A detailed look at Industrial Production during this expansion

A detailed look at Industrial Production during this expansion

In the past week there’s been a little highbrow relitigation of the drivers of the “Great Recession” between Paul Krugman and Ben Bernanke. Bernanke plumps for it having been a “credit event” — and as to the crisis of 2008, he is clearly correct — while Krugman says it was primarily a “housing event,” although Krugman also acknowledges that he is mainly speaking of the aftermath from 2009 onward.

Since neither the 10% decline in housing prices between 1989 and 1992, nor the NASDAQ internet bubble of 1999-2000 managed to cause the worst downturn in 75 years, my own view is that it was precisely because there was a credit bubble in the biggest asset that is owned by a majority of Americans — for which there was no financial help forthcoming to the middle class — that the effects were so longstanding. Had the government — as it did for the 1930s Dust Bowl — bought up or crammed down existing mortgages, and took repayment of the loans out of housing appreciation whenever the owners eventually sold, it is likely that the consumer rebound from the recession bottom would have been much more “V”-ish.

But neither Krugman nor Bernanke, so far as I can tell, mentions a third important reason for the slowness of the recovery: the second installment of the China shock. Because it is crystal clear that businesses decided, once demand picked up beginning in late 2009, to move plants and hiring overseas.

This is plain when we look at how employment recovered. Services employment recovered in relatively “V”-ish fashion: two years down and three years up. Even goods employment ex-manufacturing came back in more delayed fashion, and is at 97% of peak 2007 levels. But manufacturing employment only began to turn very late and, at 92.5% of peak 2007 levels, is still far behind:

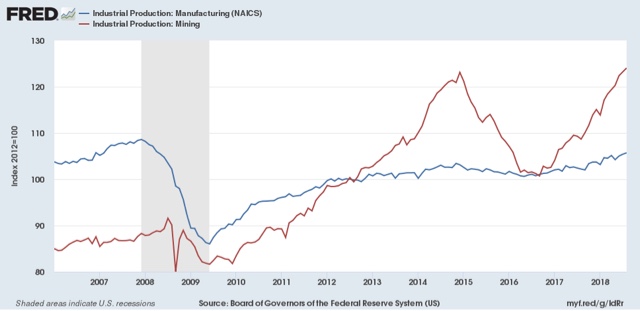

When we look at industrial production itself, a similar pattern unfolds: mining production, led by fracking, took off quickly, while manufacturing industrial production turned more slowly, and has never recovered all the way back to where it was in 2007. In other words, IT’S NOT JUST ROBOTS!!!

At the beginning of this year, I said that a big question for 2018 would be whether the US economy was booming. At that time, I concluded it was not because, while unemployment was very low, wage measures were lackluster, and industrial production had not reached a sustained level of at least 4% that typified the 1960s or late 1990s.

Well, while wages have improved a little, they are still lackluster. But industrial production, measured as a whole, has finally exceeded 4% YoY, at 4.9%, as of August:

But, alas, it turns out that this surge in production is also narrow. When we sort out production between manufacturing and mining, here’s what we get:

Manufacturing production growth exceeded 5% per year for almost all of the 1960s, and for much of the 1990s. But even now it is only up 3.1% YoY, while mining has exceed 10% growth YoY for much of the past 10 years.

In short, the “boom” in industrial production is really just an energy sector boom. US manufacturing is only showing mediocre growth.

I’m not smart enough to evaluate the WHY, but it is definitely true that as far as wage growth goes, structural changes in the economy have meant that recoveries are MUCH slower than they were more than 30 years ago.

China shock was 1997-05. Total IP though during that time exing Computers and the IT boom of the 90’s created a historical surge in IP.

If anything, the China shock has slightly reversed since 2006, yet total IP was on its trend path until 2007 and stopped then. It simply isn’t enough sales. RE is down, Auto hasn’t made a new high in 18 years and has been stagnate at around 17 saars during the peak years unlike 1980-00 when it accelerated from 14 saars to 17 saars(thanks boomers?). Take away Material Extraction manufacturing, total manufacturing has done about as you would expect with middling sales. Real Personal Consumption needs to average 3.5%+ to deliver a boom. Maybe we don’t want that though.