Trump Administration Slams the Door on Veteran Mortgage Relief

Trump’s closure of the Veterans Affairs Servicing Purchase (VASP) plan creates financial issues for veterans who have VA mortgages which did not exist previously. Even so, in the past Trump has displayed little respect for veterans, calling them suckers and losers. He has denied the name calling, but it would be typical of him to do so. Trump has little respect for any of us . . . veterans, citizens or neither.

Mortgage Bankers Association’s Elizabeth Balce (representing the Mortgage Bankers Association), at a hearing in March of 2025 before the House Committee on Veterans’ Affairs, She warned there could be more issues if the VASP program was closed.

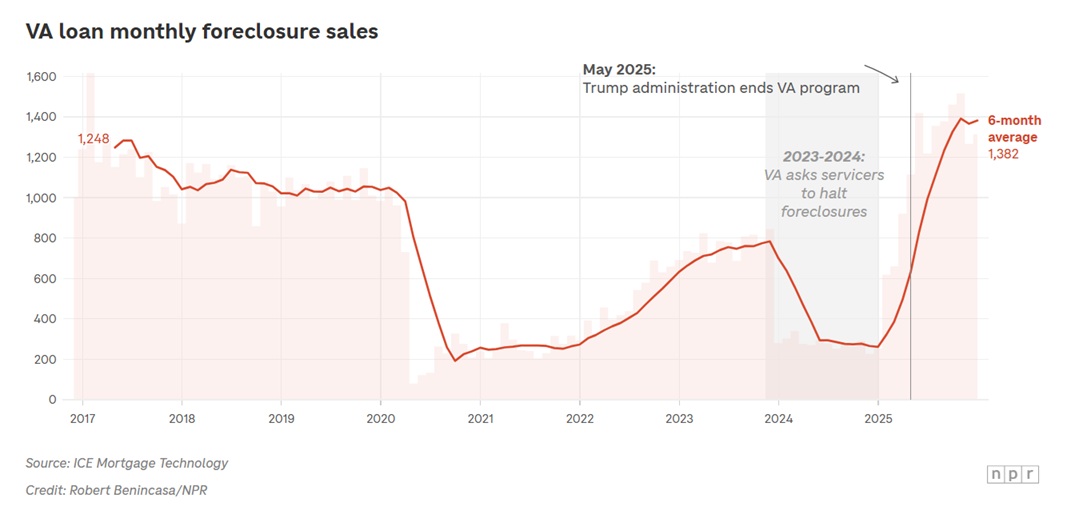

More than 10,000 veterans lost their homes to foreclosure since May of 2025. And it is only going to become worst. More veterans will be endangered. In 2025 the monthly average of foreclosures was ~1382. It is estimated; another 90,000 veterans are in danger also.

My neighbor and I both have VA mortgages. Neither of us are threatened with foreclosure.

The Republican led Congress is also doing nothing to prevent the issue caused by the Trump administration. I did have to go back through this piece and make better sense of it. It need some help to emphasize some of the issues.

“Trump’s VA killed a home loan program. Vets are now losing their homes,” NPR

The roots of the VA Home Mortgage crisis go back to a mistake made during the Biden administration. The VA had abruptly shut down a pandemic assistance program while thousands of vets were still in the middle of it. Struggling homeowners using the program to skip some mortgage payments suddenly had to pay those payments back all at once. The result was an unaffordable burden for many of them. After an NPR investigation exposed the problem, the VA halted foreclosures for a year while it rolled out a fix.

Fast forward to May 2025 . . .

As I stated earlier. more than 10,000 veterans lost their homes to foreclosure since May of last year. The Trump administration shut down a key safety net in the VA home loan program. The result of which is the highest level of foreclosures (10,000) for VA loans in a decade.

Another 90,000 vets are heading toward foreclosure also. This comes after a years-long debacle inside the Department of Veterans Affairs which has whiplashed thousands of vets between various enacted and canceled programs. It left many of them on the brink of losing their homes — often through no fault of their own.

If you do not know. Mortgage Loan backing by the VA is considered one of the most valuable benefits for military service members. It has helped millions achieve homeownership. For nearly a year now, veterans are experiencing worse, due to the lack of those protections and options which other homeowners have if they fall behind.

One attorney with the nonprofit National Consumer Law Center, Steve Sharpe said . . .

“ We should have something in place to try to stem people from losing their homes.”

No sh*t. The Trump administration was warned this would happen.

The roots of the crisis go back to a mistake made during the Biden administration which we mentioned earlier. The VA abruptly shut down a pandemic assistance program while thousands of vets were still in the middle of it. Struggling homeowners who were using the program were allowed to skip some mortgage payments. Suddenly, they were told they had to pay those payments back all at once rather than add it on to the initial mortgage. That action by the VA created an unaffordable burden for many of them.

NPR’s investigation exposed the problem; the VA halted the foreclosures for a year while it rolled out a fix. (which was probably not enough time either).

Meanwhile, Republicans in Congress, citing costs, wanted to kill that fix and replace it with something else. However, the mortgage industry last spring warned the shutting down of the program without first replacing it would be a disaster.

“Foreclosure. Period. That’s really where it’s gonna come to,” warned Elizabeth Balce. Representing the Mortgage Bankers Association at a hearing in March of 2025 before the House Committee on Veterans’ Affairs, she warned foreclosures would be the result.

The warning went unheeded. Less than two months later, the Trump administration shut down the rescue program anyway. And as noted earlier, more than 10,000 veterans lost their homes through foreclosure sales as noted by ICE Mortgage Technology, which tracks such data.

It’s unclear how many of those veterans could have avoided foreclosure through the rescue plan, called VASP, or the VA Servicing Purchase program. But mortgage industry insiders told NPR it’s clear that some of those vets had enough disability pay or other income and would have been able to keep their homes had VA not shut down the VASP program with virtually no warning.

The VA officials did not respond to NPR’s questions about why the agency shut down VASP without first replacing it with anything else or adequate warning.

Presently, 90,000 more veterans are currently behind on their mortgages or in the foreclosure process. Waking up to the issue, the VA now says it’s coming out with a new program that could help many of those vets. It will not be up and running for months leaving many to fend for themselves.

Housing and industry groups warn the new program, when operational, could still leave those vets with worse options than other homeowners. It could push their monthly payments up by hundreds of dollars a month.

Bait and switched by the VA

For one family (the Ledfords), it all started back in 2022. They had to replace their furnace and were hit with other costly home repairs. Freedom Mortgage, (their lender) told them they could get help from what was called a mortgage forbearance. The COVID-era program would let them pause making payments.

“ They told us it was for a year, and they would check in after six months,” Ledford said. “And then we would just pick up our payments at the end of the year … It felt like such a relief for us.”

She says Freedom told her the skipped payments would then be moved to the back of her loan term, to be paid later when they refinanced or sold the house.

In the wake of the pandemic, millions of Americans with other types of federally backed mortgages took advantage of such forbearance programs. But then, in October of 2022, the Biden administration shut down a key part of the VA’s forbearance program that had enabled the skipped payments to be deferred.

As a result, tens of thousands of veterans like the Ledfords were then told they suddenly had to pay that years’ worth of payments in a lump sum.

“ And we’re like, ‘wait a minute’, what?” Leann Ledford recalled.

For the Ledfords, that would have been tens of thousands of dollars. Amounts which they, and most veterans in the program, could not afford. Or the alternative was to accept a refinanced loan at the current and much higher interest rates. Rates had sharply risen from around 3% to 7% since origination. The new loan would have raised the Ledfords’ payment by about $1,000 a month. In the end, they could not afford either option.

After NPR reported in late 2023 40,000 other vets (like the Ledfords) were trapped in a similar manner to which there was no affordable way to become current on their loans. With this in mind. the VA halted the foreclosures for a year while it rolled out a rescue program. Then Trump comes on to the scene . . .

Trump’s VA kills the Biden-era fix

Once it was finally up and running by early 2025, the VA’s rescue program (VASP) was starting to save large numbers of vets and their families from foreclosure. It gave the more than 33,000 veterans who were behind on their payments new, low-cost mortgages with an interest rate of 2.5%.

Months later after VASP was fully functional and helping vets, the new Trump administration in office killed the program. On May 1, 2025, the VA abruptly did away with this safety net. The VA gave mortgage servicers and its own staff just one-week of notice. Vets who were already enrolled would keep those low-cost, affordable loans. But the door was slammed shut for any more veterans.

The Ledfords and other vets who needed the help had not managed to get enrolled yet. They called the VA. to check on the program. It was then, the Ledfords found out.

“I found out that [VASP] was ending and I called the VA loan technician, and they did not even know yet. They had to go figure out what was going on.”

Mortgage companies told NPR back then they were scrambling to enroll as many vets as they could. However, the abrupt closure of the program also caught them off guard.

“What the hell?”

Many veterans were also hurt in a different way. After VASP was shut down, vets who were mot enrolled in time felt they had no choice but to accept the offer of a loan modification. The accepted the program even though the higher interest rate meant punishingly higher payments.

Army vet Jon Henry, from Kansas City, Mo., wound up in a modified loan with monthly payments that are $380 higher than his original mortgage. Iraq veteran Henry said . . .

“It’s a struggle. Especially with everything else being inflated in the country, you know, with groceries, gas … I’m like, what the hell?”

Henry, who lives outside Kansas City, Mo., fell behind on his mortgage after losing his job managing a manufacturing plant. He’s working again now and just needed to catch up on his payments.

Those veterans who have fallen behind on their loans are in a worse position than most nonveteran homeowners. Mortgages backed by the government through Fannie Mae, Freddie Mac or FHA all have emergency options for delinquent borrowers. The options do not raise their interest rate or monthly payment. This is no longer true for veterans with loans backed by the VA.

Also, mortgage rates have been between 6% and 7% over the past 10 months since VASP shut down. The other option for a VA loan (a loan modification) could sharply raise the monthly payment as many vets originally got their loans when rates were lower. Many veterans were forced to choose between selling their house, getting foreclosed on, or accepting a much higher-cost mortgage.

Shante Benfatto told NPR, “It hurts paying $3,200 a month. Shante served in Afghanistan and is rated 100% disabled by the VA. She and her husband fell behind on payments when he was between jobs. They tried for months to get into the VASP program but that their lender did not get all the paperwork done before the VA suddenly shut the program down. After receiving letters threatening foreclosure, the Benfattos reluctantly accepted a new modified mortgage with payments about $300 a month higher than the original loan.

“We’re paying late because we can’t afford to pay the extra money until the end of the month, until she gets her disability,” said her husband, Mark. The late fees add an additional $105 to their monthly mortgage bill.

Some vets have seen their payments go up by a lot more. For example . . .

Air Force vet in Port Charlotte, Fla., Jerome Thomas was hit with a payment that is now $800 higher every month. His interest rate more than doubled to 6.8%. His lender told him he either had to agree to the new rate or be foreclosed. He felt forced into the higher-cost loan.

”I told them I can’t afford to pay it.” Thomas, who’s lived in his house for 10 years, told NPR. And as he predicted, he’s now behind on that modified loan and is receiving letters warning he’s headed into foreclosure.

“ I got my three kids in here, I’ve got the wife, she’s a teacher … it’s bad.”

“We’re paying late because we can’t afford to pay the extra money until the end of the month, until she gets her disability,” said her husband, Mark. The late fees add an additional $105 to their monthly mortgage bill. (AB: Maybe it is just my luck? I have always been able to rearrange dates if needed.)

Even when the Trump administration’s new loan program is up and running, it will not help vets like Thomas, Benfatto, or Henry who were already forced to accept loans with higher interest rates. It will not lower their payments back down to where they were before. In theory, some vets could refinance if mortgage rates drop sharply, but rates have been rising again.

The VA’s new fix

The Trump administration’s new program, when it’s up and running, will work by allowing vets to take their missed payments and move them to the back of their loan term. So, they’ll get to keep their current mortgage and interest rate. That should be a big help to vets who have a relatively low rate.

There’s a qualifier in the current draft. The way it’s written, the VA is telling mortgage companies that if a new, modified loan at a higher interest rate only raises a veteran’s monthly payment by up to 15%, they must place vets into that more costly loan. (AB: To me this is excessive, uncalled for, and a gift to the bank, etc.)

A veteran with a $2,000 monthly mortgage payment could still be pushed into a modified loan raising their payment by up to $300 a month. And they would not be given the option of moving their missed payments to the back of their loan and keeping their original, lower-cost mortgage.

The mortgage industry is telling the VA that that doesn’t make any sense.

“As drafted, Veterans will continue to have worse options than similarly situated non-Veterans,” Pete Mills, an executive with the Mortgage Bankers Association, wrote in a letter to the VA. (AB: When a banker is claiming this is a bad option, it must be taken as such. This is punishment.)

“Payment reduction is the most important driver of modification performance, and the current policy will lead to higher redefault rates,” Mills said. The association, along with housing groups, is recommending the VA put a loan with a higher payment at the very bottom of its so-called waterfall of options for homeowners who are behind on payments.

“The VA should restructure the waterfall to only allow increased monthly payments as a last resort,” Mills said.

Housing advocates are also pushing the VA to ask the mortgage industry to hold off foreclosing on vets until its new program gets up and running in a few months. That would buy time for the tens of thousands of vets who are already behind on their loans or in the foreclosure process.

“We’re talking about a heck of a lot of folks,” said Sharpe, with the National Consumer Law Center.

Eviction looms

It’s already too late for Leann Ledford, her combat-disabled husband, and their 10-year-old son in Spokane, Wash. Freedom Mortgage sold their house in a foreclosure sale, and it’s now owned by the VA and they’re being told they need to leave.

Ledford’s husband has spiraled. He’s having seizures again, and the issue made him so stressed he did not want to be interviewed for this story. “ It has really impacted him, and he is really struggling,” she said.

The VA said in a statement that it has helped thousands of vets to avoid foreclosure, but it did not offer specifics. The fall-back reasoning? VA press secretary Pete Kasperowicz wrote,

“Per federal law, VA’s home loan program is based on the premise that while Veterans may need some assistance, they must generally be able to make their mortgage payments.”

The Ledfords, who receive $3,971 a month in Ledford’s husband’s disability pay, say they could have afforded mortgage payments under the VASP program. And they could have afforded their original mortgage with its $1,447 monthly payment, had VA’s new program been up and running and allowed them to move their missed payments to the back of their loan term. But because VA killed VASP before setting up the new program, they were stranded without either option.

AB: Passing the buck . . . Pete Kasperowicz said.

“VA worked tirelessly with the Ledford family to help keep them in their home. However, they were nearly four years behind on their mortgage payment, and the decision to foreclose on their mortgage was made by Freedom Mortgage.”

Freedom Mortgage declined repeated requests for an interview or statement.

That VA statement ignores the fact that the Ledfords, like many other vets, were not allowed to resume making mortgage payments after a series of the VA’s own missteps trapped them in a bureaucratic quagmire. They were told to just keep applying for help through a loss mitigation process that dragged on for years and in the end, never offered them any actual assistance.

The VA did not respond to questions about whether it could do anything to save the Ledfords from losing their home, since the VA now owns it following the foreclosure sale. The only offer from VA so far was $3,500 to vacate the house in what’s known as “cash for keys.”

The Ledfords have been told that to get even that much help, they need to vacate their home by April 3.

In its written statement, the VA said it stands ready to assist the Ledfords with health care services as needed. Maybe they can offer lower cost housing too?

Never had my back, now they don’t have yours

I’ve always been a tad proud of that bad conduct dishonorable discharge, it took some doing to get kicked out of that Army. I ain’t missing anything I never had

So much for the socialism of the military …

Ten Bears:

I know you for what you are today. The past is past.