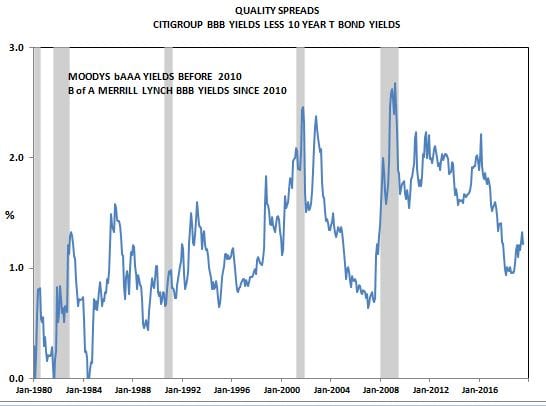

Quality Spreads

While the yield curve turning negative is getting a lot of attention and seems to be the main excuse for yesterdays stock market drop, there are other financial indicators that are also signaling weaker economic growth ahead.

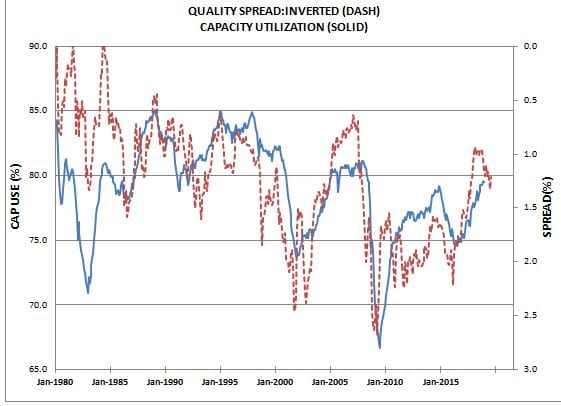

The primary one is quality spreads as the yield on corporate bonds are rising relative to treasuries. This is driven by investors fear that in a weak economy, recession environment the risk of corporate defaults rises and bond buyers demand a larger premium to take that larger risk. It is easy to see that quality spreads are driven largely by economic weakness by comparing them to capacity utilization.

It is easy to see that quality spreads are driven largely by economic weakness by comparing them to capacity utilization.

You are apparently sourcing the credit spread from different sources. If this is supposed to reflect the credit spread for corporate bonds with credit rating = BBB, this spread jumped to more than 5% right after the collapse of Lehman Brothers. So I do not get your chart even if I do get this issue.

Since Moody’s is using 20-year corporate bonds – one should be subtracting the 20-year government bond rate:

https://fred.stlouisfed.org/series/DGS20

This rate was near 2.9% as of late December 2008. It is now around 1.9%.

Moody’s BBB long-term corporate bond rate:

https://fred.stlouisfed.org/series/BAA

Recently near 4.3% so the credit spread is near 2.4% – a bit high. But back in December 2008, this rate was 8.4% so the spread back then was over 5%.

https://www.nber.org/papers/w17021

Credit Spreads and Business Cycle Fluctuations

Simon Gilchrist, Egon Zakrajšek

NBER Working Paper No. 17021

Issued in May 2011

“This paper examines the evidence on the relationship between credit spreads and economic activity. Using an extensive data set of prices of outstanding corporate bonds trading in the secondary market, we construct a credit spread index that is–compared with the standard default-risk indicators–a considerably more powerful predictor of economic activity. Using an empirical framework, we decompose our index into a predictable component that captures the available firm-specific information on expected defaults and a residual component–the excess bond premium. Our results indicate that the predictive content of credit spreads is due primarily to movements in the excess bond premium. Innovations in the excess bond premium that are orthogonal to the current state of the economy are shown to lead to significant declines in economic activity and equity prices. We also show that during the 2007-09 financial crisis, a deterioration in the creditworthiness of broker-dealers–key financial intermediaries in the corporate cash market–led to an increase in the excess bond premium. These find- ings support the notion that a rise in the excess bond premium represents a reduction in the effective risk-bearing capacity of the financial sector and, as a result, a contraction in the supply of credit with significant adverse consequences for the macroeconomy.”

They reference the following seminal papers:

Bernanke, B. S. and M. Gertler (1989): “Agency Costs, Net Worth, and Business Fluctuations,” American Economic Review, 79, 14–31.

Bernanke, B. S., M. Gertler, and S. Gilchrist (1999): “The Financial Accelerator in a Quantitative Business Cycle Framework,” in The Handbook of Macroeconomics, ed. by J. B. Taylor and M. Woodford, Amsterdam: Elsevier Science B.V, 1341–1393.

Yes – Ben Bernanke!

I used Moody’s bond yields until it was discontinued in 2016.

At that time I appended the Merrill Lynch to the old Moody’s series after 2010.

The yields on the Merrill Lynch and Moody’s were virtually identical except between 2005 and 2010. But from 2010 to 2016 the yields on the two series were virtually identical as they had been prior to 2005. Appending the two series in 2010 did not create a discernible break in the series and I feel confident that the data series as it now stand provides the same information as the old economic series.

This is a problem all data users face when an old series is changed. Do we try replicate the old information or give up on the useful insights the old data provided. I feel that using the current Merrill Lynch data without the 2005-2010 spike, does a reasonable job of replicating the old Moody’s data and will stick with it until I’m proved wrong.

But Spencer – FRED still publishes at least monthly

Moody’s Seasoned Baa Corporate Bond Yield (BAA)

And note that this yield exceeded the long-term government bond rate by more than 5% in late 2008. So please review your graph as it does not seem correct.

The general point you are making is quite right but the graph seems off.

My problem with the use of this type of spread is twofold:

1. Notice that some of the time (1981, 1989) it doesn’t seem to lead at all.

2. It’s too noisy. There are plenty of false positives (e.g., most recently 2015).

Prof. Geoffrey Moore found that the DJ Bond average was a better indicator. That series has been changed such that it no longer is helpful, which is why I use Moody’s BAA corporate spread, which has a history pretty close to the DJBI.

Should have said “BAA corporate bond *yield,* not *spread.*

NDD – credit spread is the correct terminology:

https://www.investopedia.com/terms/c/creditspread.asp

“A credit spread is the difference in yield between a U.S. Treasury bond and another debt security of the same maturity but different credit quality.”

Notice the insistence of the same maturity. Moody’s is measuring the yield on 20-year corporate bonds which is why I subtract the yield on the 20-year Federal government bond.

Pgl,

My comment addressed the article itself, not your comment.

Sorry for the confusion.