Inflation Negating Worker Wage Increases

Biden passed a strong economy over to Trump. A few things Biden passed on to Trump is due to a strong economy:

– Inflation was tamed without a recession.

– Workers benefited from a strong labor market in years

– Households, especially those limited by prior barriers, saw substantial wealth gains.

Americans faced significant price spikes and a 40-year high in inflation during the middle of Biden’s term. The overall rate of inflation cooled down closer to pre-pandemic levels by the time he left office. Trump blew it up again with his deficit increasing tax breaks for upper income brackets and businesses..

~~~~~~~

“More Inflation, and What Kevin Warsh is Getting Wrong”

Jared Bernstein’s latest commentary. Inflation is wiping out gains by Labor. Via sharp prices pressures. etc.

Partial from Jared Bernstein

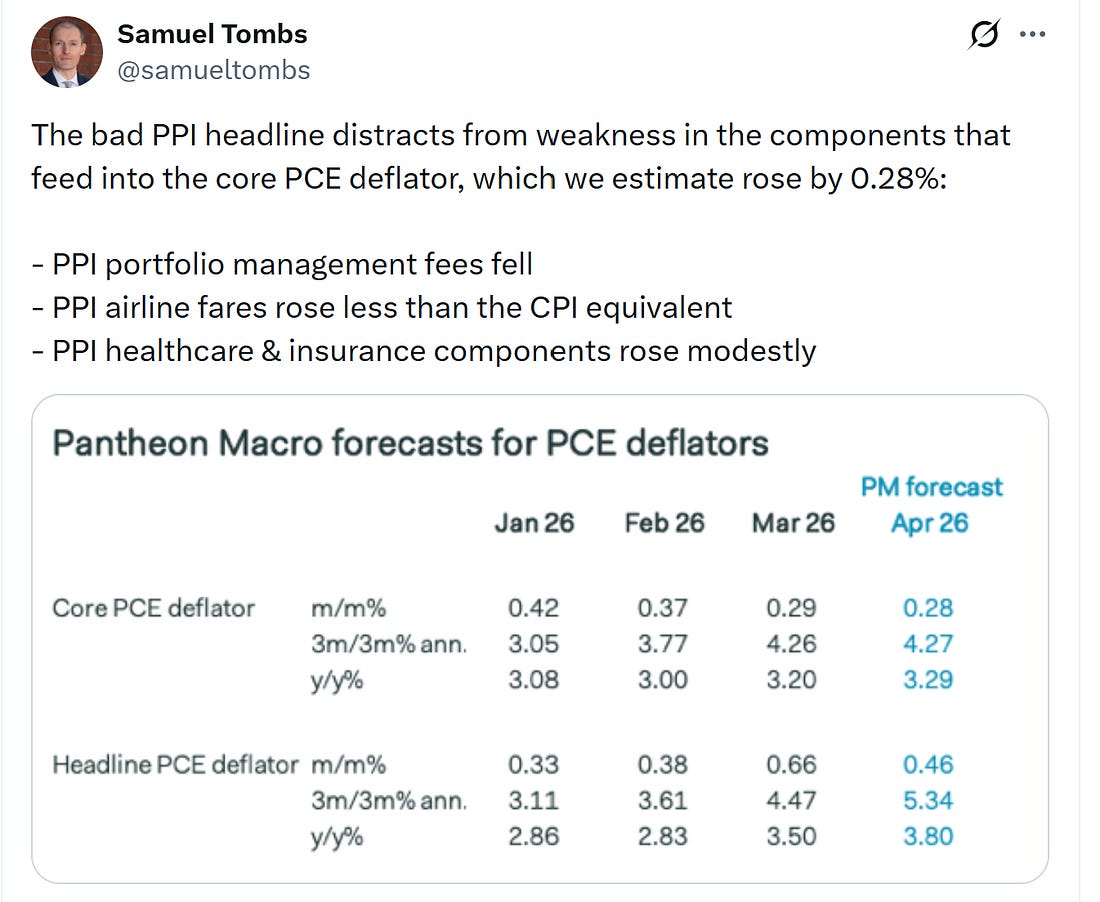

—Inflation-wise, what matters most for the Fed is the PCE deflator and based on the PPI and CPI components that feed into the PCE, it looks a bit less hot, but still too high and too sticky relative to the Fed’s target.

– I therefore am increasingly confident that, barring information pushing the other way, like a crack in the job market, the Fed’s gotta at least move to a neutral bias, if not start musing about rate hikes.

Which brings to my next topic…

Janet Yellen and I on An Important Thing Warsh is Getting Wrong

The great former Fed chair and Treasury Sec’y and the lesser yours truly penned an op-ed in the NYT yesterday. I don’t have time to go into details now, but I think it reads clearly.

Our beef with Warsh is his claim that because AI is likely to boost productivity, which allows businesses to make more outputs with the same or fewer inputs, inflationary pressures should abate, creating more space for Trumpian rate cuts.

Mr. Warsh argues. “A.I. will be a significant disinflationary force, increasing productivity and bolstering American competitiveness,” he wrote in The Wall Street Journal last fall.

But that’s only half the story. The other half—well, just look at that PPI electronic components figure above—is that AI creates a lot of demand, which pushes the other way on inflation and interest rates.

Companies expect A.I. to raise the return on the investments they make in growing their businesses, so they will increase those investments. A recent report from Moody’s Analytics showed that by the end of last year, the United States had more active and planned data centers than the rest of the world combined. Big American tech firms are expected to invest $700 billion this year. That’s over 2 percent of the country’s gross domestic product. These investment dollars will flow to construction companies building data centers, chip firms and other hardware producers, along with the workers they need to sustain the boom.

Americans who own technology stocks have done well recently, as hopes about A.I.’s future returns have buoyed investor optimism. The richest 10 percent of households saw their inflation-adjusted stock wealth appreciate by $7 trillion last year. Those wealth gains are boosting spending. Economists have found that, unsurprisingly, people who feel richer buy more, putting about 3 percent of their gains into new spending. For last year, that 3 percent translates into over $200 billion in extra spending, equivalent to roughly a fifth of the year’s increase in real spending.

Longer term, sure, faster productivity growth can be complementary to lower rates—see our discussion of the 1990s productivity surge. But nearer term, especially with the inflationary developments I document above, no one, especially an incoming Fed chair, should cherry-pick the one-half of this story that tells the part he and Trump want to hear..

More Inflation, and What Kevin Warsh is Getting Wrong Jared Berstein