US Debt, Problems, and Fixes

Discussing US Debt looked interesting enough to post on Angry Bear. I do not agree with the proposed fixes as I believe there are other fixes which would resolve the issues mentioned. Perhaps you have better ideas?

Addressing Rising US Debt

by Karen Dynan

Econofact,

The Issue:

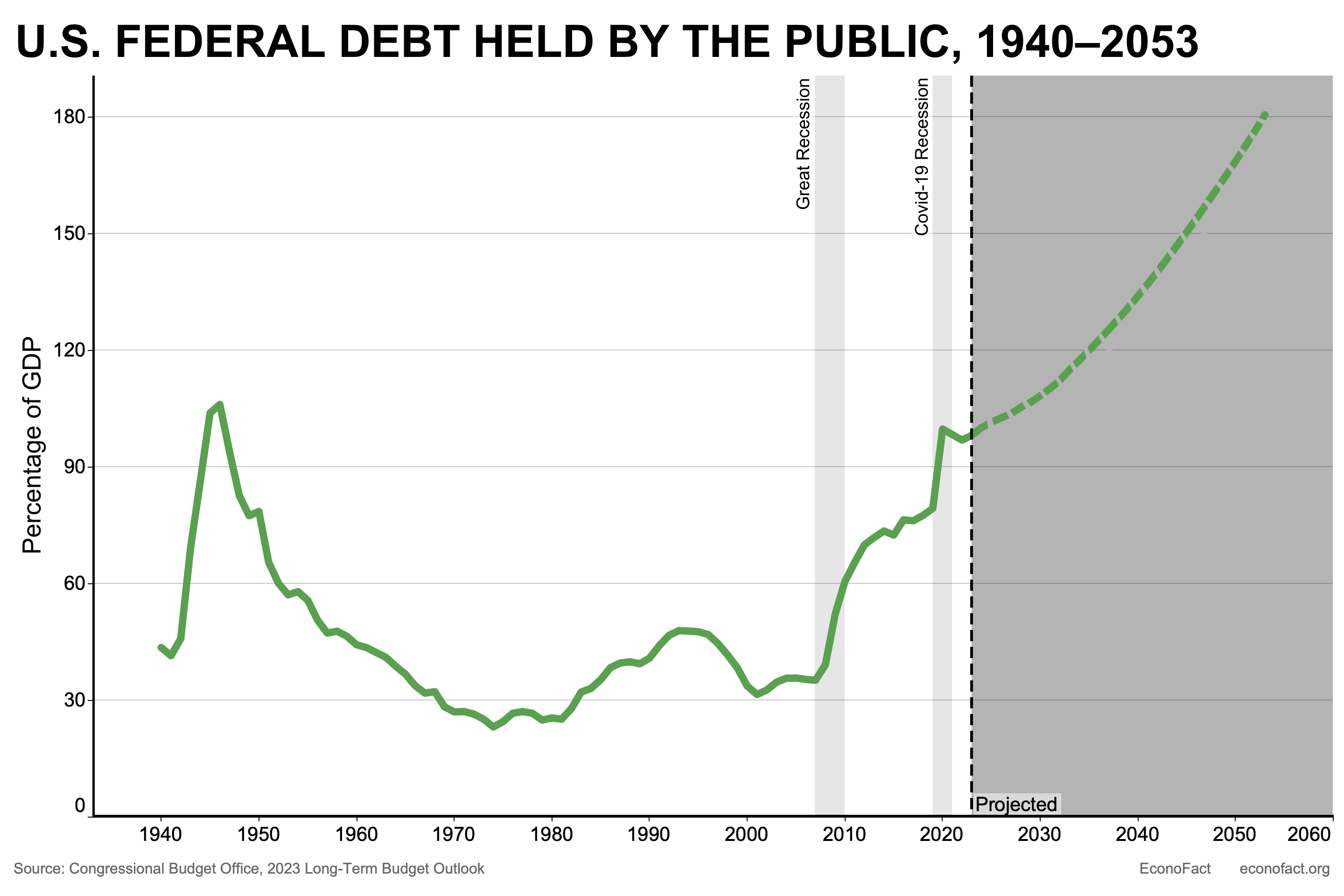

United States Federal debt rose sharply after the Great Recession. At 98% of gross domestic product (GDP) in 2023, it is close to its highest level ever. Under current policy, the federal debt is expected to continue rising over the next three decades to reach levels well above any historical experience. It holds true even under optimistic assumptions about future economic conditions. To keep the federal debt from ballooning to the levels currently predicted, a closer alignment of government spending and revenues needs to occur in coming years. Changes in policy substantially narrowing the federal deficit going forward may have economic and political disadvantages. Changes will be needed, as unprecedented levels of government debt impose significant economic costs and risks.

The Facts:

Negative economic shocks and policy changes over the past two decades have shifted current and projected levels of federal debt to higher levels.

The United States has seen two significant adverse shocks to economic activity in the 21st century. The deep and prolonged Great Recession beginning in 2007 as a result of the global US financial crisis and the sharp economic downturn that followed the onset of the COVID-19 pandemic in early 2020. These episodes led to drops in economic activity and lower tax revenues and, at the same time. Increases in federal spending on recovery programs contributed. A lasting downshift in government revenues brought about by major changes in tax policy still contributes to higher levels of debt. The changes in tax policy include the extension of tax cuts from early in the first decade of the 2000s and tax cuts enacted in the Tax Cuts and Jobs Act of 2017. If the provisions of the 2017 tax cuts scheduled to expire in the next few years were to be extended, the projected path of tax revenues would shift further down. An increase between $400 billion and $500 billion per year in the late 2020s and early 2030s.

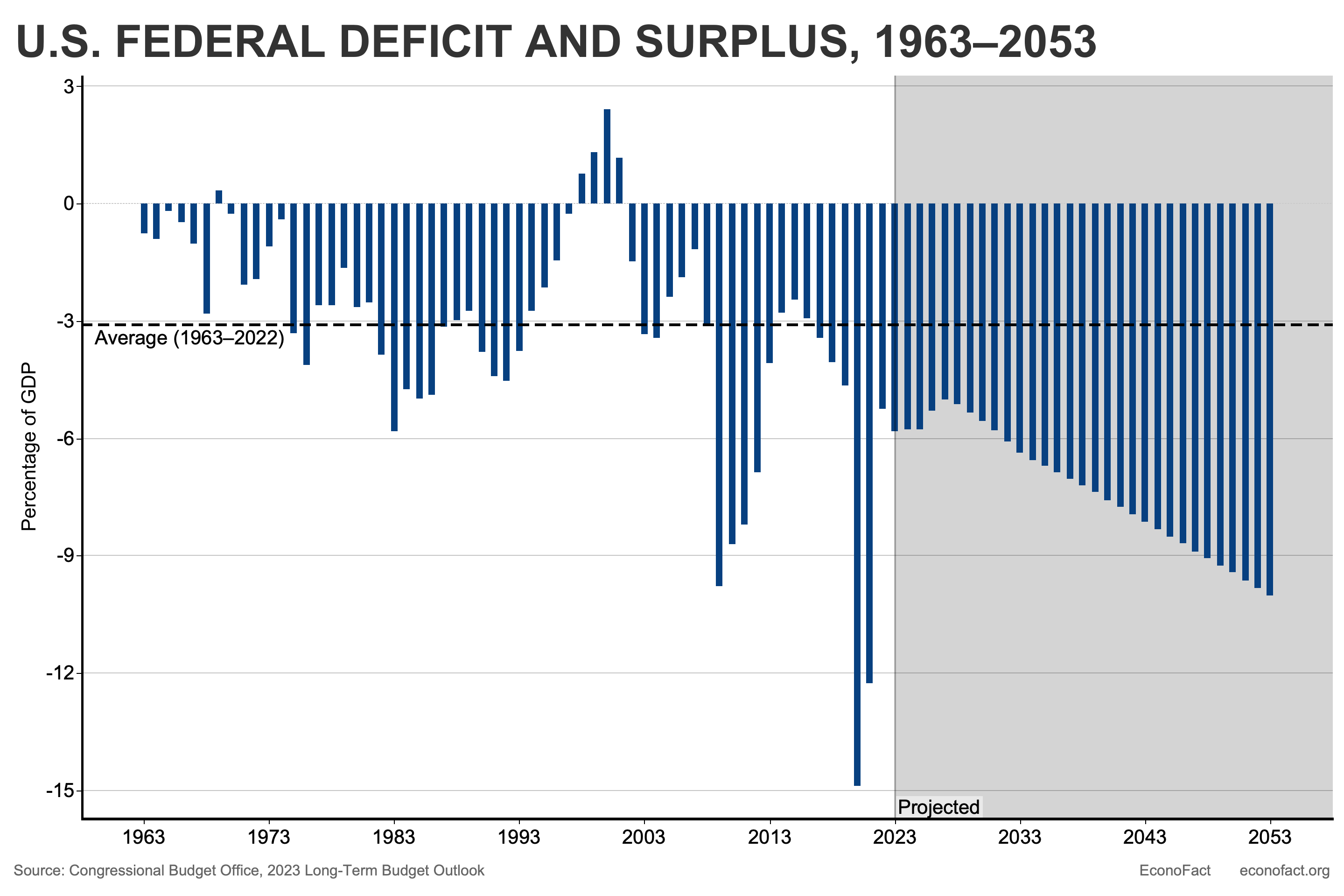

Behind the projected surge in US federal debt over the next three decades is an expected increase of the federal budget deficit, which is currently high and projected to rise steeply under existing law.

Briefly; federal budget deficit occurs when federal government spending exceeds its revenues. The government needs to borrow in order to make up the difference. The federal debt is the accumulation of federal budget deficits over time. It is not uncommon for the US federal government to have a budget deficit. Having deficits modest in size is sustainable given growth in the economy. However, the current size of the federal deficit, while smaller than its pandemic highs, is large by historical standards (chart below). Moreover, the budget deficit is projected to climb much higher over the next three decades, reaching 10% of GDP by 2053.

The aging US population is a key factor contributing to higher projected government spending.

The proportion of the US population aged 65 and older grew from about 12% in the first decade of the 2000s to 17% in 2023. Projections indicate a further increase to 22% by 2050. An increasing older population will require significant federal support for both income and health care (see here and here). The Congressional Budget Office (CBO) has projections using current policy. By 2053, the CBO projects Social Security outlays will rise by nearly 1% of GDP. It also projects spending on major federal healthcare programs, including Medicare, will rise by 3% of GDP. Spending on Social Security and federal health care programs will amount to 15% of GDP by 2053. This increase will drive the primary deficit (the deficit excluding interest payments on our existing debt) higher.

Ongoing large primary deficits, along with an already-high level of debt and interest costs, lead to a dramatic snowball effect over time.

A high level of accumulated debt and higher interest rates mean interest payments on our debt are an increasing part of federal spending. Ongoing large primary deficits generate additional debt leading to mounting interest costs. This in turn leads to an additional increase in the total deficit and debt. Under the assumption government borrowing rates remain at levels somewhat higher than the levels of the late 2010s, the CBO estimates that higher interest costs will push up the overall deficit by an additional 4% of GDP by 2053. Absent policy changes, this dynamic will push the deficit and debt ever higher even in the years beyond CBO’s window.

These structural challenges mean that even “good luck” with economic developments that would mitigate the debt burden, such as high productivity or low interest rates, will not put the debt on a sustainable path.

Growth Estimates of federal debt over time depend on assumptions about trends in productivity and interest rates and other factors. Higher-than-expected productivity growth leads to higher GDP growth, which in turn reduces the burden of higher debt. However, even under the most optimistic scenario for productivity growth estimated by the CBO, the federal debt would increase to 137% of GDP by 2053 or well above the historical range. The same is true for the most optimistic interest rate scenario considered by the CBO. An interest rate path that starts 5 basis points lower than baseline in 2023, with the gap then growing by 5 basis points per year, still results in the federal debt held by the public in 2053 increasing to 143 percent of GDP (see here). These analyses underscore that even favorable macroeconomic outcomes are very unlikely to change the conclusion that federal debt is on an unsustainable path.

The projected path of US federal debt presents significant economic costs and risks.

First, increased borrowing by the government crowds out borrowing by households and businesses. The competition for funds drives up interest rates, making it more expensive for individuals and businesses to borrow. As a result, private investment in productive capital decreases, leading to lower future output and national income. Second, elevated borrowing raises the risk of a fiscal crisis. If investors become reluctant to lend money to the government because they fear the debt will not be repaid, government borrowing rates can rise suddenly as prospective lenders demand more compensation to hold government debt. Finally, higher debt also comes with the costs of reduced “fiscal space,” meaning a limited capacity to increase the budget deficit, even temporarily, without endangering the access of a country’s government to financial markets or the sustainability of its debt. A lack of fiscal space constrains a country’s ability to effectively address sudden domestic needs, such as economic crises or pandemics, as well as international threats.

Many of the policy changes that could help put the debt on a sustainable path have disadvantages, so choices will need to be made carefully.

Many of our federal spending programs serve important purposes such as promoting economic growth, fostering economic mobility, mitigating hardship, and protecting national security. Large increases in taxes would not be popular, and some such changes could lead people to work less, save less, invest less, and innovate less.

What this Means:

The challenge posed by high and rising federal debt is significant but manageable as a matter of economics. For example, CBO projects that a combination of reductions in noninterest spending and increases in taxes that reduce the deficit by an average of 2.8% of GDP in coming decades would be expected to keep the ratio of debt to GDP at its current level; alternatively, reducing the deficit by an average of 3.3% of GDP over the 2027 to 2052 period (which would balance the primary deficit) would result in a gradual decline in the debt relative to GDP over time. Policymakers will need to carefully weigh the economic tradeoffs as they make the needed changes to spending and taxes. But the biggest obstacle to addressing high and rising federal debt may be political. Promises not to touch substantial key federal spending programs or to raise taxes are popular, but they cannot all be realized if we are to put the budget on a sustainable path.

How are we supposed to find this person credible at all when she includes Social Security as a driver of future primary deficits? One thing I think I learned here is that Social Security has nothing to do with deficits. Unless, maybe that’s merely a convenient way of describing the accounting that forces recognition of higher deficits onto other accounts of the budget. But that’s not possible, right?

Eric:

If you borrow from the Social Security Trust funds, you have to repay it. The only ones who have not been repaying it are those who are on Medicare Advantage plans. I would argue MA Plans are not the same as Medicare as they involve commercial enterprises..

Bill

I don’t understand what you are saying here. Repaying money borrowed from SS comes from the Federal budget (income taxes) the same as repaying any money they borrow (by selling bonds). I don’t think it matters whether the people paying the general taxes are on Medicare, Medicare Advantage, or even Social Security itself..if they have taxable income. I know it sounds to people like they are paying a tax on a tax. But they have got it exactly backwards. They are paying a tax on income just like everyone else. With the exception of some tax boondoggles like Roth IRA’s all income from interest (savings accounts, stock market gains, private pensions)…is taxed…”progressively” SS income is fairly low, so it won’t get taxed unless your other income raises your total income to a level that is taxed…just like the income tax itself. very low incomes don’t pay much in taxes. i over-simplified this a bit, because the complications don’t change the basic fact.

No, you are wrong and we did talk about this early on. I guess I can not count on you remembering. MA plans are being subsidized by Social Security/HI funds. Otherwise MA could not compete with Medicare.

Bill

I understand that Medicare is paying for “Medicare Advantage” overcharges and that is a problem. But it does not affect Social Security, which I regard as OASDI, These are separate programs.

Dale:

I will report on it.

Eric

It’s not strictly legal. Congress passed a law when it was convenient for them to NOT count Social Security when counting the Federal deficit. I think this was when SS was in surplus counting it in the budget REDUCED the apparent deficit. But when the SS “balance” was counted over the next 75 years, the “actuarial deficit” could be counted as part of the Debt and make it look larger, thus enabling the eternal wailing about the Debt, both so we had to cut social spending, and had to cut Social Security because…the Debt. My guess is that most of the Congress believes this, but it is dishonest accounting.

Meanwhile, the SS Trust Fund IS money the Congress has borrowed from SS and legally has to be paid back..and is being paid back as we speak. But calling it a “cause” of the debt is like telling your grandma who lent you money for college that her asking you to pay her back is her “adding to your debt.”

So what congress is doing is trying to welsh on its debt to grandma…by not only not paying her back, but by planning to continue to collect the payroll tax but cutting benefits..prevent “the young” from saving in the safest way available for their own future needs. Lotsa good money to be made servicing those “private accounts.”

“But the biggest obstacle to addressing high and rising federal debt may be political.” Really? Who knew?

“Promises not to … raise taxes are popular.” Actually proposals to raise taxes on certain groups particularly privileged by the tax cuts of the last 60 years are quite popular. The issue is not popularity but political feasibility, since the most likely candidates for increased taxes also happen to have enormous political clout, probably as a result of income from those tax cuts being partially recycled back into political donations and lobbyists’ salaries.

An apt characterization of the author: “It is Difficult to Get a Man to Understand something When His Salary Depends Upon His Not Understanding It”

John:

I have not researched the author to make a comment on the authors statements. Was I happy with the authors commentary in places? No. I do think it is important we all see what others or the opposition are thinking so as to frame our arguments. So, I left it alone. It is important you see what is being thought and the basis for it.

I get grief from others over my opposition to using external taxation of businesses and solely the rich to fund Social Security. By doing so, you make Social Security just like any other Congressional program. A program which may need additional funding on a yearly basis or so and come up for a vote on increases or reductions in funding. Social Security should not be subject to the whims of those who have political influence such as those in Congress and those who can fund the election of Congressional Reps and Senators who can be influenced by donations. And that is the direction the author is taking as well as Robert Reich, Merrill Goozner, etc.

Increasing the income taxable level for Social Security makes sense as income has increased and in perspective they are paying less than what they would have when we take this into perspective, However, this remains within the Social Security Medicare taxation and not subject to yearly congressional agreements. I do not understand why our people of influence do not understand the danger of solely taxing the rich to fund Social Security. I believe they know the danger, they have to know the danger, because repeatedly Congressional politicians’ paints beneficiaries of its bills as scofflaws. The 1 tenth of 1% (and coberly may have a different amount as well as income base) increase in tax for Social Security equates to 70-something cents a week on an income of $40,000 annually.

As far as this: “It is Difficult to Get a Man to Understand something When His Salary Depends Upon His Not Understanding It.” Women will make the same decision when they are in upper management and only see the forest and not the trees.

Bill

mostly true. the problem is simple greed. Both the Right and the Left only see what’s in it for them. The people in general don’t understand a thing, but they also complain bitterly about taxes..so if you get them to think of SS as a “tax” (instead of “the safest way to save your money and insure yourself against poverty when you can no longer work”) you can get them to feel like SS is a bad deal and demand “the rich pay thier fair share,” which turns out not to be fair at all, but the fastest way to kill SS by turning it onto welfare.

FDR understod this. He had to overrule his own social security commission (it wasn’t called that) in order to keep them from turning SS into welfare, because that’s the only way they can think.

We still see this on the Left. They think only in terms of making the rich pay for the poor even if that is the surest way to motivate the rich to NOT pay for anything that helps the poor…even if it helps them (the rich) in the long run.

The Right, of course, is even more blind. The only thing they can think of is getting the last nickle on the table. They call it “winning.”

“…and some such changes could lead people to work less, save less, invest less, and innovate less.” And which people would that be?

So Elon Musk would not be who he is if he had to pay a more realistic tax on his $42 Billion pay package. I’m sure that Hedge fund managers would stop their ‘essential’ work if carried interest loopholes are eliminated. Or how about those living off their investments? Do they stop saving/investing.

Tax rates have been shown to have minor (if at all) impact on innovation. Economically the trade-off of a lower budget deficit to possible changes to innovation/savings/investment which ‘could’ (but probably won’t) happen.

I am encouraged by the comments here (so far). It seems people recognize that Social security is not a driver of the Federal Deficit/National Deficit. And that the only sane answer to the Debt problem is to raise taxes…yes, “on the rich,” but that does not mean “make the rich pay for Social Security,” which would both be unfair (the rich already pay for Social Security as much as the benefit they get from it…and enough so that their SS taxes DO help those with the lowest incomes) and lay SS open to all the politics that ordinary welfare is subject to. Social Security has worked for over eighty years because “we paid for it ourselves.”

The article quoted demonstrates it’s stupidity by comlaining that SS costs will go up 1% of GDP over the next 75 years. Think about it ONE PERCENT to pay for food and shelter for 25% of the population…that is ALL of the people too old to work (however long they are going to live)…and without regard to the fact that all of those people will be paying for their Social SEcurity themselves…paying in advance through pay as you go financing… just like every other savings and investment plans, You cannot cut the COST of Social Security exceot by killing off the elderly. One way or another the cost of living longer will come out of “the economy.” SS is just a way of seeing that that cost is paid (in advance) by the beneficiaries themselves and not subject to the damage of inflation, market wins and losses, or political games.

because Congress ignored the warning of “short range financial inadequacy” to the SS program (meaning that taxes were not high enough to pay for needed benefits), it is no longer possible for the one tenth of one percent increases triggered by that warning to rasie the payroll tax enough to avoid depletion of the Trust Fund. BUT and increase in the tax of TWO tents of a percent per year will avoid depletion of the Trust Fund and make Social Security solvent for the forseeable future. Two tenths of a percent per year amounts to a payroll tax increase of two dollars per week per year while incomes are going up one full percent per year..about ten dollars per week per year.

I am sorry that I use words like “stupid” to describe ignoring or failing to understand these facts. But the work I use for Congress, and the higly paid “non-partisan experts” who ignore them is “dishonest.”

Pardon my bad manners if you can. But don’t let your dislike of me keep you from understanding the facts.

Dale Coberly:

I left the argument on SS to you mostly as you can detail it more than I can. I am very disappointed with some who mostly write on the economics issue correctly but fail to do so on fixing Social Security correctly. The same as Admiral Ackbar in Star Wars said; “It’s a trap.”

To fund Social Security using funds secured through Social Security taxes would cause it to be negotiable every budget time. The fix is clear for Social Security. The real is well known and those having more bandwidth than us insist on bring Social Security into the budget and “It is a trap.”

Dale:

I was not going to edit that commentary. The author like others believe there is only one solution which is the income tax or taxing the wealthy. And this method would be contested every congressional session or we might get another 2017 tax act which did not pay for itself in economic returns. I left it as it is. These people have issues seeing other solutions which you have advocated.

also please pardon my typos. the WORD I use (not the work i use)

and “raise” not “rasie”

AbeS

yes. the rich have been saying this for a few hundred years: you can’t pay workers more because they would just drink it up and not show up for work on monday. but you can’t pay the rich less, because they would just sulk and not “create jobs.”Because, after all, if you “could have” made two million dollars on a deal, why would you bother if you would only make one million?”

a furthe note on “stupid”: i try to use the word only to describe an idea or an argument. that does not mean that i think the PERSON is stupid.

the ordinary person cannot help think in terms of the ideas and arguments he has been hearing all his life. eventually these ideas are almost welded, literally, into his brain and even when he is arguing against them, they are still there unconsciouly directing his thoughts into the familiar channels.

i like to think that given a chance and somehow “forced to think” most people would understand what is really going on, and not just the words about it.

i will say, i have known some nice people who really can’t seem to bend their minds around some concepts that are strange to them. I think they just need more time and a good reason to think harder.

but i wasn’t a very good math teacher even when that was my job and there was nobody lying to my students. will say they had gotten out of the habit of really wanting to learn.

or it might just take a Roosevelt to make them understand. and a recent memory of the Great Depression instead of 80 years of prosperity made possible by the very reforms that today’s politicians want to deform.