Some Explanation for the Deficits – Quit Cutting Taxes

It is not spending causing the issues as the young Trump boasts. It is the tax cuts which have imbalanced credits to debits causing the deficits. What Republican’s promised would happen, failed to happen. The 2017 tax cuts did not stimulate the economy enough (not at all) to balance out spending to receipts. Since the tax cuts failed to improve tax receipts as claimed, taxes should be allowed to return. Since the TCJA did not pay for itself, the TCJA was passed using Reconciliation; everything which means everything that was a tax cut reverts back to pre-TCJA what it was.

Trump, his silly sons, and Republicans do not want to play now that time is up in 2025.

Furthermore, the Bush Tax Breaks have added to the deficits.

On Angry Bear, this should not be so damn difficult to understand.

Tax Cuts Are PRIMARILY RESPONSIBLE for the Increasing Debt Ratio

Some Brief History

The issue of deficit spending goes back a number of years. After WWII, the federal debt declined from 106% of GDP to 25% of GDP. A very brief recital of what has taken place through several Presidental schemes. A better recital can be found here: Tax Cuts Are Primarily Responsible for the Increasing Debt Ratio, Center for American Progress

Fiscal policy in the postwar era

In the 34 years after 1946, the federal debt declined from 106 percent of gross domestic product (GDP) to just 25 percent, despite the federal government’s running deficits in 26 of those years. The debt ratio declined for two reasons. First, the government ran a “primary,” or noninterest, surplus in a large majority of those years. This means that, not counting interest payments, the budget was in surplus. Second, the economic growth rate exceeded the Treasury interest rate in a large majority of those years. These two factors—along with the starting debt ratio—are the levers that control debt ratio sustainability.7 With a primary balance, the growth rate need only match the Treasury interest rate for the debt ratio to be stable. The presence of both primary surpluses and growth rates that exceeded the Treasury interest rate created significant downward pressure on the debt ratio.8

The nation’s fiscal pictured changed in 1981 when President Ronald Reagan enacted the largest tax cut in U.S. history,9 reducing revenues by the equivalent of $19 trillion over a decade in today’s terms. Although Congress raised taxes10 in many of the subsequent years of the Reagan administration to claw back close to half the revenue loss,11 the equivalent of $10 trillion of the president’s 1981 tax cut remained.

The Congressional Budget Office’s (CBO’s) last long-term budget outlook before those tax cuts were largely permanently extended15 projected that revenues would be higher than noninterest spending for each of the 65 years that its extended baseline covered.16 In other words, right up until before the Bush tax cuts were made permanent, the CBO was projecting that, even with an aging population and ever-growing health care costs, revenues were nonetheless expected to keep up with program costs. However, in the next year, that was no longer the case.17 As a result of the massive tax cut, the CBO projected that revenues would no longer keep up due to being cut so drastically and, as a result, the debt ratio would rise indefinitely.

The Bush Tax Cuts

The George W. Bush administration, empowered by a trifecta in 2001, enacted sweeping tax cuts that will have cost more than $8 trillion by the end of fiscal year 2023. The tax cuts lowered personal income tax rates across the board, both for labor income and for capital gains, and they significantly increased the untaxed portion of estates and lowered the estate tax rate. These changes were enormously tilted toward the rich and wealthy.23 While these increases were paired with an expansion of the child tax credit and the earned income tax credit, the total package gave significantly greater savings to the wealthy and also made the U.S. tax code significantly more regressive.24 In 2013, a significant majority of the Bush tax cuts were made permanent with bipartisan support, locking in lower tax rates and deep cuts to the estate tax.25 These changes led to a significantly more regressive tax code than existed before the Bush tax cuts were enacted, and one that brought in vastly less revenue.

President Donald Trump’s signature tax bill,26 enacted when Republicans gained control of the White House and both houses of Congress in 2017, will have cost roughly $1.7 trillion by the end of fiscal year 2023. These tax cuts reduced personal income tax rates and permanently lowered the corporate tax rate, among other changes. Despite being paired with a further expansion of the child tax credit, the 2017 changes also largely benefited the wealthy, once again making the U.S. tax code significantly more regressive.27

Taken together, the Bush tax cuts, their bipartisan extensions, and the Trump tax cuts, have cost $10 trillion since their creation and are responsible for 57 percent of the increase in the debt ratio since then. They are responsible for more than 90 percent of the increase in the debt ratio if you exclude the one-time costs for responding to COVID-19 and the Great Recession. While these one-time costs increased the level of debt, they did nothing to affect the trajectory of the debt ratio. With or without them, the United States would currently have stable debt, albeit potentially at a higher level, despite rising spending.28 In other words, these legislative changes—the Bush and Trump tax cuts—are responsible for more than 90 percent of the change in the trajectory of the debt ratio to date (see Figure 3) and will grow to be responsible for more than 100 percent of the debt ratio increase in the future. They are thus entirely responsible for the fiscal gap—the magnitude of the reduction in the primary deficit needed to stabilize the debt ratio over the long run.29 The current fiscal gap is roughly 2.4 percent of GDP. Thus, maintaining a stable debt-to-GDP ratio over the long run would require the primary deficit as a percentage of GDP to average 2.4 percent less over the period. Because the costs of the Bush tax cuts, their extensions, and the Trump tax cuts—on average, roughly 3.8 percent of GDP over the period30—exceeds the fiscal gap, without them, all else being equal, debt as a percentage of the economy would decline indefinitely.31

The Trump Tax Cuts

President Donald Trump’s signature tax bill,26 enacted when Republicans gained control of the White House and both houses of Congress in 2017, will have cost roughly $1.7 trillion by the end of fiscal year 2023. These tax cuts reduced personal income tax rates and permanently lowered the corporate tax rate, among other changes. Despite being paired with a further expansion of the child tax credit, the 2017 changes also largely benefited the wealthy, once again making the U.S. tax code significantly more regressive.27

Taken together, the Bush tax cuts, their bipartisan extensions, and the Trump tax cuts, have cost $10 trillion since their creation and are responsible for 57 percent of the increase in the debt ratio since then. They are responsible for more than 90 percent of the increase in the debt ratio if you exclude the one-time costs for responding to COVID-19 and the Great Recession. While these one-time costs increased the level of debt, they did nothing to affect the trajectory of the debt ratio. With or without them, the United States would currently have stable debt, albeit potentially at a higher level, despite rising spending.28

In other words, these legislative changes—the Bush and Trump tax cuts—are responsible for more than 90 percent of the change in the trajectory of the debt ratio to date (see Figure 3) and will grow to be responsible for more than 100 percent of the debt ratio increase in the future. They are thus entirely responsible for the fiscal gap—the magnitude of the reduction in the primary deficit needed to stabilize the debt ratio over the long run.29 The current fiscal gap is roughly 2.4 percent of GDP. Thus, maintaining a stable debt-to-GDP ratio over the long run would require the primary deficit as a percentage of GDP to average 2.4 percent less over the period. Because the costs of the Bush tax cuts, their extensions, and the Trump tax cuts—on average, roughly 3.8 percent of GDP over the period30—exceeds the fiscal gap, without them, all else being equal, debt as a percentage of the economy would decline indefinitely.31

Try and plant the “raising tax revenue by increased rates” tree now.

The best time to plant this tree was 2009. The second best was 2021.

paddy:

You have no idea what you are talking about. The tax cuts did NOT produce the revenue the promotors of the tax breaks claimed. Everyone done by a Republican President has failed miserably. Then we get the son of a president, who has no political or government stature lecture us on spending. The issue was created by cutting taxes which was supported by a lie, such action would create more revenue.

We would return to what should have been left alone in the first place. The heaviest part would fall upon those who were undeserving of the bulk of that 2017 tax break. They lined their pockets at the expense of the public.

There is no planting a seed. This was passed under RECONCILIATION. It failed so everything goes back to what it was.

Then you come out here and wish to lecture me?

It is hard to get elected when one side is promising tax cuts and maintaining spending while the other side is promoting tax increases (back to the original tax rate). The effects of the tax cuts are not immediate or even in the next five years but long term (which is now) they could almost be fatal.

It helps in governing if both sides are are mature and responsible. Now we have a president that will promote “tax cuts that will pay for themselves”. There probably is one somewhere in the universe but it hasn’t shown up on this planet (or at least in this hemisphere).

An interesting chart. The “one-time” Great Recession impact continues pretty uniform through 2019 when COVID is added to it. So what does “one-time” encompass if it is still there about a decade later? Will one-time COVID still be a big item in 2029? The “one-time” contributions eyeball about 4x Trump tax cuts. Maybe a plan could be to cut those and end Trump tax cuts as a package.

I linked the Center for American Progress article in one of my comments in Angry Bear. I wonder if that is what brought it to your attention.

Besides the Bush Tax Cuts, between 50 – 75% of the Covid spending was unnecessary, wasteful, and fraudulent. We should have focused on maintaining personal income for those out of work instead of paying businesses to keep people employed who probably would have stayed employed. This Covid spending at least wasn’t permanent like the Bush tax cuts.

My solution to the debt problem in general (it would have been easier to do at the beginning of Biden’s term rather than now or next year) would be to reverse the Bush and Trump tax cuts and then if there was still a deficit then cut spending. Republicans might have gone for that at the beginning of Biden’s term.

@Pre,

When was the last time the GOP supported raising taxes?

According to Grover Norquist’s group, Americans for Tax Reform, 42 Senators and 191 House members have signed the pledge to not raise taxes.

About ATR’s Taxpayer Protection Pledge

@Jim,

Do you know of any Republicans who have stated a willingness to raise taxes?

Jim:

Lets get it straight. Spending is not the issue as much as the reduction of taxes which left a deficit as the cuts did not improve government revenue. With the TCJA repeal, one is not increasing taxes. They are restoring the tax base which was cut with the idea, the thought, the hope, the lie, etc, government revenue would increase. IT DID NOT!

As passing such breaks under reconciliation, if the cut does NOT pay for itself, the tax base goes back to what it was pre-taxcut.

George H.W. Bush raised taxes. He lost to Clinton afterwards.

I am not saying that it would have worked but you have to support reasonable policies and let the other side vote them down. Taxes were at a reasonable level to get most things done then.

Republicans always say that Democrats would continue to spend more even if taxes are raised (although Republicans spend more even if taxes are cut) so call their bluff and make a commitment to not increase spending and balance any remaining deficit once taxes got restored to the pre-Bush taxcut era.

It probably wouldn’t have worked but at least you can make your case to the voters.

@Pre,

Sorry, I meant present-day Republicans, not historical Republicans.

Bush signed the bill to raise taxes in 1990. We’re in 2024, 34 years later. Bush was right to call supply-side economics “voo-doo economics,” and he paid the price for his honesty. Have any present-day Republican politicians rebelled against the borrow-and-spend creed of the GOP?

Pre:

ok, I will bite.

George Bush was faced with a similar issue as what would have plagued Biden if he were in office in 2025. George Bush the Elder had a deficit issue also and he decided to address it. Address it by going back to the old tax structure which brought a balance or closer to it. This was precisely how we would end up in 2025 unless a Republican Congress makes the tax break permanent. Your story is not complete as the one factor not being said here is it was not as much a tax increase as it was a return to the prior tax base.

After a year and a half in office, the 41st president courageously (though belatedly) decided to address the long-postponed budget deficit problem that he had inherited. He entered into difficult negotiations with the Congressional leadership. The Democrats had the majority in both houses of Congress and they refused to agree to restrain domestic spending unless taxes also contributed to the budget package. Thus in June 1990 Bush admitted that any agreement to cut the deficit would require not just spending restraint but also tax increases. This was universally viewed as a retraction of his “no new taxes” pledge. The taxes that were raised were in fact old taxes, but that was considered just a technicality. On October 8, the House and Senate finally agreed on a budget plan (narrowly avoiding a government shutdown).

The lesson from George H.W. Bush’s tax reversal

Pre:

I suspect you are quoting Congressman Posey. I will use this one objection of a bunch he has: An expansion of Obamacare that subsidizes health care for wealthier families,

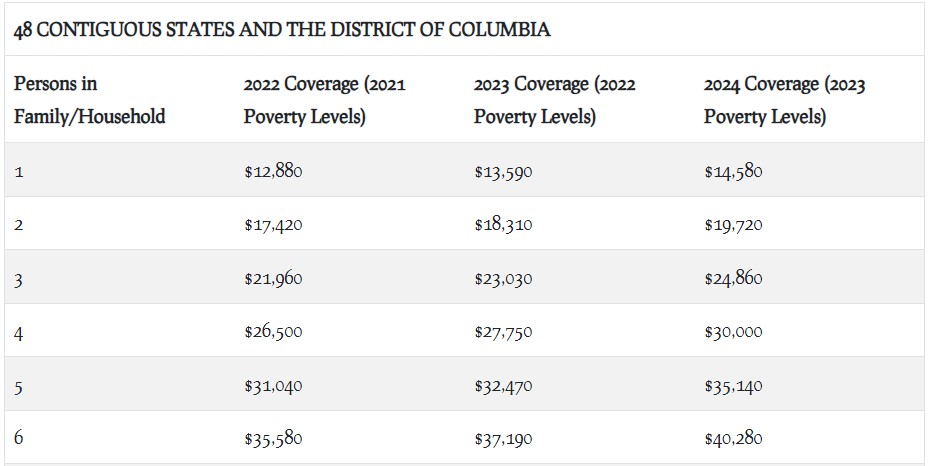

The ACA was expanded to cover people over 400% of FPL That is not wealthy.

https://angrybearblog.com/wp-content/uploads/2024/12/Poverty-Levels-for-the-ACA-in-2024.jpg

Poverty Levels for the ACA in 2024

How is that Wealthy??

You leave much open ended without supplying much needed support for what you say. You have to support your commentary with other than an opinion.