Pew Charitable Trust confirms the “rental (and ownership) affordability crisis”

Pew Charitable Trust confirms the “rental (and ownership) affordability crisis”

In case you thought I was talking through my hat about the general lack of affordability of all types of housing, including both owning and renting, the Pew Charitable Trust has also stepped up with a nearly identical analysis. Go read the whole thing, but here are a few especially noteworthy excerpts:

[A]ccording to the Harvard Joint Center for Housing Studies[, d]emand for rental properties has increased across age and socio-economic groups since 2008….

In the aftermath of the 2007-09 downturn, [… m]any families struggle to save enough for a down payment or lack a sufficiently strong credit profile to meet the stringent underwriting standards that were put in place in the wake of the crisis. But some renters—even with down payment assistance programs— simply cannot afford the monthly payments for homes that in many areas are commanding prices near those of the 2007 market peak

…. The steadily rising demand for rental properties over the past decade has reduced vacancy rates to near historic lows, fueling a rapid increase in rental market prices that has outpaced household incomes for many families. This imbalance is contributing to high rates of “rent burden” …. In 2015, 38 percent of all “renter households” were rent burdened, an increase of about 19 percent from 2001.

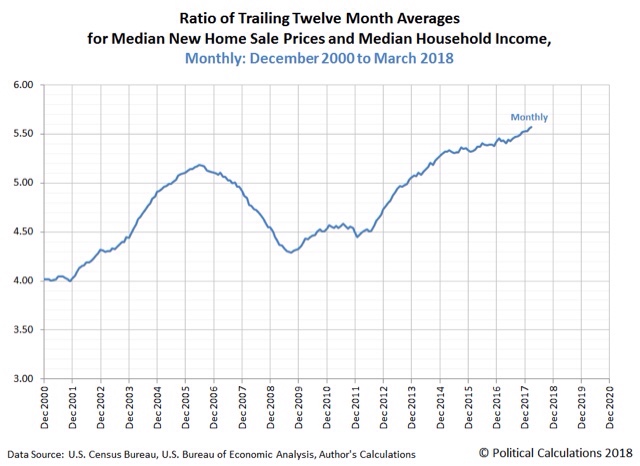

It’s clear that the very high, and in some cases record cost of new housing has played an important role in the surge of households who rent. Here’s my most recent graph comparing median housing costs with median household income (h/t Political Calculations):

That high cost of housing is one driving force behind the surge in rentership:

….[A] 2016 Pew Research Center survey found that 72 percent of renters said they want to buy a home at some point, and most cited financial reasons when asked why they rent. Another recent public opinion poll asked renters ages 18-34 why they were not buying homes, and 57 percent said they could not obtain a mortgage. On the other hand, a recent survey of Americans over 55 found that 71 percent of those who plan to move again said they intended to rent rather than buy. Most renters over 55 cited cost as a driver of their decision and said it makes the most sense for people their age to rent.

In summary, Pew found that

the increased demand for rental properties and their limited supply, along with the lingering effects of foreclosures, demographic changes, and a decline in the rate of renters transitioning to owning, have led to higher rents.

More specifically:

Between 2001 and 2015, the median rent rose from $512 a month to $678, a 32 percent increase.

This is nearly an identical graph to the one I have posted several times, except that it uses the CPI for rents as opposed to the American Community Survey’s “median asking rent” metric, in comparison with median household income.

One significant new piece of information that I hadn’t considered is the change in demographic profile among renters. They note:

…. In 2015, nearly 43 million American households lived in rental housing, an increase of 9.3 million since 2004 and the largest rise since 1970…. However, unlike the early 1970s when young families drove the increase in renting, the 2015 spike is largely propelled by those 55 and older, largely baby boomers, who are responsible for a 4.3 million jump in the number of renters since 2005.

It seems that Boomers haven’t quite finished being “the bulge in the belly of the python” as they compete with the equally large Millennial generation for the scarce resource of apartment housing.

The bottom line here is that incomes simply have not kept up with the costs of all sorts of housing, for both owners and renters. The best way to resolve this problem would be for much more multi-unit housing to be built. Why it isn’t being built is something I have not seen authoritatively addressed. Some, like Matt Yglesias, think it’s all about zoning. There is also the issue of whether building costs are too high for units aimed at lower income dwellers. Part of the issue may also be an increasing oligopolies of local builders.

Whatever the cause may be, it is a real problem, and interest rate hikes by the Fed, which make mortgages more expensive, are severely counter-productive.

TALE OF TWO (or three or more) AMERICAN CITIES

LA

https://www.nbcnews.com/dateline/reporter-s-notebook-covering-homelessness-hits-close-home-n901726

Don’t have time to run down specifics now (rushing out door) but remember most of homeless in L.A. story were out on the street because growing rent outdistanced their shrinking incomes.

* * * * * *

SF

https://48hills.org/2016/02/five-myths-about-the-homeless-problem-in-san-francisco/

“#2 The reason people are homeless is that they lack job skills or are lazy or are on drugs.

Actually, no. The main reason that so many people in San Francisco, and other cities like Los Angeles, are living on the streets is that the cost of housing over the past two decades has vastly exceeded the amount of income that people earn making minimum-wage jobs or bring in from modest pensions, disability, or welfare.”

* * * *

“The vast majority of the people who are homeless today used to be housed – in San Francisco. According to the city’s 2015 homeless count, 71 percent of the people on the streets were living in San Francisco when they lost their housing.”

* * * * * *

[cut-and-paste]

Why Not Hold Union Representation Elections on a Regular Schedule?

Andrew Strom — November 1st, 2017

“Republicans in Congress have already proposed a bill [Repub amend] that would require a new election in each unionized bargaining unit whenever, through turnover, expansion, or merger, a unit experiences at least 50 percent turnover. While no union would be happy about expending limited resources on regular retention elections, I think it would be hard to turn down a trade that would allow the 93% of workers who are unrepresented to have a chance to opt for unionization on a regular schedule.”

https://onlabor.org/why-not-hold-union-representation-elections-on-a-regular-schedule

FORGET LABOR ORGANIZING FOREVER. THE CULTURE IS SO SATURATED WITH UNION BUSTING YOU CAN NEVER PUT THAT GENIE BACK IN THE BOTTLE. If we made union busting a fed felony and hired (tens of) thousands of enforcement agents, what would keep millions of employers and managers from laughing and taunting: “What are you going to do, lock us all up?”

Labor civil war — or regulated piece — take your pick.

* * * * * *

If McDonald’s can pay $15/hr at 33% labor costs — then — Target and Walgreen’s (and most firms) should be able to pay $20/hr at 10-15% labor costs — and — Walmart should realistically have no trouble paying $25/hr at 7% labor costs.

Homeless cannot move to lower rent areas because lower rent areas have even lower wages. Current fed min wage at $7.25/hr is $4.57/hr lower than 1968 fed min adjusted for inflation at $11.82/hr — even though per capita income doubled in the meantime! (I keep looking at that comparison and wondering if I made a stupid addition/subtraction error.)

https://data.bls.gov/cgi-bin/cpicalc.pl?cost1=1.60&year1=196801&year2=201807

* * * * * *

CHICAGO

100,000 Chicago gang age minority males shooting it out daily in street gangs. American born won’t work for $10/hr. I wouldn’t. When my taxi earnings dropped to $10/hr I did not join a street gang — I moved to SF where I could earn $20/hr driving a cab instead.

https://www.nbcchicago.com/news/local/chicago-crime-commission-gang-book-485166811.html

I gave up free rent in my mother’s large comfortable apartment, free utilities, free use of my brother’s Lincoln Town Car — for a (soon now to be demolished) residence hotel where the electricity went out in your little room 4-5 times a day (you bought the biggest computer backup battery you could afford and plugged it into the only outlet — for when one tenant too many tried to run something off your “community” circuit breaker) and the elevator went out once a week. The people were alright — a little like in the movie the The Million Dollar Hotel.

But I was making $20/hr (more to come as my seniority and knowledge grew) — I would figure the rest out later.

$20/hr jobs is the answer to most of this country’s problems — along with re-empowerment of the average person’s interests through resurrected labor unions from coast to coast.

Boomer here.

After selling our home last year, for a variety of reasons we chose to rent instead of re-invest in a mortgage…mostly because:

• no property tax bill

• no maintenance hassles/costs (we are in a really well-run building)

• DC rents are roughly same as mortgage/tax/insurance costs

• Rent Control!

I’m not surprised that many other boomers are taking similar steps if they have the options. Sorry that we collectively dominate the market – we’ll die soon enough and leave the next generation a chunk of change…

You got it backwards. The Fed should make mortgages costly and reduce housing costs. Sorry, but lower interest rates are part of the long run problem. You take the old stupid line that cutting interest rates are the key to everything. It isn’t. We need higher rates to reduce costs and changes in investment patterns.

America hasn’t taken short term pain since the 80’s. Time to do so again.

RE is always “local” Rents in the biggest rental market in the USA (NYC) have been falling for more than a year.

E Lampert just cherry picks data….

https://www.bloomberg.com/news/articles/2018-04-12/pick-a-new-york-city-borough-rents-are-falling-there-and-fast

BK…..that is not Ed.

Ed did it for sure! It has to be Ed. Who else would it be?

Invasion works, duh

The real question is ,….why do renters vote for pro-invasion elected officials?

Smitty:

Welcome to Angry Bear. First time posts always go to moderation to weed out spammers and advertising.