American plutocracy in two simple graphs; plus, when will wage growth bottom?

American plutocracy in two simple graphs; plus, when will wage growth bottom?

The JOLTS report for February comes out later this morning; I may post on it later or tomorrow.

In the meantime, here are updates on several graphs I used to run during the last expansion in order to examine how shared out (or not) economic growth was.

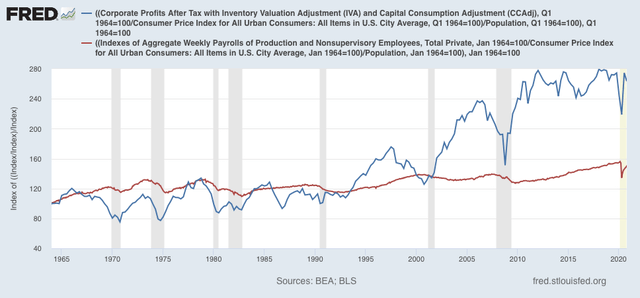

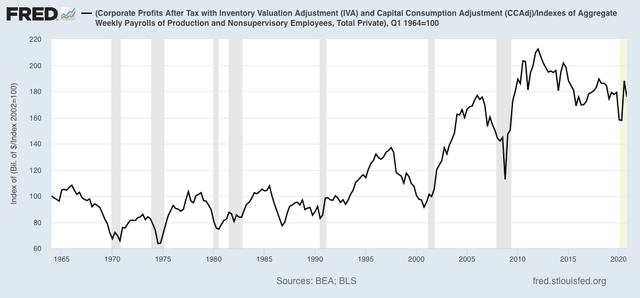

First, here is a graph comparing corporate profits adjusted for inflation, and total nonsupervisory wages, also adjusted for inflation. Both are also adjusted for population growth, so that we can see how much each has grown (or not) per person:

During the era of strong unions, ordinary workers got an increasing share of the pie. That reversed after the 1970s, took off in the 1990s, and really exploded after 2000. By 2020, real corporate profits per capita had grown by 75% more than total wages per capita:

All of which supports President Biden’s plan to raise corporate taxes to pay for infrastructure, as well as Treasury Secretary Yellen’s proposal for a global minimum corporate tax rate.

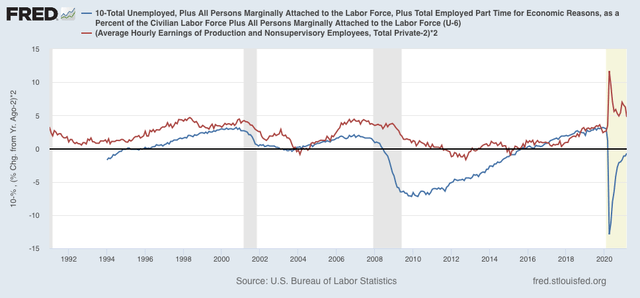

Next, let’s turn to underemployment and wage growth. One graph I used to regularly update was the U6 underemployment rate vs. YoY wage growth, which is a “long lagging” metric. In other words, typically an expansion has to be well underway before wage growth starts to accelerate. Based on the history of the broad measure of U6, which only goes back to 1994, it appears that it takes an underemployment rate of less than 10% for wage growth to finally tick up.

In the below graph, I subtract the U6 rate from 10 (blue), so that, e.g., an underemployment rate of 8% shows as +2%. In other words, the more the underemployment rate is under 10%, the more positive it shows. Meanwhile to account for the long term average inflation rate, I subtract 2% from YoY wage growth (red), and multiple *2 for scale:

The U6 rate as of March was 10.7%, and has declined by about 1% in the past 6 months. There are still about 8.4 million fewer workers, mainly from low-paying service jobs, than there were in February 2020. It will probably require the majority of them to be rehired before wage growth bottoms out.

“During the era of strong unions, ordinary workers got an increasing share of the pie.”

Nothing could remedy this situation more easily and quickly than federal labor law the recognizes that 6% union in private economy instead of 30% or maybe even 60% is the result of illegal vote suppression and that the only way to remedy it is — at long last — to require regularly scheduled cert/recert/decert elections at every private workplace.

When is somebody here going to pick up the topic?

https://onlabor.org/why-not-hold-union-representation-elections-on-a-regular-schedule/

* * * * * *

45,000 votes the other way in three states and the Repulican-Facist Party would have taken control. Take those blue collar votes back with reg scheduled union votes. This is the issue the RFP could not run away from.

It really isn’t about a minimum wage; it must be about a living wage. Those who are doing the work of America deserve a fair share of the returns. Amazon warehouse workers and drivers should be making around $30/hr by my calculations, so grocery store workers, janitors, school cafeteria, restaurant workers, … . Fast-food workers should start at $20/hr, a good entry-level wage. Nurses and teachers should all be paid at least $100k/yr. Mandated, unions too slow.

Denis, “RFP”. Request for proposal or Republican former president? Problem with the latter is that I do not know which you refer to on unions. Seriously, I think labor is probably just about the only real deal killer between Big Business and the Democrats. There is a lot of other stuff like taxes, environmental protection, anti discrimination and so forth which annoys Big Business but they take a back seat to stability. Unions not so much. It is sort of like abortion to Evangelicals.

Ken, if workers can charge consumers as much as consumers will tolerate, then, that will assure a living wage. You must be an American if you think unions are some kind of strange entity. [;-)] Ask a German or a French Canadian if they don’t think unions should be freely available to set up or join without running the impossible gauntlet (why there is only 6% unionized in US private economy).

. . .

I fear the RFP (Republican Fascist Party) is about to steal the 2022 elections — and never let anyone take the government back again. Georgia legislature can now take over vote counting where it feels job not done right by legit poll workers. Only way to take back blue collar America (who are correct in seeing Dems not having done anything for them lately) is regularly scheduled cert/recert/decert elections. This issue would totally swamp any RFP maneuvers with a tsunami of Dem votes.

. . .

Whenever I discuss this with a worker they get all enthusiastic if they think I am talking about something current. Most American workers would kill to get mandated union elections. FREE AT LAST!!!