Improving Social Security Options

Dean Baker: Don’t Buy the Scare About Social Security. “The increase in spending on Social Security from 2033 to 2034 (measured as a share of GDP) is 0.03 percentage points. That would be less than 1.0 percent of the Pentagon’s budget. This is the extent of the increased economic burden in the year the trust fund faces depletion.”

This is one way of looking at making Social Security solvent for one-year making it able to continue paying full benefits for 2033 -2024. I am not sure what the next year would involve. The foregoing proposed solution by Dean Baker is to do a fix Social Security at the last moment. And this would be typical of Congress to wait till the last moment to do anything. But then, this si where we are today. The last moment even though it may be eight years.

A total fix as proposed by Dale Coberly and Bruce Webb was to tweak the withholding tax for Social Security one tenth of one percent ten years or more before full payment insolvency. Unfortunately, we have a Congress and other interests who are more interested in making this a political crisis. . . . And wait till it becomes a greater issue. Since we passed 10 years before the fund dissipates, that tweak would now be more than one tenth of one percent each year.

Social Security tax today covers $176,000 in income for both employee and employer as a 6.2% tax for each. Ideally, one way to improve solvency is also to raise the amount of income subject to the tax. At this time, that would still not be enough. I can not tell you the solution at this time; but I suspect an increase in taxation is needed beside an increase in what is taxable.

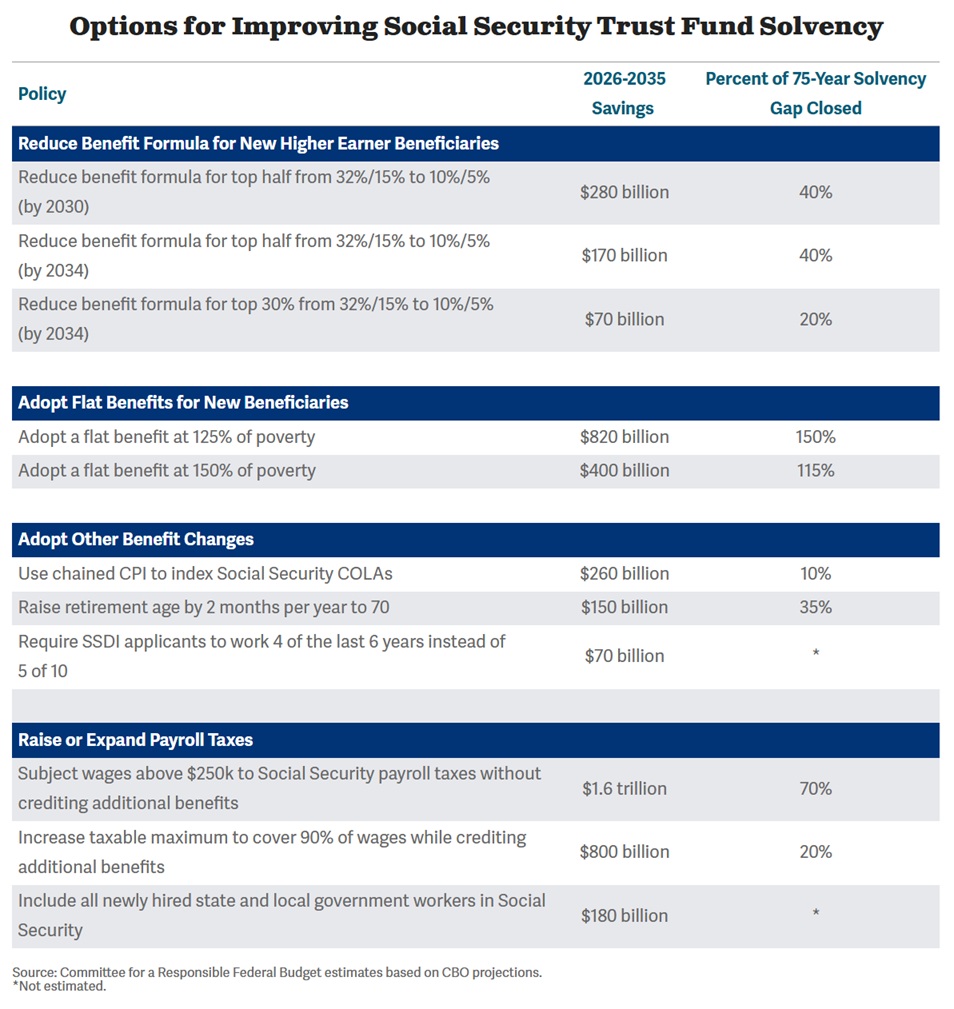

Some partial solutions . . .

It would appear an increase in wages taxable is a form of solvency or some combination. I have left this open-ended so as to elicit conversation. The only limit I stress being “doing nothing is not a solution.

“CBO’s Budget Options to Improve Social Security Solvency,” Committee for a Responsible Federal Budget

Other Information that may differ: “The Social Security Taxable Maximum,” Bipartisan Policy Center

More Information: “Social Security: The Gem of American Economic Policy,” CEPR

“Social Security Isn’t Going Broke: What the 2025 Report Really Says,” CEPR

Mr. Haskell,

Most of your solutions represent wealth transfers or reductions in benefits.

The big problems is Social Security is structured as a financing vehicle for the federal deficit and does not resemble a long term pension fund (which it is). A better solution is to purchase 10-15% in major equity indices (like pension funds) which would better reflect inflation adjusted outlays (and give the market a boost which would have a salutary effect on capital gains tax remittance)

@Phil,

You obviously don’t know anything about Social Security. Social Security in not a pension fund, nor was it designed to be. It is retirement insurance. Your solution will result in wealth transfers to Wall Street and reduction in benefits due to load and stock market volatility.

Mr. Stone:

Social Security is “not” an investment tool. Its original design was pay as you go as there were no reserve funds to payout in the beginning. It does well just doing such with funds being held in treasuries. Wall Street investing blew themselves up in 2008 with the help of Greenspan. There is no reason to believe they would do better in 2025. Whereas the proposed solution is and was accepted as a solution. Except, it had to be started 10 years out.

Most of the issues today are tax breaks for the upper 5% income brackets thereby creating larger deficits such as Trumps 2017 tax break which DID NOT pay for itself and is being further extended going farther out for a small percentage of tax payers in the upper 5%. A few charts to explain:

The 2017 Trump Tax Law Was Skewed to the Rich, Expensive, and Failed to Deliver on Its Promises

Since 1974 and 3 years after I left the military and picked up my first degree, I went into companies and sorted their demand and inventory issues out for management that could not plan their way out of a paper bag. They were too enamored with their offices, corporate cars, golf outings while I was on the floor or doing their overall demand and inventory plans coupled to manufacturing capacity to meet the overall business plans.

2008 was a great time, wasn’t it? Greenspan let Wall Street almost destroy the economy and the nation with their irrational exuberance. And here we are today, Trump and Republicans are driving the nation with greater debt at the expense of citizens and what are you asking me?

Mr. Stone:

Some charts to help you understand where this is all heading.

@Terry,

tl;dr: tariffs are merely regressive consumption taxes, intended to partially offset deficits caused by tax cuts for the 1% and corporations. Hold on to your wallet.

Joel, you can label the old-age benefit as insurance, but the actual transactions are very similar to pensions. You hand over funds to SSA, another party hands over some more (if not self-employed) and SSA promises to send you monthly checks based on what was contributed in your name and when you want to start taking it. There is no obligation to demonstrate any particular valid insured claim. You just get old enough and say you want it to start. I would say the biggest difference between pensions and Social Security is that pensions are enforceable contracts. Social Security is whatever Congress says it is at any moment.

@Eric,

You can label the old-age benefit as pensions, but the actual program is identical to retirement insurance.

“. . .and SSA promises to send you monthly checks based on what was contributed in your name and when you want to start taking it.”

Wrong. SSA promises nothing. SSA makes projections about benefits, not promises.

SS has been reliable for 90 years. My dad’s pension was converted to a 401k when he retired, without his consent. His private company pension was not an enforceable contract. Pensions can experience insolvency or even termination. Whether state pensions are considered enforceable contracts is a complex issue that varies significantly by state.

Joel:

True on the projections and then adjusts to meet demand supposedly in a timely manner.

No Joel, SSA promises to send you a calculable amount based on current law and they send you an estimate of what they believe that could be based on the data they have. What they can’t do is look ahead and tell you they are going to ease back 2% so as to give Congress some more time to act. But if Congress says, hey cut back 2% so we have some more time to do something better, you’ll get what Congress says. As to your father’s pension, I did not say that the contract did not allow conversions or even that the pension-fund might not breach, just that a contract existed between the parties. You don’t have a contract with SSA. SSA follows a law that grants you a certain benefit, but SSA obligation is not to you, but to the law. It’s great that SS has been reliable and popular. I do not think Congress will radically change the system, but that does not make it a contract.

Wrong, Eric. SSA doesn’t promise benefits. It projects benefits. Those projections are based on current law, an estimate of what they believe that could be based on the data they have. That’s what a projection means. That’s not what a promise means.