No signs of the international political crisis creating any Western economic crisis at this point

No signs of the international political crisis creating any Western economic crisis at this point

No important economic data today, and no significant COVID updates over the weekend. Let me make a few comments and then turn to the bond market, particularly as it reflects the international situation.

I have no more insight into the Ukraine matter than probably any other well informed average citizen. It feels like the closest Russia and the US have come to actual war since the Cuban Missile Crisis in 1962 – but only in relative terms. I have a recollection back then of walking to the bus stop in the morning, and being told by my older sibling unit that the world might end at noon. I think I simply nodded and accepted that this was something that I had been taught in religion classes would happen sooner or later anyway.

In the Korean War, Soviet pilots apparently did fly North Korean jets. And during Vietnam, Russia and China openly armed the North Vietnamese. Similarly, after the Russian invasion of Afghanistan in 1979, the US openly aided the Taliban. None of those acts on either side were consistent with neutrality, but were accepted as better than open conflict between the superpowers.

This is a little different, both in location and magnitude. Ukraine is not just adjacent to Russia, but was formerly part of the USSR itself. The closest Cold War analogy is Cuba. There was the matter of the Bay of Pigs, but after that the US accepted that Cuba was allied with the USSR – so long as the USSR did not equip Cuba with any offensive weapons, and as those of us alive at the time well recall, nuclear weapons in particular.

As to magnitude, Putin was clearly told there would be severe sanctions, but obviously he had concluded, based on his experience as to Chechnya and Crimea, that they would be manageable. Instead, the entire West, including all of Europe both via the EU and NATO, as well as the US, Canada, and Japan as well, have essentially declared economic war on Russia. Whether or not Russia ultimately succeeds in militarily conquering Ukraine, Russia’s complete freeze-out from the Western economic and financial system is going to remain.

It is all well and good to argue what Putin “rationally” ought to do or not do, but as I always remind people, that didn’t exactly work out with Kaiser Wilhelm II 100 years ago. Let us hope that cool heads prevail.

As I write this, the 10 year Treasury bond is trading at roughly 1.89%. This is about 0.10% below where it was trading most of last week. It is the beneficiary of what traders call a “flight to safety,” i.e., pulling back from more risky assets to ride out the storm in a more plain, but stable, investment. This is about in the middle of its range over the past five years:

No particular sign of stress there.

Meanwhile, gas prices have risen to $3.62/gallon, according to gas buddy, continuing their rise from $3.25 just two months ago. This will inflict some further stress on consumers, but it is hardly the makings of a crisis:

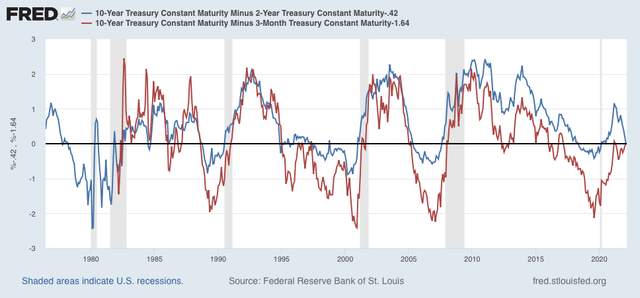

Finally, as I commented in my weekly article at Seeking Alpha, while the 10 year minus 2 year Treasury spread is down to 0.42%, not only is that not a yield curve inversion, it isn’t even particularly tight looked at from a longer-term perspective. Below is the 10 minus 2 year spread (blue), minus -0.42% so that the current spread shows as 0, and the 10 year minus 3 months spread (red), currently 1.64%, normed to 0 as well:

Similar spreads occurred anywhere from 2 to 7 years before the next recession over the past 40+ years.

So, at least economically speaking, the current international political crisis is not showing signs of spilling over into any kind of economic crisis in the West.

Did I read in Joe Biden’s State of the Union speech last night a comment that the way out of this mess, the way “back to normal,” is to spend more? To produce more, consume more?

To go shopping !?

I thought overproduction, overconsumption, too much of a good thing, was what got us here …

TB,

Read again, but produce more was about producing stuff we get from offshore to shorten the supply chain. Consume more was about public infrastructure first, but also healthcare, childcare, education, and green replacements for oil. Not to just fawn over Ordinary Joe, then I must admit that although his list of wants was terrific there was an extraordinary shortfall in the area of political feasibility without a windfall midterm election to geld the Elephant Party opposition; not that there is anything wrong with that.

OK, I see it. I think I might of knee-jerked.

I am disturbed by this notion the “normal” everybody wants to get back to is the way it used to be. The belly of the beast has been exposed; the cans kicked to the end of the road. We have stuff on our plates that can’t be dealt with the way we used to. Maybe we shouldn’t let the disaster capitalists capitalize on what has been a disaster. Maybe we should capitalize on it to make some changes.

TB,

Understood and agreed.

First there is them and then we still have to confront Pogo’s Lament “We have met the enemy and it are us.”

TB

No, to the last sentence.

Just leave it lay for all to see, an abject disaster?

Like Project Just Let Them Speak?

TB,

I believe that works much better for them than it does for us. Preserving the status quo involves little new information and no real plan. When the status quo speaks then it has the wind of widespread priors at its back.

OTOH, change is just the opposite. The problem with change is that it has not happened yet making it mysterious at best and really easy to screw up at worst. So, then the agents of change get very few at bats since they are uneasy to trust and when they do get a chance then they swing wildly for the fences and their side is retired quickly.

There are generally two ways that substantial change can be accomplished. The first is when things suck so bad that almost everyone agrees what should be done including both broad popular support and the acquiescence of the status quo. Since elites must engineer and implement change then they must support it for it to really happen even if it is only for their own survival against a threatened barrage of pitchforks. The second approach to change is broad consensus among both the populous front and the elites for baby steps towards some common goal. No big change can gain that kind of support without the existence of an imminent existential threat. A long range existential threat (e.g., climate change) is not enough.

If Ordinary Joe gets his Congress this year and they do most of what he described, then they will screw up a lot of it. However, I have no fear that will actually happen.

No to “I thought overproduction, overconsumption, too much of a good thing, was what got us here.”

To paraphrase the immoral words of Bubba Clinton “It depends upon what the meaning of ‘here‘ is.” TB’s reason is a fair approximation of how we got “here” on climate change and the Great Pacific Garbage Patch. Vanishing recent wage gains due to retrograde supply chain inflation is a different “here” entirely. The long run reversal of the New Deal, vanishing American Dream, and Ken Melvin’s “The Gilded Lily” is another “here“, one stemming from JP Morgan (Sr. & Jr.) and their sycophants along with most economists’ belief in capital markets primacy (pure Schumpeter, but entirely consistent with Von Mises and Hayek – and the essential foundation for financialization). Keynes knew differently, but why listen to him?

Money is now moving into the safety of US treasuries with expected ‘transient’ lower ten year note rate. About ten trading days ago the ten year note touched 2.06%. The previous nadir (less than 0.5%) for the US ten year note occurred about a week before the US composite equities March 2020 low.

The point that the nothing has really happened to the US Economy with Putin’s poor judgement is notable. But the asset-debt global economy is interlinked. The overvalued and collapsing Chinese real estate market and the overvalued US property market (relative to disposable income) and the US stock market overvaluations matter.

The Russian Stock Market’s 79 % crash (so far from the Oct 2021 high)..

Putin’s one week Epic Blunder

The Russian Moex composite has been closed since 25 February 2022, before the global banking community put the deep freeze on the Ruble which is undergoing valuation fractal collapse. On 24 February 2022 the Moex composite traded below its March 2020 valuation low. However, the VanEck Vectors Russia ETF fund is still trading and today that index touched below its March 2009 valuation low (7) and 89% below its 2008 peak valuation (59) when the ruble in US dollars was worth 400% more than it was on this trading today. (It had the deadest of dead cat bounces today with a 7 % gain – and still worth only 25% of its 2008 value against the US dollar) The VanEck Vectors Russian ETF is following the March 2020 Global equity composites’ lows 33/72 week first and second fractal series. The Russian ETF fund is following a 71 of 72 week second fractal which is self-assembled into a 14/30/29 of 30 week fractal series. The 30 week third subfractal of this 14/30/30 week series starting the week of l6 August 2021 is following a 6/14/11 of 12 week series. The 14 week second subfractal series is composed of a 3/8/5 and the 12 week final third subfractal is composed of a 2/5/5/2 of 3 week fractal series. Starting 24 January 2022 the trading days to the final low are self-assembled into three sequential fractal daily decay sequences: 3/7/7 days, 2/5/4 days , and as of today 2/4 of 5/4 days.

The best case scenario for the Moex when it reopens is that it will have only lost 90% of it Oct 2021 valuation or about 900 billion dollars.

Just how is Mr. Putin going to pay war reparations?

How War in Ukraine Threatens the World’s Economic Recovery

Bloomberg – Feb 25