped recovery.

The increase in defense spending not only won the Cold War, it created a “peace dividend,” which facilitated growth in the 1990s (as defense spending declined to a multi-decade low as a percent of GDP, even with increasingly larger trade deficits, which subtract from GDP growth).

It should be noted, Reagan wanted to cut other spending programs and made deals with Congress to raise taxes for spending cuts, which didn’t work out well for Reagan.

Of course, disinflation, lower interest rates, and a strong expansion will increase the demand for credit, and federal deficits or surpluses are more accurately measured as a percent of GDP.

Never elect a president from California or Texas.

From Angus Maddison’s data , via Lord Keynes:

Average Decadal Real Per Capita Growth Rates

Average Growth Rate 1941–1950: 3.87%

Average Growth Rate 1951–1960: 1.75%

Average Growth Rate 1961–1970: 2.88%

So , ~2.9% for 1941-1970

Average Growth Rate 1971–1980: 2.16%

Average Growth Rate 1981–1990: 2.26%

Average Growth Rate 1991–2000: 1.94%

~2.1% for 1971-2000

We’ll be lucky to get 1.0-1.5% for 2001-2030 , based on results so far.

Yeah , supply-side was a smokin’ hot innovation in growth theory.

Forgot to leave the link :

http://socialdemocracy21stcentury.blogspot.com/2012/09/us-real-per-capita-gdp-from-18702001.html

Marko, my data are from the BEA. Your data make no sense.

For example, under the Clinton economy from 1995-00, actual output exceeded potential output, the country was beyond full employment, real wages rose, and there were budget surpluses. Oil and commodity prices were very low, there was a “peace dividend,” and the Baby-Boomers (born between 1946-64) reached their peak productive years (i.e. “prime-age” or 35-54). We were in a spectacular structural bull market. It was one of the greatest periods of domestic growth.

PT –

I have no idea what the point of your first comment from last night is. I’m leaving it there so people can laugh at you.

In your 2nd comment you average RGDP from ’82 to ’07, as if the Great Recession had nothing to do with policies of the preceding years.

And there is a bit of unfairness in including the 50’s in a long run GDP/Cap calculation due to the denominator effect. The 50’s was the height of the post war baby boom, so anything measured per cap will be distorted downward.

http://research.stlouisfed.org/fred2/graph/?g=rBy

From the data in the graphs above, I get RGDP/cap averages as follows

1961-81 2.47%

1982-07 2.03%

1982-11 1.83%

And trade deficits are either GDP neutral or actually cause an increase, since they represent borrowing used for investment and/or consumption.

http://www.infoplease.com/cig/economics/trade-deficits-bad-good.html

So your first two comments are nonsense.

I’m taking the third one down for irrelevance. This post is not about China. Also, your 10:17 am comment. Attack ideas, not people.

And, yes, percentages can be misleading. That’s exactly why 1984 looks so good.

This is your last warning. You will stop being trollish or your future comments get deleted.

Persist, and I will delete them with extreme prejudice.

JzB

You gotta love the “won the cold war” thing.

My all time favorite.

JazzBumpa, I see you weakened my position by deleting some of my comments. You’re biased, dishonest, and want to remain delusional. So, why waste my time contradicting you with actual data.

JzB,

There are two graph 3’s. Just wanted to let you know. No need to post this comment.

Also, I may add JazzBumpa. I saved everything I wrote, along with saving valuable comments from other people, to contradict your economic ignorance in articles by moderate and open-minded people with at least some understanding of economics. You’ll be cited appropriately 🙂

Peak Trader –

That’s it.

There is a limit to my good graces.

You were warned and still persisted, and now you have personally insulted me. That comment is staying up.

I give every commenter the benefit of the doubt, sometimes excessively so. You have proven yourself to be a troll on two consecutive posts. There is no reason either I nor any serious reader needs to put up with that.

In the future, any comment you make on any post of mine will be treated as spam.

Go take your drivel somewhere else.

JzB

Angus Maddison’s annual data quoted at 10:24 above is generally in good agreement with the post 1960 data I got from FRED. They do separate a bit in the years ’96 to 2000 andcthere is the occasional discrepancy, but for the most part, those are in the second decimal place.

So Marko’s data are not nonsense.

Averages

Marko FRED

61 to 70 2.88% 2.90%

71 to 80 2.17% 2.13%

81 to 90 2.27% 2.30%

91 to 00 1.95% 2.17%

JzB

There are two graph 3’s. Just wanted to let you know.

That’s what i get for posting late in the evening.

I’ll leave it that way to prove I’m human.

JzB

jazz:

Don’t feel bad, I have more more in the title of one post

Jazz,

I wonder if the difference between the Maddison/FRED data is due to the recent “redefinition” of U.S. GDP.

The big difference appears in the ’91-’00 data , so mission accomplished for our statisticians , I guess. They’re making things look better in recent years , as per their mandate.

The Maddison data I cited would come from the pre-fudged era.

There are two amazing details here:

* GDP statistics are cleverly “influenced” by massive hedonic adjustments, so they tend to be rather optimistic. How cleverly? Well, for example:

http://equitablegrowth.org/2014/01/14/1688/afternoon-must-read-larry-summers-no-a-one-commodity-model-is-not-adequate

* As the very, very good book “Wall Street: the book” by Doug Henwood reports, in the past 30 years borrowing against the nominal valuation of house prices as collateral has been equal to over 100% of GDP growth; in other words the *entire* GDP growth of the past 30 years has been equal to the demand financed by home equity withdrawals.

Marko –

GDP does get revised, and an existing publication would perhaps not keep up with that. I’m not aware of the redefinition, though. Do yuo have some information on that?

Blissex –

The GDP to home equity extraction equivalence is astounding.

JzB

Jazz,

Here’s a description from the FT :

“Data shift to lift US economy 3%”

http://www.ft.com/cms/s/0/52d23fa6-aa98-11e2-bc0d-00144feabdc0.html

The revisions are supposed to apply to all past data , but my suspicion is that it’s mostly designed to make recent/future performance look better.

I don’t know if FRED is fully updated yet , but I’m pretty certain the Maddison data I cited would be based on the old methods.

So, the monetarist says if a) there is inflation so that the future value of money will be less than the current value of money, then b) money printed and placed into consumers’ pockets — whether by a tax cut or a check mailed directly to them — should be spent relatively quickly. After all, it will simply lose value if stuffed under a mattress, right?

Except your graphs show — and the Fed’s flow of funds data from the last tax cut (the Obama stimulus tax cut) shows — that it doesn’t happen that way. In many cases, the money goes either into deleveraging (i.e. paying for *past* economic activity) or into savings (which in an economic downturn is basically a virtual mattress, since banks don’t lend during a downturn, due to the effects on their own balance sheets of consumers and businesses going bankrupt during a downturn).

But why? Clearly there is another factor, and I believe the needs hierarchy is what is telling people to assign higher future value to the money than would be predicted. In other words, during an economic downturn printing money will often result in plump mattresses as people save up for when they become unemployed, rather than economic activity.

In other words, the monetarist solution might work if the economic downturns are caught swiftly before consumer sentiment can collapse, but once consumer sentiment has collapsed and people view their future income as less than needed for survival, it won’t work. And long-term it doesn’t work anyhow, as your graphs show, because it simply redistributes spending in the economy rather than increase the overall level of spending.

The oddest thing is that you don’t even seem to need to get to the zero bounds before you start the predicted Keynesian effect of pushing on a string. All it requires is low enough consumer sentiment combined with low enough (but above zero) inflation, and you get what the Keynesians predict will happen at the zero bounds..

More at my blog: http://snarkypenguin.wordpress.com/2014/02/02/more-on-tax-cuts-helicopter-drops-at-the-zero-bounds/

This is impressively bad news. I knew that the value of an hour’s labor in terms of per capita GDP has been falling, not that the real value of the GDP has been falling as well. We’re halfway to being like the Soviet Union. We have “they pretend to pay us”, but we haven’t quite reached “we pretend to work”. I give it another generation.

P.S. Which GDP deflator is being used? I gather there is a deflator designed for deflating macro statistics like the GDP, and that this deflator has diverged from the deflator used to measure the value of wages.

A very telling explicit explanation of the aggregate economic trend. What is missing is how real median household-wages stagnates from 1980 and onwards. One would look not only on RGDP but also on real investments by businesses and government/public. I think it is undisputed that there is positive correlation between wages and investments. And the real investment-trend in the USA has also been stagnating since the 80´s. Notably real investment by business had a big rise in the 90´s and also 00´s. But still inside “trend-channels”. It is also worth noting that todays business-investments have shorter cycles(product-cycles). This is the result of new and very fast developments in digital-technology, hard competion and easy credit in low interest-environment. Shorter product-lifes does not promote employment the way we where used to. And we have a skill/competence matching-problem as well.

Total credit-growth is also a good teller about the long term economic prospects. The diminishing return on growth(GNP) per dollar-credit is in constant fall.

It would be interesting if you could post real investment/wage-data based on the same sources(FRED).

A growing economy requires a growing supply of money, which is what tax cuts provide. However, some tax cuts act faster than others. Cutting taxes on the rich may have a very slow response, as the rich do not spend money quickly.

But eliminate FICA (http://mythfighter.com/2009/09/08/ten-reasons-to-eliminate-fica/) and you will see immediate, positive GDP growth.

A better source of “growing supply of money” is wage increases, not tax cuts. Tax cuts merely shift money from one spender to another.

Tax cuts do not increase the “supply” of money.

Tax cuts are not the same nor the equivalent of income increase via productivity growth. Thus tax cuts are not the same nor the equivalent of a wage increase.

Tax cuts are simply a means of further shifting the transfer of income from productivity growth to those with the control of capital.

Tax cuts are simply the maintenance of what ever the current income distribution is. There is no new money being distributed broadly thus driving velocity.

As long as we can cut taxes, companies will continue to be insulated from the effects of misappropriations of the income produced by their efforts. That is, we can continue to believe the economy is growing when it is not.

Of course, this ignores the effects of the nation’s asset and capital destruction do to lack of maintenance and investment in new tangible assets that also drive the intangible assets that allow one’s company to further develop productivity growth as a continual decrease in tax collections.

If you are going to grow the money supply, printing money and giving it to people who need it such as the unemployed and the poor is probably more effective than tax cuts to people who already have more money than they could reasonably spend in any given lifetime. In fact giving money to people who have more money than they could reasonably spend in any given lifetime will *reduce* consumption, because they will invest the extra money in commodities, driving up commodity prices, making goods more expensive for consumers, meaning fewer goods sold.

As for FICA, the problem is not that it’s a tax, but that it is a regressive tax that hits the poor and barely touches the rich. This is a consequence of pretending Social Security is a pension fund, which it is not and has never been — it is a pay-go system where past workers’ retirements are funded by current workers’ taxes. FDR had to pretend it was a pension fund to get it passed, but it’s long past time to admit reality and expand the FICA tax to all income both earned and unearned and exempt the poorest of workers from paying it.

Well, the EITC does “”exempt” the poorest of workers from paying it. We do need to expand it to help those without children.

Somehow I have a problem with RMM’s idea of cutting FICA adding to spending and growth. Considering they are paygos the money is already being spent.

If you’re talking about printing money to increase the money supply, printing money to pay Social Security benefits rather than paying them via FICA taxes is no different from printing money for any other purpose. Still, we should be aiming for long-term financial neutrality for Social Security such that long term, it’s paid for out of the tax stream, not by printing money, because you can’t keep printing money once the economy starts heating up or you get inflation as people quit stashing money under mattresses and start spending it again.

Daniel Becker said, “Tax cuts do not increase the ‘supply’ of money.”

Federal taxes (as opposed to state and local taxes) leave the money supply as soon as they are received. Therefore, tax cuts do increase the money supply by reducing the drain on the money supply.

In contrast, state and local taxes are stored in private bank accounts, so are included in the money supply.

EMichael said, “Somehow I have a problem with RMM’s idea of cutting FICA adding to spending and growth. Considering they are paygos the money is already being spent.”

Actually, federal taxes do not support federal spending. The federal government is Monetarily Sovereign (http://mythfighter.com/2013/07/27/i-just-thought-you-should-know-lunch-really-can-be-free/) meaning it creates dollars by spending dollars.

When you pay federal taxes, the dollars leave the money supply. This includes FICA taxes.

By contrast, state and local governments are monetarily non-sovereign. Those taxes remain in the money supply.

In short, contrary to popular myth, federal Social Security and Medicare are not “paygo,” though the state part of Medicaid is paygo.

Badtux said, “As for FICA, the problem is not that it’s a tax, but that it is a regressive tax that hits the poor and barely touches the rich. This is a consequence of pretending Social Security is a pension fund, which it is not and has never been — it is a pay-go system where past workers’ retirements are funded by current workers’ taxes.”

FICA does not pay for Social Security or Medicare. (See: http://mythfighter.com/2010/08/13/monetarily-sovereign-the-key-to-understanding-economics/ )

The federal government is Monetarily Soveriegn. It creates dollars by spending. This is in contrast to state and local governments, which are monetarily non-sovereign, so need taxes to pay their bills.

Badtux also said, ” . . . it’s long past time to admit reality and expand the FICA tax to all income both earned and unearned and exempt the poorest of workers from paying it.”

Actually, it’s long past the time to eliminate the FICA tax altogether. It funds nothing. See: http://mythfighter.com/2009/09/08/ten-reasons-to-eliminate-fica/

“Check, Please!”

Uhm, Rodger. Every dime the Federal Government collects as taxes re-enters the economy as Federal spending within days of entering the Federal coffers. There is no vault where tax money gets stored, we’re running a deficit at the Federal level. Pay attention to the news, okay?

And yes, you can print money via Federal spending, and in fact we are doing so, selling Treasuries to the Federal Reserve in exchange for dollars. There are limits, however, to how much money you can print before it is a problem. Those limits are extremely high during a recession because printed money tends to flee to under (virtual) mattresses, but there are limits, nevertheless. Funding 100% of national government operations via printing money has never proven viable for any country that’s ever tried it. Though admittedly, none of those countries possessed what is basically the fiat currency of the entire planet….

Kaleberg –

You raise a good point about the deflator. As I showed here with Doug Short’s work, it can make a substantial difference.

http://angrybearblog.strategydemo.com/2013/10/different-views-of-real-median-household-income-and-recessions.html

The more I think about inflation adjustment, the less I like it.

Per Capita throws a clinker in there too. I might address these things in another post.

Christer Kamb –

Yes, agree with what you are saying. I’ve at least glanced at some other variables, in this post and the earlier one linked there.

http://angrybearblog.strategydemo.com/2013/09/rational-nonexuberence-part-2.html

For deep analysis, check out Edward Lambert’s posts here at AB.

Rodger Malcolm Mitchell –

There are non-economic reasons for keeping FICA as a funding mechanism for SS and Medicare. It has to do with perceptions over-riding reality. Without FICA, SS and Medicare are welfare programs, and a large percentage of the population hates welfare.

Sometimes the psychology has to be a driver as well. See posts on SS by Coberly and others here.

Cheers!

JzB

JazzBumpa

February 3, 2014 1:30 pm

Thank You for a great post. Graph 5, 7 and 9

were all very interesting!

( Graph 9 – USARGDPC/JPNRGDPC)