March JOLTS report: powerful further evidence of a taboo against rasing wages

March JOLTS report: powerful further evidence of a taboo against rasing wages

The March JOLTS report this morning is powerful further evidence that raising wages (or training new workers) has become a taboo.

Just about everyone thinks that, faced with a worker shortage, “rational” employers will offer higher wages to fill the empty skilled positions. This in turn will draw more marginal potential workers into open unskilled positions.

That’s the theory, anyway.

What is really happening — as so breathtakingly shown this morning — is that by and large employers will refuse to raise wages, and then complain about their unfilled job openings.

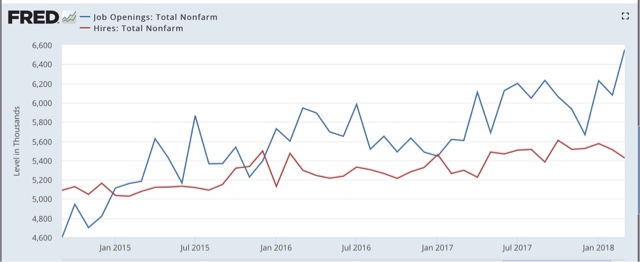

As Exhibit “A,” I give you job openings (blue) vs. actual hires (red) in this morning’s report:

Incidentally, Paul Krugman may be ready to embrace the idea of a taboo against raising wages, although for now he is plumping for the “employers are afraid of getting stuck with a highly paid workforce when the next recession comes” hypothesis. The problem with that particular hypothesis, though, is that such skittish employers — a lot of them anyway — won’t bother to post new job openings, since they know they would need to raise wages to fill them. The big spike in openings in this morning’s report suggests instead that employers are refusing to get the message.

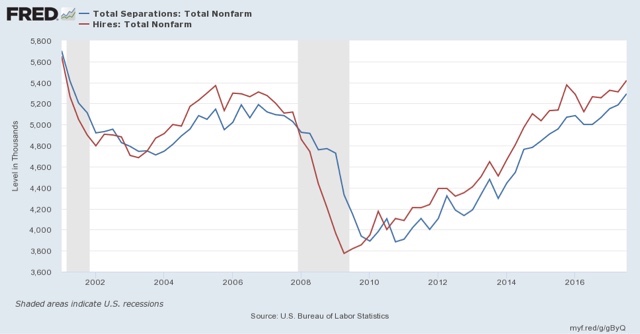

Turning to other noteworthy items in the report, as a general rule, historically hiring leads firing. While the one big shortcoming of this report is that it has only covered one full business cycle, during that time hires have peaked and troughed before separations. This is manifest when we compare hiring (red) and total separations (blue) on a quarterly basis as it existed through the end of the third quarter of 2017:

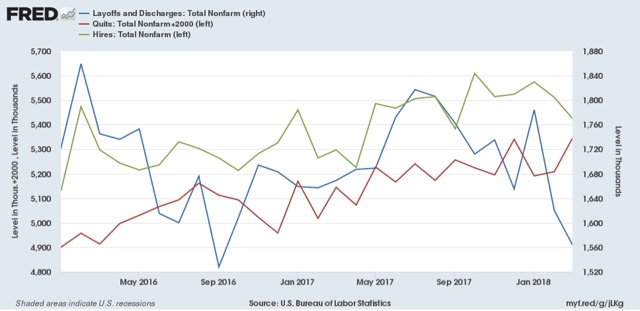

If hiring and total separations have indeed peaked for this cycle, based on the last cycle I would expect quits to continue to improve for a short while — and they have — before also beginning to decline. As a counterpoint to that, separations have approached their bottom, a very good sign.

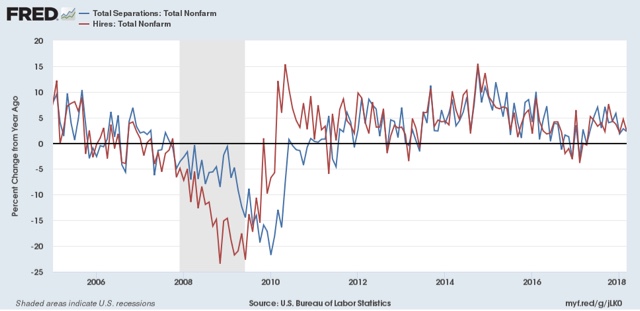

Two months from now when the YoY comparisons get much harder, if we haven’t established any new highs in hires and total separations, and they are at or below zero — which is a real possibility — then we may have confirmation of a late-cycle trend.

“employers will refuse to raise wages”

There is also the issue of productivity. If the worker doesn’t produce enough to justify the higher wage, he won’t/shouldn’t be hired. Unless the employer can raise prices.

We know it isn’t about productivity. Wage gains have lagged productivity gains since the 1980s.