Boom in U.S. Construction of Manufacturing Facilities

This piece is a review on what is happening in increasing manufacturing capacity for computer, electronic, and electrical manufacturing. Where I am, there is increasing builds of facilities for each of those products. That being around the Phoenix area. One facility they have been working on for two years now and it appears to be near the end. Much of this is automated and probably using much Labor. A Semiconductor process is basically growing wafer, populated the slices, and layering or packaging. I have oversimplified it so add to it.

TSMC Arizona’s first fab will operate it’s leading-edge semiconductor process technology (N4 process) starting production in the first half of 2025. The second fab will utilize be present leading edge N3 and N2 process technology and be operational in 2028. The recently announced third fab will manufacture chips using 2nm or even more advanced process technology, with production starting by the end of the decade.

The exciting part of this being more technological manufacturing in the US and employing advanced technology to build such product again in the United States. Browse a used excavator for sale by Boom & Bucket to find reliable equipment at competitive prices.

All sponsored and accomplished by a president claimed to be on the verge of senility.

“Unpacking the Boom in U.S. Construction of Manufacturing Facilities”

U.S. Department of the Treasury

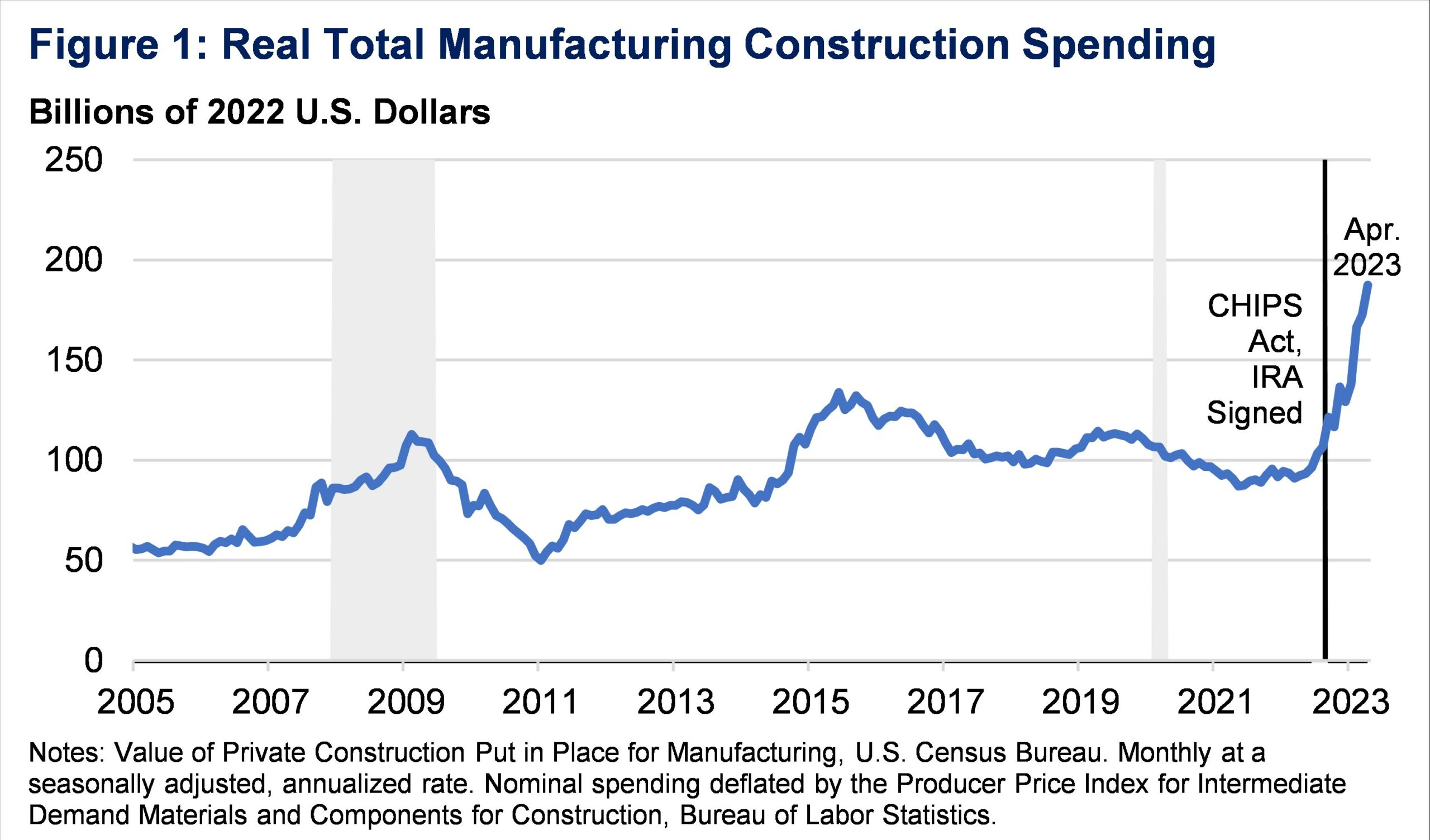

The United States has experienced a surge in construction spending for manufacturing facilities. Real manufacturing construction spending has doubled since the end of 2021 (Figure 1). The surge comes in a supportive policy environment for manufacturing construction: the Infrastructure Investment and Jobs Act (IIJA), Inflation Reduction Act (IRA), and CHIPS Act providing direct funding and tax incentives for public and private manufacturing construction.

Exploring the surge along three key dimensions:

- The boom or need of home-based technology is principally driving the construction of computer, electronic, and electrical manufacturing. A relatively small share of manufacturing construction over the past few decades and now a dominant component.

- Manufacturing construction is one element of a broader increase in U.S. non-residential construction spending. This along side new building for public and private infrastructure following the IIJA. The manufacturing surge has not crowded out other types of construction spending, which generally continues to strengthen.

- Finally, we put the trend in international context. While it can be difficult to compare such granular data across countries, the surge appears to be uniquely American and not mirrored in other advanced economies.

Decomposing the Surge

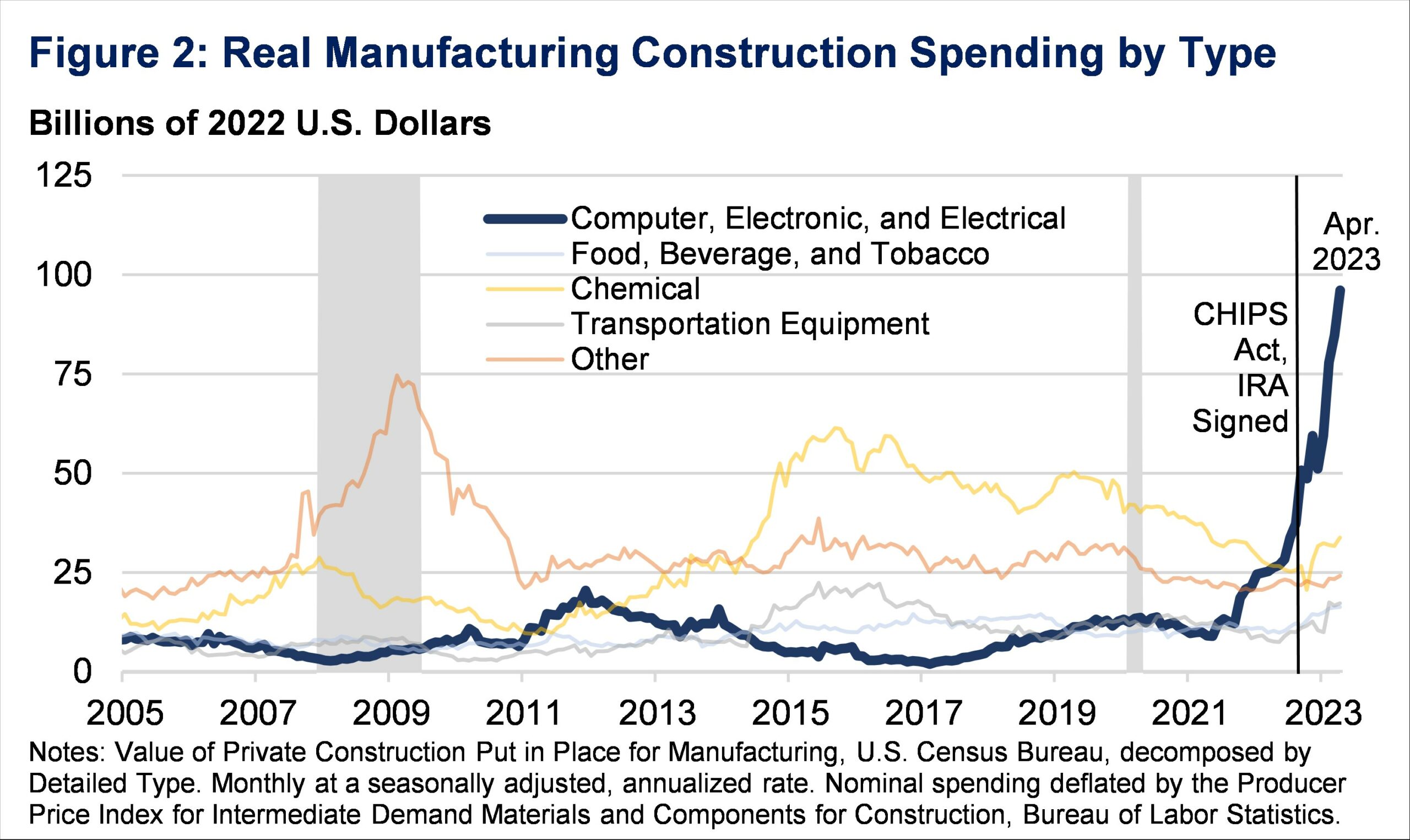

Within real construction spending on manufacturing, most of the growth has been driven by computer, electronics, and electrical manufacturing needs. Since the beginning of 2022, real spending on construction for this specific type of manufacturing capability has nearly quadrupled (Figure 2).

The adjustment for price increases is particularly important here. Construction costs have risen quickly in recent years. Therefore, nominal spending growth should not be misconstrued or mistaken as increased physical construction. But by considering deflated measures as we do here, it is clear that the surge is a real one (see Appendix for a more detailed discussion of our choice of deflator).

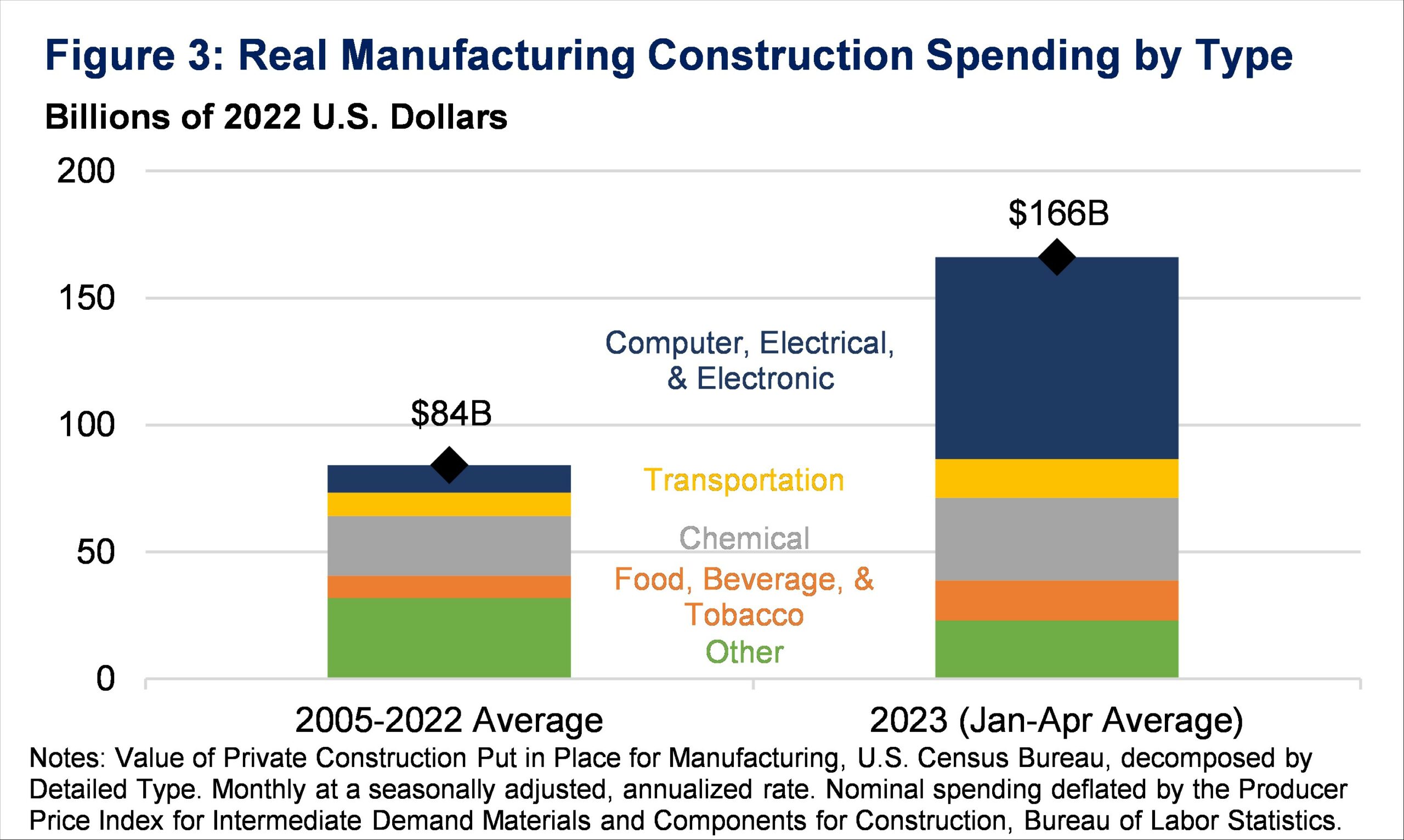

Today, the computer/electronic segment is the dominant component of U.S. manufacturing construction. Importantly, the boom in this segment has not been offset by reduced spending on other manufacturing construction segments, which are largely consistent with long-term levels (Figure 3). In fact, construction for chemical, transportation, and food/beverage manufacturing is also up from 2022, albeit much less than the computer/electronic sector.

This rise in the spending began in the months before the CHIPS Act passed, as many factors beyond policy contribute to construction spending. Still, the legislation has played a critical part in continuing and expanding this trend. In particular, private sector analysts have recognized the connection between the growth in construction for electronics manufacturing and the CHIPS Act. Bank of America notes this rise came “potentially on the back of ongoing construction of semiconductor factories as part of the CHIPS Act.” According to Deutsche Bank Research, 18 new chipmaking facilities will have started construction between 2021 and 2023. The Semiconductor Industry Association reports, over 50 new semiconductor ecosystem projects built in the wake of the CHIPS Act.

The macroeconomic situation, policy implementation, and a range of other conditions will continue to shape construction manufacturing spending in the months and years to come. While today’s striking trend may cool, the CHIPS Act has fostered an ongoing opportunity for investment in this sector.

Broader U.S. Non-Residential Construction Spending

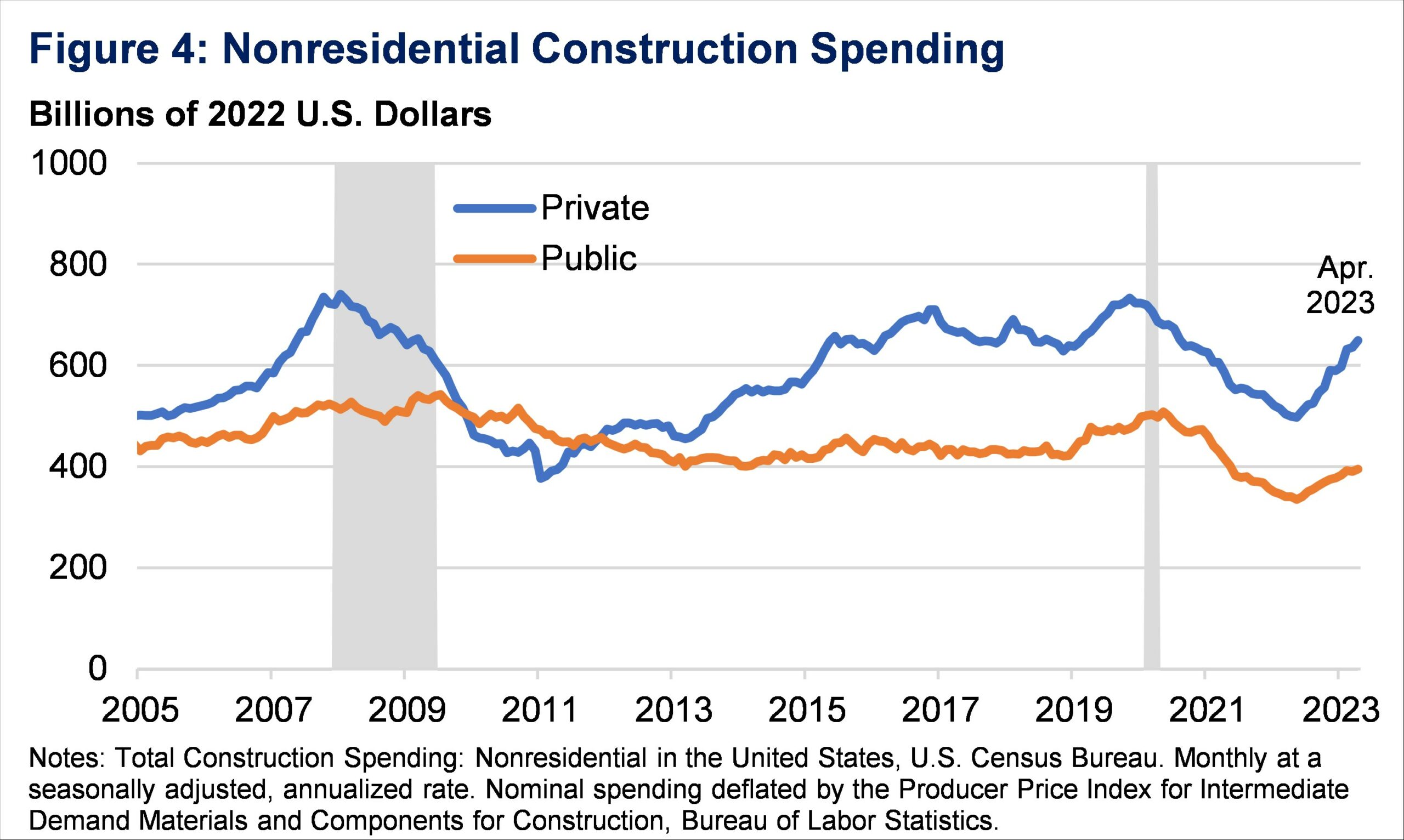

While manufacturing is the most eye-popping component of construction spending, overall real nonresidential construction spending has increased by about 15 percent from November 2021, when the President signed the IIJA, to April 2023. Real public spending, which increased by 7 percent, did not crowd out real private spending, which increased by nearly 20 percent (Figure 4). Moreover, as more IIJA projects come online and break ground, more public and private dollars will go toward our public infrastructure.

Under the hood, specific components of construction spending, beyond manufacturing, have also had substantial increases driven by recent legislation. The IIJA authorized the federal government to distribute new funds to state and local governments for infrastructure needs tied to roads, bridges, public transit, water, and broadband. That funding has started translating to spending.

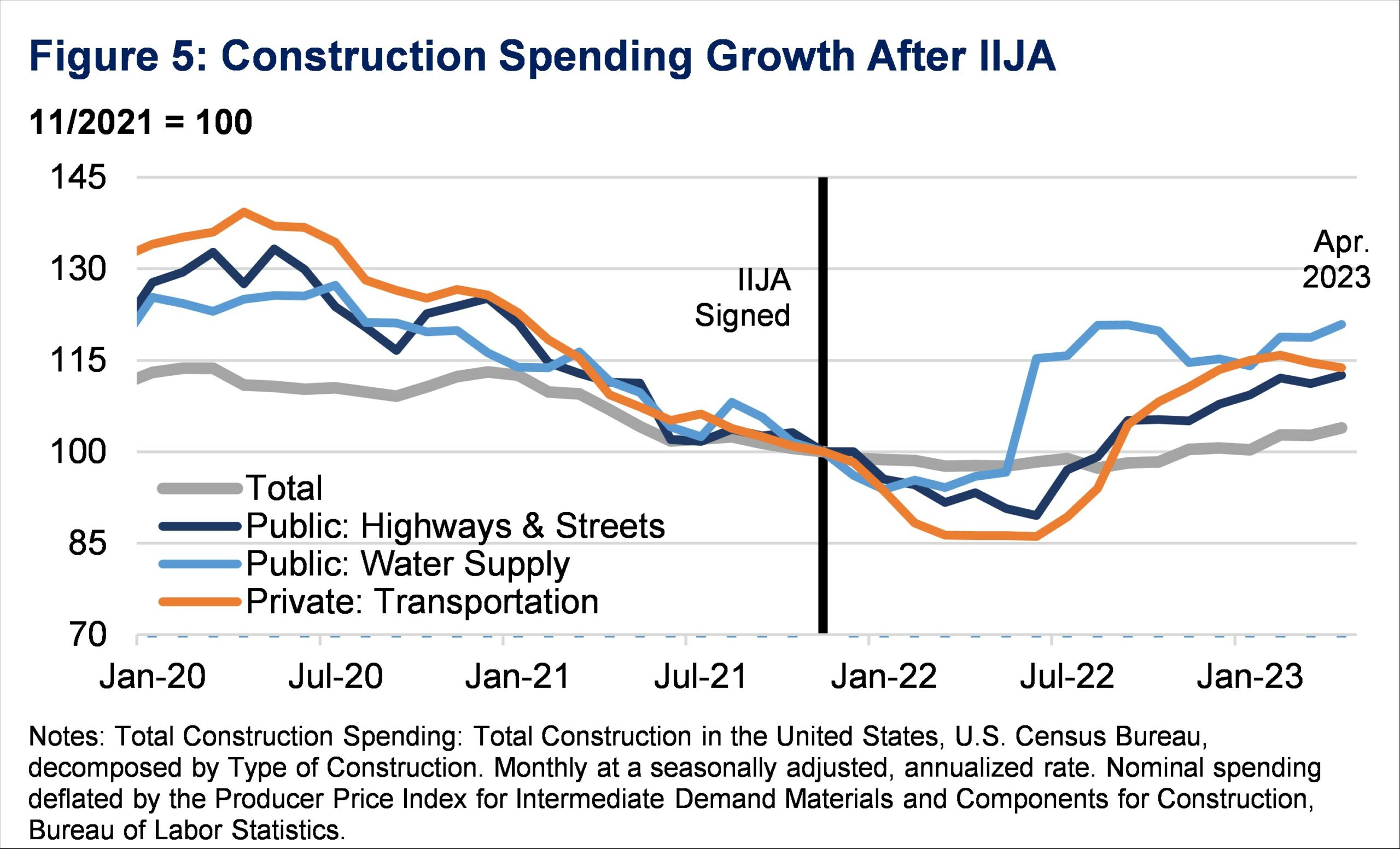

Since the bill’s passage, construction spending on these areas has outpaced total construction spending. For example, total construction spending has increased about 4 percent, while public construction spending on the water supply has increased by over 20 percent (Figure 5). The IIJA delivered more than $50 billion to the EPA to improve the nation’s drinking water, wastewater, and stormwater infrastructure. Public spending on highways and streets has also increased by about 13 percent, as the IIJA funds roads, bridges, and major projects with over $110 billion over five years.

Again, the legislation increased public spending but has not crowded out private spending. Real private spending on transportation construction has grown by nearly 14 percent since the President signed the IIJA. The legislation increased the available Private Activity Bonds (PABs) authority from $15 to $30 billion. PABs, allocated by the Secretary of Transportation, incentivize private sector investment in U.S. transportation infrastructure. Across over 40 projects, the Department of Transportation has approved nearly $17 billion and allocated an additional $2.8 billion in PABs.

Such investments harness government resources to increase productive capacity. This being a central goal of Secretary Yellen’s Modern Supply-Side Economics policy framework. Private manufacturing for semiconductors, with funding from the CHIPS Act, expand the U.S. economy’s footprint in a sector vital for today and tomorrow’s technologies. Increased public expenditure on our infrastructure from the IIJA enables a better functioning, more resilient economy. Tax incentives from the IRA address the historically overlooked market failure of climate change, ushering in a green energy transition that steers the country toward sustainable growth. Each of these projects addresses market failures to increase inputs to production which fuels long-run growth.

Acronym Explanation: The Infrastructure Investment and Jobs Act (IIJA), aka Bipartisan Infrastructure Law (BIL), was signed into law by President Biden on November 15, 2021. The law authorizes $1.2 trillion for transportation and infrastructure spending with $550 billion of that figure going toward “new” investments and programs. This bipartisan law strengthens PHMSA’s safety authority and includes many provisions that will help PHMSA fulfill its mission of protecting people and the environment by advancing the safe transportation of energy and other hazardous materials.

This is great information, which should be shouted by the current party seeking re-election. This construction spending on manufacturing represents ‘making America a great manufacturing country again’. In 2026 and 2027 this wise investment will pay dividends.

Is the growth and decay of asset valuations in the asset-debt macroeconomic system relegated to an elegantly simple fractal self-organization mathematical process?

Observe the valuation patterns over the next 12-14 months.

The current short term valuation decay is obvious with a broken trend line and nonlinear gapped lower low and with US manufacturing and employment data shouting contraction and recession.

(China, Japan, and Europe are arguably in much worse shape than the US).

The global mathematical initial decay fractal is a 1 July 2024 8/13/7 of 13/?8-9 day decay fractal series.

Time will tell.

Gary:

Every time you write something, I begin to wonder “what the hell did I miss 40-something years ago” when I was picking up an MA (speaking of your site). My expertise is more along the lines of manufacturing and the resulting supply chain in and out of a facility. Something so simple to learn about, put in place, and do and yet so often neglected in planning. Manufacturing and supply chain was my livelihood.

Planning a trip back to Chicago in the next couple of months to visit my econ prof., my associate in consulting for Ingersoll Engineers, and an attorney friend. The three of us are getting up in years. I do not feel like flying. My 2015 VW Passat has 68,000 miles on it and I feel the need to make the journey out of AZ to the Chicago area across country. I want to see the countryside one more time.

If you ever feel a need to write oon a topic most of AB’s readers would understand, we would love to have you.

Bill