Industrial production improves in August, but with sharp deceleration

Industrial production improves in August, but with sharp deceleration

If the jobs report is the Queen of Coincident Indicators, industrial production is the King. It, more than any other metric, is found at the turning points where recessions both begin and end.

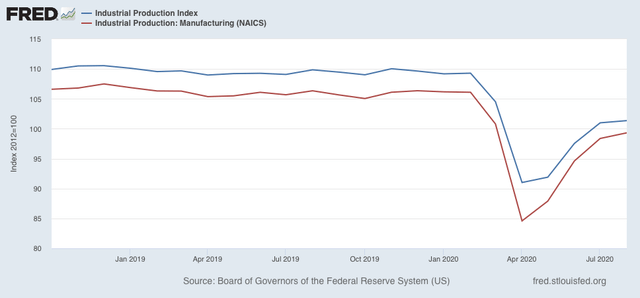

This morning’s report of industrial production for August shows that the recovery from the bottom of the coronavirus recession has come close to stalling out.

Overall industrial production grew by 0.4%, while July was revised higher by 0.5%. Manufacturing production grew just under 1.0%. July was likewise revised higher by 0.6%. Here are the overall totals:

The good news is that manufacturing production has gained back almost 70% of its decline from March. Overall production has gained a little over half of its decline.

The bad news, as is easily seen from the trajectories of the recoveries, is that there has been a sharp deceleration in them since June.

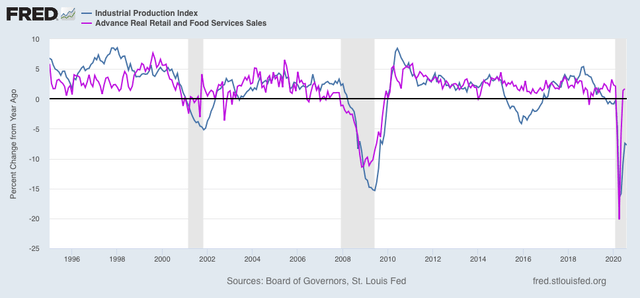

Since production generally follows consumption (but is considerably more volatile), it is not a surprise that industrial production (blue) has continued to recover in the face of a total recovery in real retail sales (violet) (shown YoY):

But with the expiration of supplemental Congressional unemployment aid, like most observers I am expecting that consumption rebound to end – and that will likely show up in the ending of the industrial rebound as well in several months.

re: ” industrial production grew by 0.4%, while July was revised higher by 0.5%

not quite right. July was revised 0.8% higher, and June was revised 0.3% higher.

Republicans should issue every citizen a citizen credit card with $200 per month credit. it would increase our capacity utilization with a multiplier effect and increase our economy of scale, prevent lot of sadness for poor people.

how to pay for this without increasing the public debt? Tax real estate, all real property unimproved, and all improved real property should be taxed.

Mark Perry once said, “when you tax something you get less of it. sure! he’s right about production; but his axiom does not apply to real estate. we will have the same number of square miles and the same number of acres in this country after the tax on real property is levied. Public spending by means of Real property taxation has no “crowding out effect”!

Get

it

!