At the beginning of each year, I try to identify economic series that I think will be most important in the next 12 months. This year I asked: Is the US economy going to enter a Boom in 2018?

There is no standard definition of a Boom. But in my lifetime there have been two occasions when the “good times” feeling was palpable, and the economy was working extremely well on a very broad basis: the 1960s and the late 1990s tech era. During both times, employment was rampant and average people felt that their situations were going well.

Back in January I identified five markers that, taken together, marked off the two eras as unique:

- the low unemployment rate

- the duration of a very good rate of growth of industrial production

- strong growth in real average hourly wages

- strong growth in real aggregate hourly wages, and

- increasing inflation.

Now that the year is ending, let’s update all of these.

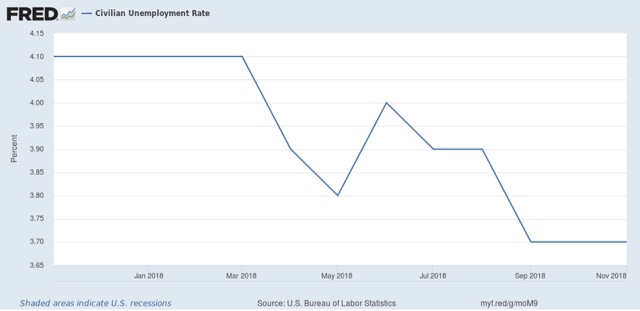

1. Unemployment remains very low

In both the 1960s and late 1990s, the unemployment rate (note that the U6 underemployment rate wasn’t reported in its current configuration until 1994, and so is not helpful), hit 4.5% or below for extended periods of time:

While these weren’t the only two periods of low unemployment, they are among those that stand out.

We had already hit that marker at the beginning of the year, and through the course of the year, it has only improved:

The unemployment rate is now the lowest in 48 years, since 1970.

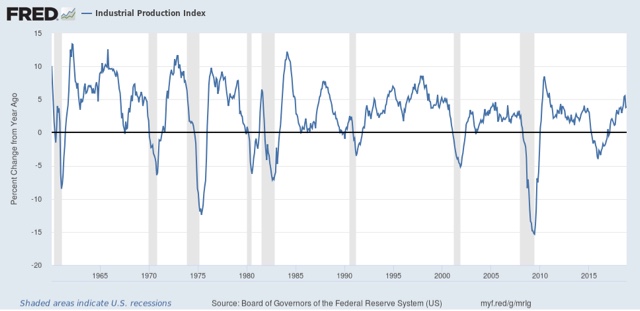

2. Industrial production did briefly boom, but has backed off.

During both the 1960s and 1990s, production grew at or over 4% a year for extended periods of time, not just right after the end of a recession. At the beginning of this year, production was under 4%:

It did surge above 4% during the three months of the third quarter, but for the last two months YoY growth in industrial production is back below 4%:

3. Real average hourly wages failed to ignite

In contrast to other expansions, during the 1960s and the late 1990s, real average hourly earnings also grew at roughly 1% YoY or better, and even exceeded 2.5% growth for significant periods:

During the current expansion, by contrast, real wages have only grown by more than 1% when gas prices have declined dramatically. In 2018, the situation continued: real average hourly wages grew by no more than 0.3% YoY until the last three months, when a big decline in gas prices caused consumer inflation to subside, leading to a YoY rate of growth of exactly 1% in November:

4. Real aggregate payrolls continue to grow modestly

During the 1960s and 1990s booms (as well as some other expansions), real aggregate earnings grew at a rate of 4% YoY or better, for extended periods of time:

By contrast, during this expansion, and continuing this year, real aggregate payrolls have averaged growth of about 2.5% a year:

This is decent, but it’s simply not a boom.

5. Inflation has waned

The fifth and final marker of a Boom — probably as the byproduct of the first four — is an increase in the YoY rate of inflation:

A boom means that resources are getting constrained, so bidding for them intensifies.

The rate of consumer inflation did increase throughout the first half of this year, but since July has waned, and with one month’s data left to go, is only 0.1% higher (2.2% vs. 2.1%) than the rate of inflation at the beginning of the year:

To sum up, the production side of US economy, which was doing well at the beginning of 2018, did briefly boom during the summer, but the consumer side never joined it. Only one of the five markers of a boom — low unemployment — persisted through the year. The US economy did not boom in 2018, and if anything is likely to decelerate sharply in 2019.

There is no evidence that the economy has broken out of the trend of sluggish growth that prevailed over the last 4 years under Obama.

For example the monthly increase in employment gains averaged 204 thousand from 2012 to 2016. But in 2017-2018 it hs averaged 190 thousand.

Trump and all brag about 3% real GDP growth but it was stronger than this in 2014 and 2015 under Obama.

The real story is that the Republican propaganda machine is operating at full force. They come on strong claiming what are about the same numbers as under Obama are new record growth. Under Obama they claimed that the same data was weak. The real problem is not that they are making such claims. Rather it is that the press takes their propaganda at face value and repeat their biases claims.

I for one, am really surprised that the impact of the massive tax cut has been so small.

Whats also crazy is how corporate debt has basically pushed corporate “expansion” above the rate of final demand this long as well. We had that in the 90’s as well(outside the crazy debt stock bubble fueled 1999). Yet GDP has not grown much. I view this the post-Boomer recession in RE. If RE had grown like in 84-00, we would have had better growth. The Boomers, once pro-growth, turned to anti-growth. Luckily, this fades in the 2020’s. But the bull market looks and unlike 2000-1, corporate earnings and profit are a total lie as much of the debt is rated at junk levels. Meaning earnings and profits are going to crash next year creating a recession, which is why the market is contracting right now.

Consumer debt is again at a record high, wages have been essentially stagnant since Ronald Reagan in real terms, the concentration of wealth in the hands of a few continues to increase as does the national debt despite “full employment”. This does not look like a sustainable economy to me, but until the average Joe and Jane wake up to the idea that the system including government is rigged against them we are going to experience increasingly severe economic collapses that we will be less and less able to correct

I consider the low rate of inflation a reason that one might predict that the US economy will not deteriorate sharply. Note the subjunctive, if one were Robert Waldmann one would have noted that almost all of one’s predictions have been wrong and one would try to avoid making predictions.

But one (not typing) might argue that increasing inflation is considered by the Fed Open Market Committee to imply overheating and the need for sharply increased interest rates. One (or rather two named Romer) might go on to note that often the US economy sharply deteriorates soon after the argument that a recession is needed to fight inflation appears in FOMC minutes.

It is true that the last 3 recessions haven’t been deliberately induced inflation fighting recessions. But they have followed clear bubbles which were noted before the recession — commercial real estate & empty office buildings, dot.coms, and houses. What’s the bubble now ?

If I were one who makes predictions, I would predict continued normal growth. But I’m not.

The bubble is in corporate debt, or they have over spent final demand since 2010. I amazed Robert, you can’t see that. When high yield corporate bonds crash, that is the next financial crisis(sans Single Market issue in Europe over England). My guess they are ready to crash, which is the scary scary.

Each bubble was its own story. At least the 90’s stock bubble was a old school bubble caused by overspending by business related to Y2K. By 2000 post-Y2K they badly needed balance sheet repair busting the Stock Bubble. This one……….the balance sheet isn’t that good. They are just using debt to make you think it is.

While food and energy are dampening the headline CPI, the core CPI has increased to over the Fed’s 2% target.

So the judgement over the Fed should remember that the Fed considers

the core CPI a far superior leading indicator of inflation.