Inflation Depreciates Wages

Intro: Former Biden CEA Chair: Jared Bernstein from his new Econ Site. Right now Jared’s site is opened to all readers with no fees for the site. You may want to take a few moments and read what he has to say on various economic topics while you can,

This commentary is on inflation and its impact. More informative than what this former manufacturing and supply chain supposed expert can provide. I say such because when everything was going well I was just a person at a desk or on the floor. If things were erupting somewhere within our corporation globally, I was suddenly the expert.

Increasing inflation and costs are impacting wage and cost of living.

“May Inflation: Higher Inflation Is Driving Real Wages Down,” Jared Bernstein

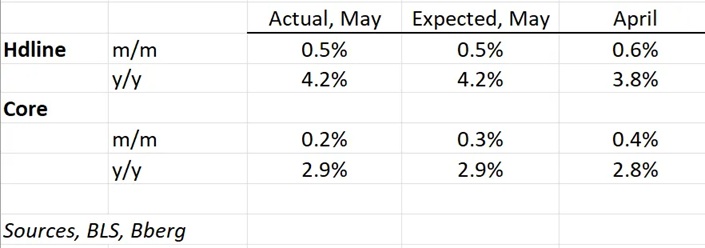

Here’s what struck me in today’s CPI inflation report for May:

—Consumer inflation was up 0.5% in May and 4.2% over the past year. That’s the highest yearly rate since April 2023.

—Core inflation—sans food, energy—rose 0.2% and 2.9%, respectively.

—Both measures came in at around expectations, though the slightly downside miss on monthly core is welcomed.

—The gas price was up 7% last month after rising 5.4% in April. More recent data, however, show the national gas price falling consistently since May 20th, down $0.41, about 9% through this AM. That’s due to both lower oil prices on rumors of peace talks re the war and also diminished driver demand in reaction to prices that still remain well above pre-war levels of around $3/gal. To be clear, we’re still far from out of the Strait woods, given that missiles are flying as we speak. Though this recent trend is welcomed, given consumers’ affordability constraints, no one should be overly confident that it continues.

—A year ago, headline/core CPI inflation was 2.4%/2.8%, yr/yr. IOW, we’re in the midst of a considerably higher headline inflation regime, at least for now, while core is also somewhat elevated…and sticky.

—Inflationary pressures are coming from tariffs, the Iran war, and strong demand for the inputs into AI.

—While energy costs in particular are driving up inflation over the past few months, price pressures are bleeding into the core as well. This is a particular concern for the Fed, as the further such pressures spread, the less they can “look through” them (i.e., consider them a one-time shock to the price level, versus a persistent growth pressure point).

—As noted, AI, along with import-price pressures, is generating notably and usually higher inflation in computers and software, though the price stayed flat in May:

—Housing inflation, heavily weighted in the CPI, continues to come in at mild rates: the CPI shelter index rose 0.3% in May and has been trending around pre-pandemic rates. Of course home- and rent-price levels remain elevated relative to both history and incomes, especially for younger people.

—There is thus little doubt that in their meeting later this month, even under new Trump-related leadership, they’ll shift their language from a cutting to a neutral bias.

—Here’s where inflation is not coming from: wages. Both nominal and real wages have slowed in recent months, even as the job growth has picked up.

—Real wages fell -0.7% over the past year for all private-sector workers and -0.6% for mid/low-wage workers. That’s the second month in a row of declining real wages, something we haven’t seen since ‘23.

Bottom line, policy is pushing up prices and has been doing so ever since the beginning of Trump’s 2nd term.

That’s obviously a big problem for the majority of Americans who were already stressed about making ends meet, and now face the new problem of real wage pressures. In more macro-econ terms, it’s a potentially longer-lasting problem if price-setters in the economy come to believe these price pressures aren’t going away any time soon, and thus start building them into their expectations. There’s some evidence that this is occurring—”de-anchored inflationary expectations”—but it’s still in a range where it could be corrected.