Dealing with supply chain issues

February car sales decline, but truck sales continue rebound; plus a comment about the urgency of dealing with supply chain issues

I used to follow vehicle sales more closely – until the vehicle manufacturers, one by one, stopped reporting monthly, and only updated quarterly for the previous quarter. While this makes the data less timely and useful, it reflects their focus on addressing supply chain issues, ensuring that their reporting aligns with more accurate and stable production and distribution cycles.

Fortunately the BEA does keep track of sales, although for some reason FRED is only able to publish the figures with a one month delay.

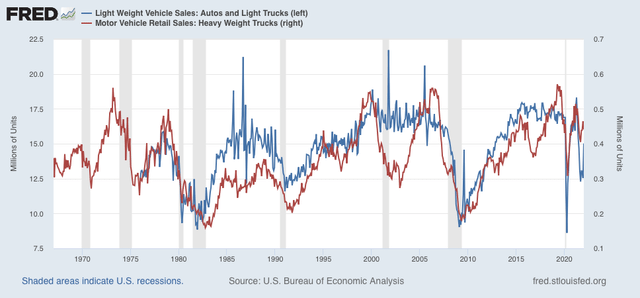

Here is the drill: light vehicle sales generally turn down *after* home sales, but before most other consumer durable goods and other consumer purchases. This makes them a useful short leading indicator, although as you can see below (blue line), they are quite noisy. Heavy truck sales, by contrast (red), turn down earlier, and much more sharply, with much less noise (and the also turn up later after a recession is over):

Heavy truck sales have turned down at least 15%, and usually much more, before a recession has hit.

Now let’s take a look at the last 12 months:

Both car and truck sales peaked early last spring, and bottomed last September. Car sales were down -33%, and truck sales were down -21%. Although not shown, in February according to the BEA, heavy truck sales increased to 0.471 million, only down -8% from their peak. Car and light truck sales decreased again to 14.1 million annualized, down -23% from peak.

Both light and heavy vehicle sales last autumn were consistent with – but did not necessarily mean – an oncoming recession. The rebound in heavy truck sales in the past few months suggests that was a false positive, and is consistent with basically all of the other production and manufacturing data we have received, such as yesterday’s ISM manufacturing report, and durable goods orders.

At the same time, it would behoove the Biden Administration to really lean on, and assist, vehicle manufacturers to solve their supply chain problems. This has gone on for over a year, it has done enough damage to the economy, and Russia’s invasion of Ukraine demonstrates the urgent national security considerations with this type of offshoring.

On the lighter side of vehicle sales, then consumer purchases are further divided between rational demand and reflexive demand. Our vehicles last much longer now that I am retired and my wife’s employer has decided to maintain telecommuting permanently now that the networking and software investment has already been made. To save money now her employer has been selling off their owned office buildings while replacing what they still need for employee “hoteling” with rental space.

NDd

Auto manufacturers, the tiers, and other manufacturers are making money off this artificial shortage. It does not behoove them to fix their own issues either the too short lead time orders or the too much on order purchases. With the former (automotive), they push inventory on the supplier (Tiers) the same as they do the larger than demand orders. Change over to newer models will start mid-year and building too much supply is hazardous to an automotive supplier’s health as they will eat it.

Similar occurred in 2008 with automotive and chips. It took almost two years to sort out.

Non-automotive suppliers may lack flexible capacity. They may also be lengthening lead-times which does nothing for capacity or throughput. They could farm some product out to other companies having it like I used to do. It is better to move parts with more expensive resource or older inhouse resources to maintain delivery.

There are alternatives. And Biden should push them to use some of them.

I agree with your findings NDd.

Bill

Ward’s Automotive reports Light Vehicle Sales once a month, on the 1st…they are the source of the BEA data…although it’s paywalled, enough is available to see that the light vehicle sales report for February from Wards Automotive estimated that vehicles sold at a 14.07 annual rate in February, down 6.4% from the revised 15.04 million annual rate in January, and down 10.2% from the 15.67 million annual sales rate in February a year ago…they link to other files and also have graphs..

that said, i came to this thread to bring this bit of news: