Changes in Funding for the IRS Will Impact Service During Filing

Is downsizing the IRS part of Trump’s goals? I would say it is. Short staffing an agency such as the IRS makes it difficult to maintain the process and also audit taxpayers. Those who take advantage of greater would welcome an IRS less capable. It, like other parts of the Federal Government, has been faced with cuts to staffing. Granted some of this was be needed. This reduction specifically targets the higher income brackets who may take advantage.

We shall see how bad this one is sooner than the next tax season.

As part of the president’s push to downsize the civil service, more than 26,000 IRS employees left the agency, generally after the 2025 tax season and mostly as a result of voluntary separation incentives. In contrast, during the Biden administration the IRS workforce grew to more than 100,000 staffers.

And the cuts may not be finished. The tax agency reported in its fiscal 2027 budget justification it is aiming to shed another net 4,000 staffers as part of a $1.4 billion funding reduction request.

~~~~~~~

If you cut staffing, you can impede service. “Funding rescissions and executive-wide workforce reductions led to a significant drop in IRS personnel in recent months.” Hence operational short falls is the result of labor reductions.

IRS Staffing Cuts Will Reduce Revenues, Driving Deficits Higher

Summary

The Internal Revenue Service’s (IRS’s) budget funds various activities directly and indirectly affecting the amounts of revenues it collects. Historically, the IRS’s funding has primarily been discretionary. That is, the agency has mostly been funded through annual appropriation acts. Through 2031, however, the agency’s activities are also supported by nearly $80 billion in mandatory funding provided in the 2022 reconciliation act (Public Law 117-169).

The Congressional Budget Office report describes how funding for the IRS affects CBO’s baseline projections of revenues and how the CBO estimates the revenue effects of rescissions of such funding. (Rescissions are provisions of law that cancel budget authority previously provided before it is scheduled to expire.) In addition, the agency estimated the budgetary effects over the next 10 years of three illustrative options that would rescind varying amounts of the IRS’s mandatory funding:

- A $5 billion rescission would reduce revenues by $5.2 billion over the 2024–2034 period and increase the cumulative deficit for that period by $0.2 billion.

- A $20 billion rescission would reduce revenues by $44 billion and increase the cumulative deficit by $24 billion.

- A $35 billion rescission would reduce revenues by $89 billion and increase the cumulative deficit by $54 billion.

In CBO’s assessment, the IRS would respond to a rescission by maintaining its planned spending in the near term and reducing outlays in the final years before the budget authority expires. CBO also expects that the IRS would first curtail enforcement activities that, in its view, will have the lowest average return. Thus, the revenue reduction per dollar rescinded would be larger for a $20 billion rescission than it would be for a $5 billion one and even larger for a $35 billion rescission.

In 2019, the Government Accountability Office found that the IRS faced several workforce-related challenges that “pose risks to meeting its mission” and result in “billions of dollars in taxes [going] unpaid every year.” To address the structural challenges facing the agency, lawmakers provided $80 billion to the IRS over ten years through the 2022 Inflation Reduction Act (IRA). With the new funds, the IRS was able to begin to rebuild its workforce.

However, since the IRA, a series of funding rescissions and executive-wide workforce reductions led to a significant drop in IRS personnel in recent months.

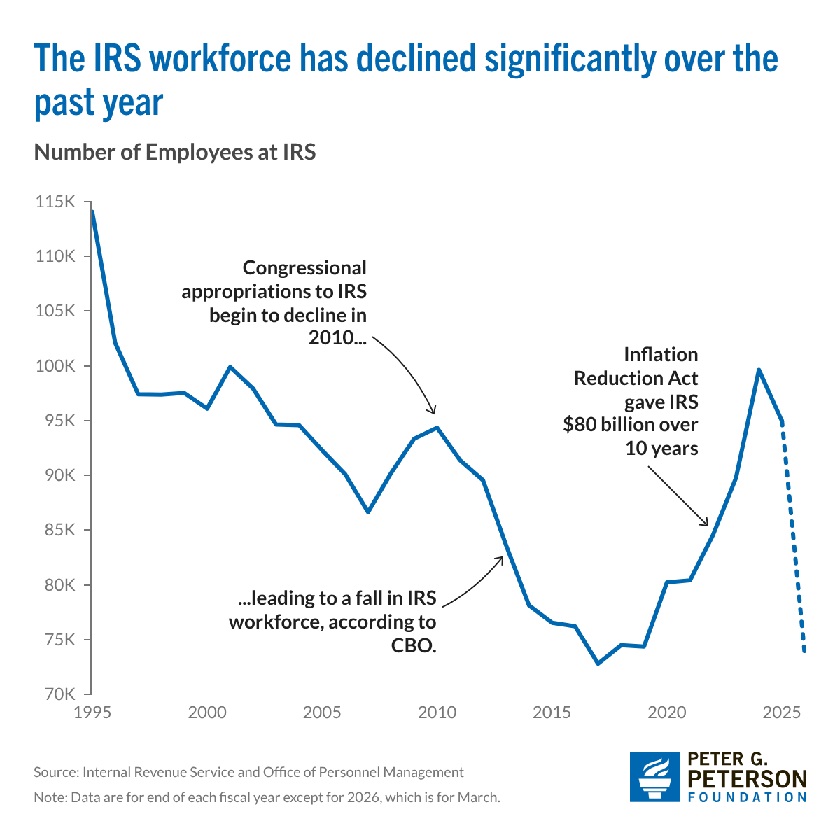

Some History: How Much Has the IRS Workforce Declined?

The number of IRS personnel remained relatively stable from 1998 through 2011. However, the workforce began to decline in the 2010s as Congress appropriated fewer funds to the agency. According to the Congressional Budget Office, the decline in IRS funding and staff led to a decline in IRS law enforcement activities. The amount of additional tax required after audits fell from $63 billion in 2010 to $32 billion in 2018 (adjusted for inflation to 2023 dollars). In 2017, the IRS workforce fell to 73,000, its lowest level since at least 1995.

In 2019, the Government Accountability Office found that the IRS faced several workforce-related challenges “posing risks to meeting its mission” resulting in “billions of dollars in taxes [going] unpaid every year.” To address the structural challenges facing the agency, lawmakers provided $80 billion to the IRS over ten years through the 2022 Inflation Reduction Act (IRA). With the new funds, the IRS was able to begin to rebuild its workforce.

However, since the IRA, a series of funding rescissions and executive-wide workforce reductions led to a significant drop in IRS personnel in recent months.

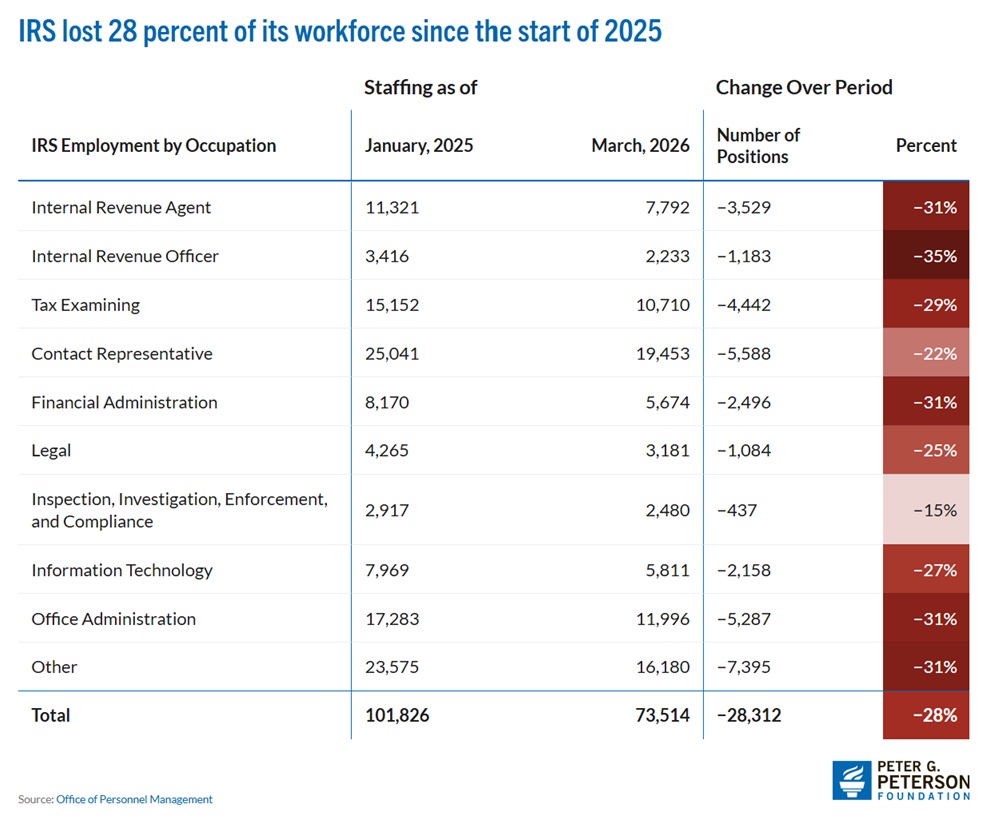

The NTA warns that the 2025 staff reductions may impact the ability of the IRS to properly administer the 2026 filing season. This year, in addition to its regular activities of responding to taxpayers’ questions and processing filings, the IRS must also update systems to reflect recent changes in the tax law. The One Big Beautiful Bill Act made more than 100 changes to the tax code, many of which are complex, according to the NTA. Overall, the agency lost 28,312 employees from January 2025 through March 2026, including significant losses in the number of internal revenue agents and officers as well as contact representatives.

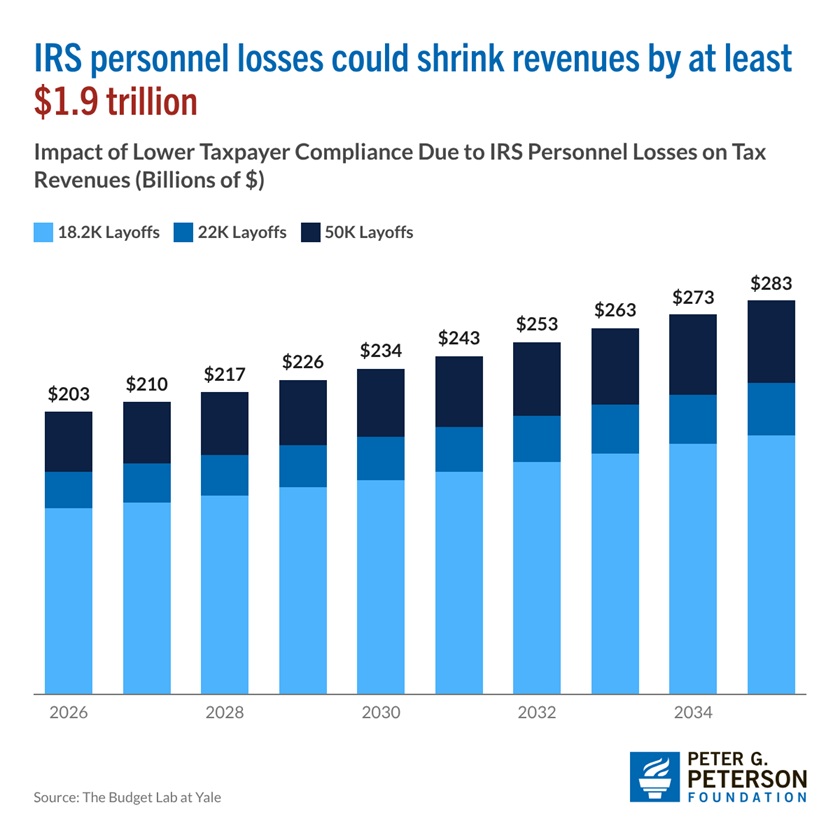

IRS Personnel Loss is Projected to Decrease Revenues, Adding to the Deficit

At the start of the reduction-in-force (RIF) in early 2025, the Budget Lab at Yale estimated the revenue effect of reducing the IRS workforce. The Budget Lab found that a 22,000 RIF at the agency would reduce federal revenues on net by $198 billion from 2026 through 2035. A 43,000 RIF would shrink revenues by $286 billion over the same period. However, the Budget Lab also estimated the effect that a sizeable RIF could have on taxpayer behavior, as less law enforcement activity by the IRS could reduce voluntary taxpayer compliance. The Budget Lab estimates reduced taxpayer compliance due to a 22,000 RIF could decrease revenues by $1.9 trillion over ten years.

Increasing IRS funding to provide for additional enforcement activity either through more staff or improved technology would increase revenue collections, thereby reducing deficits. A recent study found that for every additional $1 spent auditing taxpayers above the 90th percentile, revenues increase by more than $12. For audits below the median income, revenues increase by $5. That means that providing more funding for the IRS to perform its audit function more than pays for itself. Additionally, IRS taxpayer engagement increases taxpayer compliance and revenue collection.

Conclusion

Reductions in IRS personnel decrease federal revenues, increase deficits, and significantly exacerbate the gap between taxes that are owed and taxes that are actually paid. Increasing IRS funding and personnel would help to shrink the tax gap, promote fairness in the economy, and be a step toward addressing America’s structural mismatch between spending and revenues.